IN PARTNERSHIP WITH

For more information visit: www.incisiveworks.com

This digital experience is an Incisive Works product © 2021 Incisive Business Media (IP) Limited

Real assets and the net-zero pathway

xxxxxxx

xxxxxxxxxxx

The sustainable forces driving change in real assets

The real asset green premium explained

ast year saw record issuances of green, social and sustainability (GSS) bonds. 2021 has been similar, reaching several new records. At the same time,

climate risk has become a key consideration to ensure stability of financial returns going forward as issuers and investors alike grapple with physical and transition risks.

L

Yet challenges remain as to how fund managers can properly incorporate these considerations into investment strategies and continue to deliver risk-adjusted returns for investors.

“Net zero commitments are set to revolutionise the world of long-dated real assets”

scroll

Fixed IncoMe and ESG

Disclaimer Past performance is not a guarantee or a reliable indicator of future results.The Fund will be actively managed in reference to the Bloomberg Barclays MSCI Global Green Bond Index as further outlined in the Prospectus and Key Investor Information Document. Performance and fees Past performance is not a guarantee or a reliable indicator of future results. Performance figures are presented net of management fees commissions, other expenses, and the deduction of actual investment advisory fees; but do not reflect the deduction of custodial fees. The "net of fees" performance figures above also reflect the reinvestment of earnings. All periods longer than one year are annualized. Separate account clients may elect to include PIMCO sector funds in their portfolio; sector funds may be subject to additional terms and fees. Charts Performance results for certain charts and graphs may be limited by data ranges specified on those charts and graphs; different time periods may produce different results. ESG Socially responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgment exercised, by PIMCO will reflect the beliefs or values of any one particular investor. Information regarding responsible practices is obtained through voluntary or third-party reporting, which may not be accurate or complete, and PIMCO is dependent on such information to evaluate a company’s commitment to, or implementation of, responsible practices. Socially responsible norms differ by region. There is no assurance that the socially responsible investing strategy and techniques employed will be successful. Past performance is not a guarantee or reliable indicator of future results. For professional use only The services and products described in this communication are only available to professional clients as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness.The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E) and PIMCO Europe GmbH Irish Branch (Company No. 909462) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch and Spanish Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; and (3) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication.| PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2) . The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser.

For portfolio manager Ketish Pothalingam and ESG research analyst Samuel Mary, the importance of proprietary forward-looking methodologies is often core to delivering both ESG metrics and return objectives in fixed income.

Unearthing the future of sustainable fixed income

Past performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested.

he growth of responsible and sustainable investing is changing the shape of the investment industry and could prove critical in

supporting the transition to a lower carbon and more socially just world.

Fixed Income and ESG

In addition, the importance of fund manager engagement and their influence in helping companies to drive climate-change focused transitions, such as the race to net zero, have become crucial in 2021.

Mark Meiklejon on the Aviva Investors’ Climate Transition Real Assets Fund

How can pension funds use ESG to futureproof portfolios?

For Professional Clients only

In this exclusive Spotlight guide, we explore the future of the sustainable fixed income market, discussing the driving forces for future growth and the impact of more stringent regulation and an intensified global focus on sustainability, including the COP26 event that recently took place in Glasgow.

We also speak to Pothalingam and Mary about PIMCO’s award-winning GIS Climate Bond Fund, launched in September 2020, and how this product achieves its climate and sustainability goals using PIMCO’s proprietary tools and methodologies.

Featured in this Spotlight

Click on the plus icons for more information

Ketish Pothalingam Portfolio Manager, EVP

Ketish is a member of PIMCO’s ESG team, focusing on corporate credit and global bond ESG portfolios

Samuel Mary ESG Research Analyst, SVP

Samuel focuses on the integration of ESG factors into PIMCO's portfolio management and credit research

Why the ‘tooth and nail’ fight for ESG data is key to future of sustainable bonds

ESG engagement in action

PIMCO GIS Climate Bond Fund

Spotlight on:

SPOTLIGHT ON:

ESG labels versus investor goals:

How PIMCO integrates real sustainable thinking into bond strategies

SPOTLIGHT

MENU

HIDE X

But like many asset managers, over the last decade, PIMCO has been intensifying its focus on ESG issues. A decade ago, it became a signatory of the UN Principles for Responsible Investment (UN PRI) and established a dedicated ESG team. From 2017, PIMCO began launching dedicated ESG-labelled bond products and now offers a full suite, including the GIS Global Bond ESG Fund, the GIS ESG Income Fund and the GIS Climate Bond Fund.

socially responsible version of one of its key funds as far back as 1991.

he idea of investing with environmental, social and governance (ESG) principles in mind has been gaining traction in the world of investing for several years, but the concept is not new for PIMCO. The bond house first offered clients a

T

“We see this as totally consistent with the way our credit analysts think”

ESG labels versus investor goals: How PIMCO integrates real sustainable thinking into bond strategies

As one of the biggest bond houses in the world, merging the worlds of fixed income and ESG has come naturally to PIMCO over the past decade. Yet integrating sustainable metrics must go beyond investment strategies and ensure risk is considered too – especially when it comes to climate change targets.

According to Ketish Pothalingam, portfolio manager and member of PIMCO's ESG team, today the group has ESG integrated in its investment thinking, with sustainability metrics integrated into the way teams consider risk.

For PIMCO there are two key types of climate risk that must be considered: transition risk, which includes the risk posed by increasing climate regulation and reporting standards globally, and the physical risks from climate change, such as wildfires and floods. To measure these risks, the firm is constantly working on developing proprietary analytical frameworks and scoring methodologies.

This is particularly the case when it comes to one of the most hotly debated and researched sustainability topics of the year: climate change.

Risk assessment

The EU Sustainable Finance Disclosure Regulation (SFDR), which came into force in March 2021, aims to improve financial industry transparency and consistency on sustainable investments and associated processes, discourage misleading claims about an investment’s sustainability credentials, and encourage the integration of financially material sustainability risks into the investment process. It obliges certain financial market participants to make what can be complex sets of disclosures. It is one of several measures the EU is using to create a common framework for sustainability and to reorient capital flows, with the aim of easing the transition to a more sustainable economy.

“The move to quantify everything could really be dangerous if it ends up removing that human layer of judgment”

Royal London Asset Management is one of the longest-established responsible investors in the industry. So, what does its experienced team think are the most fruitful paths and potential dead-ends in the latest market developments?

who has lived with a teenager knows that fast maturation comes with challenges and a few wrong turns.

he world needs responsible and sustainable investing to mature and grow so that it can drive beneficial change more quickly. But anyone

For Mike Fox, Head of Sustainable Investments, the overarching positive change in the last few years is that “responsible and sustainable investing has an influence and cultural acceptance it simply never used to have.”

Researching reality

Hamilton Claxton says that a parallel trend is also now clear. “The conversation is moving on from ‘what is the financial ESG risk of my companies or my funds’ to ‘what is their direct impact on sustainability’, in addition to any financial risk implications,” she says. This shift is changing the approach of the Responsible Investment team – who work not just with Fox’s sustainable funds but across RLAM’s investment universe.

“We're thinking more broadly about how we can research, describe and measure the direct impact of large corporations on the world,” she says, “and we’re looking at new information in new ways.”

More broadly, the availability of sustainability data is gradually improving and there is increasing pressure from investors and regulators to use that data to back up claims about sustainability.

The power of engagement

Yet even when issuers fail to meet the stringent criteria for inclusion into the firm’s ESG-focused fixed income funds, PIMCO continues to engage with companies with a view to helping them improve and perhaps become eligible for investment over time. This approach has already been successful in the past, says Mary.

Pothalingam adds that PIMCO’s scale allows it to drive positive change in corporate behaviour on ESG metrics: “PIMCO is a firm with a significant amount of assets under management. In the context of this, the firm has the ability to interact with the senior management of corporates and pose questions relating to all areas of those companies’ business, including climate change and the sustainability of business models.”

While climate is a key area of focus, PIMCO employs a holistic approach which takes into account many other ESG-related issues, as well as a wide variety of environmental concerns, such as preservation of biodiversity. This multi-faceted approach, along with the expertise and breadth of the team, allows PIMCO to lead the way and continue to innovate in the area of ESG fixed income.

In the utilities sector, PIMCO does not base its evaluation of a company on past emissions reduction, but rather evaluates expected future reductions based on a company’s strategy to transition from coal to renewable energy. Its future energy mix must be climate-friendly and in line with the International Energy Agency’s climate pathway. For example, an Italian utility company has committed, both verbally and in their annual report, to reach 55% renewables by 2022, 60% by 2024 and so on. PIMCO has backed this company’s debt, as it is seen as a climate leader.

Did you KNOW?

“We see this as totally consistent with the way our credit analysts think,” he explains.

Samuel Mary, ESG research analyst at PIMCO, explains that it is one of the reasons why having a proprietary methodology is particularly important for fixed income investors: “Many ESG-related ratings are developed for equities, so it is extremely important for us as a fixed income manager to have a proprietary methodology that is looking at ESG characteristics.”

Crucially, these metrics must be forward-looking to spot the “winners” of the transition to a net zero carbon economy. As engagement is also a key part of the investment strategy, PIMCO’s metrics also allow the team to monitor issuers on their journey to net zero.

“We have been developing certain tools that are evaluating not only the current carbon emissions associated with a portfolio, but the glide pathway for future portfolio carbon emissions or exposure to green bonds that will be bringing down carbon emissions, consistent with the Paris Agreement 1.5-degree objective,” says Mary.

“PIMCO’s scale allows it to drive positive change”

Pothalingam adds that “a label doesn’t confirm virtue”, which means the ESG fixed income investment process is highly active. PIMCO’s proprietary methodology allows it to “say ‘no’ to many labelled bonds, since a label doesn’t necessarily mean it is aligned with ESG goals”, he explains.

Active approach

As a result, the team does not simply invest in green or sustainability-labelled bonds; the approach is multi-faceted and includes identifying climate leaders in each sector and regular engagement to ensure the issuer is on track to achieve its climate commitments within the set timeframe.

The GIS Climate Bond Fund invests across three key segments: green bonds – those labelled ‘green’ and displaying best practices; climate leaders – those that are ahead of their competitors in mitigating climate emissions; and unlabelled green bonds – issuers that are fundamentally aligned with a low carbon pathway. This broad and inclusive approach allows PIMCO to capture the best opportunities across the board, while also remaining highly selective in its exposure and picking issuers that are leading the way in the transition to net zero.

One of the ways to ensure an issuer is aligned with climate transition goals is via sustainability-linked bonds where the coupon is contingent on the company meeting specific interim targets. According to Pothalingam, companies that don’t want to make climate commitments will find that over time the cost of their debt might increase. This incentivises businesses to create ambitious targets and meet them within the specific timeframe to avoid having to pay more for their debt.

Electrification of transport

Carbon capture technology

Engagement in action: Utilities

Physical risks from climate change include wildfires and floods.

For Dixon, his attraction to this sector has been fuelled by a decade-plus long green career. He joined Aviva Investors in 2019 as head of ESG, Real Assets and brought with him a wealth of experience from the private sector. He had held senior sustainability roles at commercial development company Landsec, construction firm Mace and retailer Marks & Spencer. In addition, Dixon is a graduate of the Sustainability Leadership Programme at Harvard.

Spotlight on: PIMCO GIS Climate Bond Fund

(1) UNPRI assessment report limited to asset managers signed up to the Principles for Responsible Investment (PRI) and based on how well ESG metrics are incorporated into their investment processes. UNPRI Transparency Reports are available at https://bit.ly/3AdJamv.

Sources.

The first is regulation resulting from global efforts to cut CO₂ emissions and stop the devastating effects of climate change. Whether this means the de-carbonisation of heat, transport, buildings and electricity, Dixon sees these regulatory changes influencing all aspects of real asset investing, creating both risks and opportunities for long-term investors. For example, in the UK, buildings accounted for 17% of emissions in 2019 and the Climate Change Committee recently estimated investment of £2.8bn¹ per year is needed to decarbonise commercial buildings.

Regulatory decarbonisation

The global energy transition

These efforts will also result in a global energy transition, which could see a carbon tax imposed on carbon-intensive industries to drive assets into greener alternatives at a faster pace. Already, more than 110 countries have made a commitment to become carbon neutral by 2050. Institutional investors are also making pledges, with the Aviva Investors’ Real Assets Study finding that 92% of global insurance and pension fund investors are committed to achieving net zero.

Existing and proposed legislation will put the onus on asset owners to account for the sources of climate risk in their portfolios and find ways to mitigate it. The physical and transition risks of climate change will affect real asset holdings, such as energy and fossil fuels. At the same time, a growing number of areas, such as carbon capture and storage technologies, will require financing. Opportunities are also being created across other, less obvious areas of the market, including renewable-only energy suppliers, efficient energy suppliers and buildings, and sustainable transport.

Renewable technology

Meanwhile, technological innovation is driving down the cost of renewable energy, making it a more viable investment option. In fact, according to the Exponential Roadmap report, “by 2030, renewables hold the very real promise of abundant almost-free energy”. On the other hand, carbon-intensive investing is set to be more expensive as carbon pricing schemes are becoming more mainstream.

Shifting portfolios towards investment in renewable energy sources can help pension funds manage transition risk in portfolios while also maximising returns. According to a study by Imperial College London and the International Energy Agency , renewables investments in Germany and France yielded returns of 178.2% over five years, compared with -20.7% for fossil fuel investments. UK green energy investments returned 75.4% versus just 8.8% from fossil fuels over the same timeframe.

Post-pandemic sustainable initiatives

The third key theme in real asset investing will come from the societal changes resulting from the Covid-19 pandemic. This is likely to drive differentiation in performance within the asset class itself.

Given these changes, investors can expect strong performance from areas such as logistics, data centres and e-commerce, which have benefitted from a shift to digital and online, while investment in sustainable buildings is set to continue growing.

In the long-term, Dixon says that being aware of these macro trends, while also “understanding your back book and mitigating downside risks” can create strong portfolio performance for real asset investors with long-term liabilities, such as pension funds.

(2) Square Mile - A rating is not a recommendation to buy, sell or hold a fund. Square Mile is an independent investment research business that works in partnership with regulated professional financial services firms.

(3) The Greenhouse Gas Protocol defines Scope 3 emissions as all indirect emissions in the value chain of a company not captured in Scope 2, indirect emissions from the generation of purchased energy, or Scope 1, direct emissions from owned or controlled sources. Data coverage for carbon intensity: c. 92.6% of the Corporate PMV (Percentage Market Value) of the funds. This figure represents the issuer’s most recently reported or estimated Scope 1 + Scope 2 greenhouse gas emissions normalized by sales in USD.

2

3

NEXT >

< PREV

The Fund focuses on issuers with lower carbon emissions and intensity to reduce the footprint of the entire portfolio. This has led to a significant reduction in both Scope 1 and Scope 2 emissions of the GIS Climate Bond Fund compared to the broader IG credit market (represented by the BBG MSCI Global Agg Credit index). (3)

The infographic below shows the CO2 emissions reduction of the average corporate issuer in the Fund versus the global credit index and puts this number into an easily understandable context. (4)

Fund's average corporate issuer emits 4,817,373 less tons of CO2 than the global credit index, which equivalent to:

Incandescent lamps switched to LED's

Tree seedlings grown for 10 years

Passenger vehicles taken off the road in one year

Homes powered by clean energy for one year in the United States

OR

Significant reduction in co2 emissions

A focus on sustainability

PIMCO has a holistic approach to climate action going well beyond green bonds, investing in issuers that the firm deems to be at the forefront of the net zero transition. Examples include renewable energy generation companies, a municipality-owned water system, and a REIT whose science-based carbon emissions reductions targets cover both corporate operations and logistics.

Key Investment Guidelines

• Duration range 2-8 years

• Max 25% of total assets in HY

• Max 25% of total assets in EMD

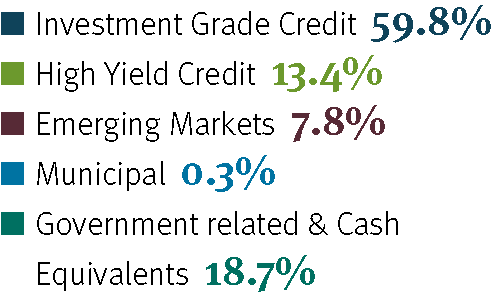

The GIS Climate Bond Fund invests across the spectrum of the bond market, finding opportunities even in those areas that are not traditionally known for sustainable bonds. While the largest exposure remains to investment grade credit, as can be seen from the chart below, a quite meaningful proportion is allocated to high yield credit and emerging market debt. As the universe continues to grow, the team expects to see new opportunities in a wider range of market segments.

The second pie chart shows the climate-related breakdown of the Fund between the three key segments. The majority is invested in green bonds and climate leaders, while unlabelled bonds remain a relatively small proportion of the portfolio.

Asset class breakdown - mv%

climate related breakdown - mv%

What doesn’t the Fund invest in?

Fossil fuel-related sectors across the value chain

Violations of UNGC compliance / UN human rights

Alcohol, gambling, tobacco, weapons, adult content

PIMCO ESG sovereign exclusions including sovereign issuers with poor governance practices and/or those in violation of global principles

PIMCO’s sustainable heritage

PIMCO manages first Socially Responsible separate account

Sustainable Investment Assets under management (7)

PIMCO becomes a signatory to the U.N. Principles for Responsible Investing (PRI)

Investment Professionals with Sustainable Investment leadership responsibility

PIMCO’s U.N. PRI Assessment Report (8) (2018, 2019, 2020) across all Fixed Income categories

Impactful global initiatives, as a market leader driving sustainable change

Launches Climate Bond Strategy, winning ESG Investment of the Year as a climate-themed bond solution

1991

$627B

2011

2019

20+

A+

50+

PIMCO’s aim is to be a leading provider of ESG fixed income solutions and it does so by focusing on what it considers to be powerful engagement platforms, which allow it to drive positive change in the market.

This includes work with the United Nations Global Compact (UNGC) CFO Taskforce to drive market innovation and collaborating with the International Capital Markets Association (ICMA) to help shape industry standards. A key area of focus for the firm is to improve data quality in the fixed income space and PIMCO works closely with regulators and industry bodies to drive standardisation in this area. (9)

Fund overview

(exc. mortgage- and asset-backed securities)

Fund name: PIMCO GIS Climate Bond Fund Benchmark: Bloomberg MSCI Global Green Bond Index Management style: Actively managed Approach: Not a relative return product, seeks to deliver positive investment performance while supporting positive climate change solutions. Awards and recognitions: Company-wide: A+ rating in the UNPRI Assessment Report across All Fixed Income Categories. (1) GIS Climate Bond Fund Specific: ESG Investment Initiative of the year (By Environmental Finance Sustainable Investment Awards), Positive Prospect Rating (by Square Mile). (2)

(4) Greenhouse gas equivalencies are calculated according to US EPA methodology found at: https://bit.ly/3AL95Ca. Corporate bonds only.

(5) PIMCO. Past performance is not indicative of future results.

(6) Climate related breakdown includes: EM sovereigns, corporate credit, securitized, munis.

(7) PIMCO. As of 30 June 2021. Sustainable Investment AUM includes third party and Allianz Socially Responsible AUM (negative screened portfolios), ESG AUM (portfolios with ESG objectives) and thematic AUM.

(8) UNPRI assessment report limited to asset managers signed up to the Principles for Responsible Investment (PRI) and based on how well ESG metrics are incorporated into their investment processes. UNPRI Transparency Reports are available at https://bit.ly/3AdJamv

(9) As of 30 June 2021. KPI: Key Performance Indicator

(1) to (5) as of 30 September 2021. PIMCO, MSCI, EPA

(5)

(6)

Driving positive change

In 2020 alone, PIMCO’s global team of 75+ credit analysts engaged with close to 1,600 corporate bond issuers on ESG-related topics, with more than 600 of these representing substantive repeat interactions where PIMCO’s analysts provided recommendations on material issues such as climate risk, balance sheet strategy, health & safety, supply chain and setting long-term ESG targets.

THREE SEGMENTS

Green Bonds

Unlabeled Green Bonds

Climate Leaders

(1) Climate Change Committee, “The sixth Carbon Budget, The UK’s path to Net Zero”, 2020.

Green bonds - those issued

Issuers fundamentally aligned to low carbon products and services, including renewable energy 'pure-plays'

PHARMACEUTICAL COMPANY

Sustainable Investment Assets under management1

PIMCO’s U.N. PRI Assessment Report (2) (2018, 2019, 2020) across all Fixed Income categories

<

>

driving market innovation

United Nations Global Compact (UNGC) CFO Taskforce aims to engage global CFOs on sustainable development, leveraging the nearly 10,000 UNGC-participating companies

Co-founded by PIMCO, in partnership with the UNGC and energy utility Enel, and co-chaired by Scott Mather, PIMCO’s Managing Director and Chief Investment Officer of US Core Strategies

setting industry standards

International Capital Markets Association (ICMA) promotes resilient well-functioning global debt markets through developing standard best practices

PIMCO participates on the Executive Committee, which oversees ICMA and its impact bond principles / guidelines, and the Climate Transition Finance and Sustainability / KPI-linked bonds Working Groups

Topic: Covid-19 resilience and responsibility

(1) Department for Business, Energy & Industrial Strategy provisional UK emissions 2019

Source.

4

Real assets are directly responsible for a large proportion of the carbon dioxide in the atmosphere. For example, direct emissions from buildings, power and transport account for 60% of all emissions in the UK¹. As a result, the decarbonisation efforts create huge opportunities for investors, from financing new building projects, to investment in green building materials, to allocating to renewable energy grids.

Aviva Investors’ net-zero real asset commitment

ngagement is the backbone of PIMCO’s sustainable fixed income offering, and there are many examples where the firm has worked with issuers to actively improve their ESG credentials.

E

80+%

of PIMCO's firm-wide holdings of corporate issuers were engaged on ESG topics in 2020

PENSION FUND – AUSTRALIA

MULTINATIONAL INSURANCE AND FINANCIAL SERVICES COMPANY

Sustainability goal: Responsible investing ESG investing approach: Company B is fully committed to investing responsibly, and in a way that positively impacts people and the planet. Client partnership: In 2020 Company B announced a Climate Change Transition Plan that will see the A$60bn pension fund commit to reducing the absolute carbon emissions in its portfolio by 33% by 2030 and to net zero by 2050. They are the first major Australian pension fund to make carbon reduction commitments of this scale. PIMCO has been working closely with Company B to enhance the positive impacts of their portfolios, measuring the carbon footprint of their portfolios in order to measure the change and improvement over time, and allocating more to issuers with favourable ESG profiles.

The partnership approach

Sustainability goal: Net zero commitment by 2050 for insurance investments ESG investing approach: Company A systematically integrates ESG considerations across its business activities. On the insurance investment side, as a founding member of the UN-convened Net-Zero Asset Owner Alliance, Company A has committed to becoming carbon neutral by 2050 and to emphasize carbon emissions reduction outcomes in the real economy. Following that commitment, in 2021 Company A announced an ambitious set of 2025 targets for insurance investment portfolios. Partnership: PIMCO and Company A have partnered very closely on implementing and refining the way ESG criteria are reflected in insurance investment portfolios, a journey that started several years ago and is continuously evolving. The next step in this partnership is achieving intermediate and long-term climate objectives, as well as working on how climate targets can be achieved in portfolios.

Background: Company C is the UK’s largest food retailer and PIMCO believes it to have a leading practice on ESG within the food retail sector.

Engagement: PIMCO regularly engages with Company C on a variety of ESG factors, including deforestation, sustainable bond issuance, and supply chain disruption. Early in the Covid-19 crisis, PIMCO engaged with the food retailer on its plans around worker health and safety.

Progress to date: PIMCO found that Company C demonstrated reasonable resilience and responsiveness in upholding expectations on employee health and benefits. They kept vulnerable staff and workers in self-isolation at home with full paid leave at the outset of the pandemic to minimise health risk for its workforce. Longer term, Company C continues to target more sustainable packaging by establishing a closed loop for plastics. It has worked with suppliers to remove hard-to-recycle materials, with industry-leading innovation to create recyclable products, which help prolong the shelf life of goods and reduce food waste. In early 2021 Company C also issued its first sustainability-linked bond.

FOOD RETAILER COMPANY

Topic: Covid-19 resilience and responsibility, access to healthcare

Background: In the pharmaceutical industry, PIMCO typically looks for internal controls to guard against questionable sales incentives and marketing practices, guidelines regarding interactions with healthcare professionals, drug pricing transparency and access to healthcare strategy which aligns with diversity & inclusion programmes.

Engagement: PIMCO engaged Company D on Covid-19-related concerns, including supply chain disruption preparedness, employee health measures and benefits, and access strategy for vaccine delivery. The analysts were looking to better understand Company D’s approach to encouraging responsible promotion through sales incentive structures and transfers of values to healthcare professionals. Despite leading efforts to partner across the sector and with prominent research institutions and manufacturers to ensure fair access, Company D has faced recent concerns over its intellectual property (IP) and patent protection policies related to its Covid-19 vaccine. PIMCO encouraged the issuer to increase transparency on its approach to equitable access related to Covid, as well as to focus on the development of additional therapeutics for Covid-19, given the lack of treatment options currently available.

Progress to date: The company has steadily improved its access-to-medicine strategy over the years for developing countries and antimicrobial resistance. There is a strong focus on strengthening health systems by investing in capacity-building initiatives to enhance patient access to care and vaccines, seeking to prevent opioid overdoses, and medicine drone delivery. Additionally, their recent sustainability bond issuance, the first of its kind in the biopharmaceutical industry, will use proceeds to help manage the company’s environmental impact, strengthen healthcare systems, and support increased patient access to Company D’s medicines and vaccines, especially among underserved populations. Company D is also rated as one of the top five by the Access to Medicine Index 2021 due to its improvement on access strategies and planning in developing countries.

(1) PIMCO firm-wide ESG engagement activities, Jan 1 - Dec 31, 2020

(1)

the world of investing for several years, but the concept is not new for PIMCO. The bond house first offered clients a socially responsible version of one of its key funds as far back as 1991.

he idea of investing with environmental, social and governance (ESG) principles in mind has been gaining traction in

2020 Engagement by industry

2020 in-depth engagement by theme

The Brundtland Report, sponsored by the United Nations and named after Gro Harlem Brundtland, chair of the World Commission on Environment and Development (WCED), was a milestone in the attempt to build a more sustainable world. Published in March 1987, the report attempted “to formulate an interdisciplinary, integrated approach to global concerns and our common future,” particularly with respect to sustainable development.

What is the SFDR?

What was the Brundtland report?

Back up to choices

There are many driving forces behind the growth of this area of the fixed income market. One of the key reasons is increasing climate-related regulation, with Europe leading the way and policymakers in the UK and the US following suit. Financial institutions, including pension funds, are increasingly being asked to report on climate change risks and opportunities in their investment portfolios, driving up demand for ESG-friendly solutions.

fresh record of $700bn, with cumulative green bond issuance surpassing the long-awaited $1trn milestone.

he rising prominence of environmental and social considerations in fixed income investing has been reflected in the growing issuance of green, social and sustainability (GSS) bonds. In 2020 alone, GSS bond issuance reached a

Why the ‘tooth and nail’ fight for ESG data is key to the future of sustainable bonds

The future of the sustainable fixed income market is looking bright following a renewed focus on environmental and social issues post-Covid-19. But the industry has a long way to go to overcome challenges when it comes to integrating ESG metrics into investment strategies

With many nations, including the UK, committing to reach net zero by 2050, and some setting ambitious interim targets, the need for private capital to help achieve this goal has also never been greater. And while issuance has increased exponentially, much more is needed to meet the UN Sustainable Development Goals (SDGs) and the aims of the Paris Agreement.

Indeed, such is the drive towards climate change transitions and net zero, capital is the single largest need for sustainability, according to Ketish Pothalingam, “Trillions of dollars are needed to get ourselves aligned with the Paris agreement and achieve SDG goals.”

This is particularly important in a post-Covid-19 environment, as the pandemic has accelerated existing trends, and driven both demand for ESG-focused credit from investors and the need to finance a sustainable recovery. “In Europe, we have seen the central bank announce a €750bn recovery package, ~30% of which is set to be financed through green bond issuance.”

Samuel Mary, ESG research analyst, says: “We have seen a number of issuers developing Covid-19 related sustainability bonds, banks lending to companies particularly hit by the pandemic, or pharma companies developing vaccines or providing related spending to help with the Covid-19 response.”

However, incorporating ESG into fixed income strategies is not without its challenges. The biggest of these, according to Pothalingam, is the availability and quality of data. Over the years, this issue has been particularly prominent in the fixed income space, though Pothalingam says the situation is getting “steadily better”.

The data challenge

My starting point is that not everything that matters can be measured

Whilst the move to net zero is resulting in record issuance of GSS bonds, the pandemic’s refocusing of investors’ attention on issues such as health and safety in the workplace, inclusive economies and healthy communities has resulted in a huge increase in the issuance of social bonds. During 2020, the size of the social bond market alone sky-rocketed 1,017% to $249bn, and there is room for further growth.

Favourable landscape

This demand is driving a favourable landscape for fixed income investors keen to make a difference with their investments. In particular, Mary says the ESG fixed income market has continued to broaden over the last 18 months. ESG-labelled debt is being issued by sovereigns in both developed and emerging markets, as well as the high yield space, while the traditional green bond space and sustainability-linked bond issuance is also growing.

“If we take a forward-looking approach, we are likely to see similar momentum for other parts of the market, such as green ABS, for example,” says Mary.

The pandemic’s refocusing of investors’ attention on issues has resulted in a huge increase in the issuance of social bonds.

the new Aviva Investors Climate Transition Real Assets Fund. Mark Meiklejon, head of real assets global investment specialists at Aviva Investors, explains that pension schemes are increasingly looking to achieve their return objectives while also meeting explicit ESG targets set by trustees and the regulator.

“There is a huge impetus to invest in real assets, since you get this perfect storm from a scheme point of view because of the low correlation [to other asset classes], higher inflation protection, and higher return potential,” he says. “It’s a key thematic from a client perspective, being able to access a product that can help with both [returns and ESG commitments].”

Managed by a team from across Aviva Investors’ Real Assets platform, the new Aviva Investors Climate Transition Real Assets Fund targets a return of net 8% annually over rolling five-year periods, investing in direct real estate, direct pan-European infrastructure assets, and direct timber and forestry assets, with some limited exposure to liquid assets. The fund is aimed primarily at UK defined contribution (DC) pension schemes, alongside wider institutional and advisory wholesale investors across Europe.

Targeting assets that help accelerate the transition to net zero is a key aim for the fund, which seeks to reach net zero by 2040, while also adhering to explicit social goals and reporting carbon savings year-on-year. The real asset sector holds multiple opportunities for the fund to achieve these targets.

A liquid structure

Meiklejon believes the fund’s structure makes it a perfect vehicle for pension schemes. The vehicle is structured as a UK Non-UCITS Retail Scheme (NURS) and will be a Fund of Alternative Funds (FAIF), investing into underlying asset-class specific Luxembourg RAIF vehicles, some liquid assets and forestry. The fund has been seeded with approximately £425m which, combined with the ability to leverage up to 50% of loan to value, will generate approximately £950m of investment capital to deploy.

The emphasis of the strategy is, however, multi-faceted, with the fund one of the first of its kind in the industry to offer investors direct investment in nature-based solutions. For example, real asset investments will be supplemented by proactive “afforesting” – planting new forest to generate not just an investment return, but also a direct carbon benefit.

Having launched the fund in the middle of the pandemic, Aviva Investors is acutely aware of how the crisis has affected real assets sectors. Within real estate, offices and retail spaces are going through a structural change, while sectors like logistics, data centres and power storage have grown exponentially. Within infrastructure, the focus is continually shifting from transport sectors towards renewables and the pandemic has only accelerated this.

And given recent issuance figures, it seems the bond market is this year stepping up efforts to offer some of this much needed funding.

Climate-related regulation is increasing, with Europe leading the way.

“We are fighting tooth and nail for standardisation of data,” Pothalingam says. “It will make all our lives easier, especially from a reporting perspective.”

PIMCO has a dedicated team of ESG analysts who analyse the ESG merits of each issuer using various quantitative and qualitative factors and assign a proprietary score for each of the ‘E’, ‘S’ and ‘G’ pillars.

“We are trying very hard to get standardisation as a key part of the process going forward, and regulation will be an important part of that, especially with regard to disclosing data.”

There are many driving forces behind the growth of this area of the fixed income market

“We have seen a number of issuers developing Covid-19 related sustainability bonds, banks lending to companies particularly hit by the pandemic, or pharma companies developing vaccines or providing related spending to help with the Covid-19 response”

Meanwhile, regulators are increasingly placing more emphasis on the quality of reporting. Reporting against the Task Force on Climate-related Financial Disclosures (TCFD) is set to become mandatory in the UK for publicly quoted companies, large private companies and Limited Liability Partnerships (LLPs).

The International Financial Reporting Standards (IFRS) Foundation is also developing a new Sustainability Standards Board, with the intent of adopting a similar climate disclosure standard. With the support of the regulators, the quality of data is set to continue improving.

The 26th UN Climate Change Conference of the Parties (COP26) in Glasgow this year set out to accelerate climate action and push companies to make net-zero commitments, set regular targets for achieving these and report on their progress. With these driving forces behind it, the ESG fixed income space is set to become broader and more sophisticated in the years to come.

His comments are backed by the Energy Transition Commission (ETC) report published in September 2020, which noted additional investment of $1trn-$2trn a year globally will be required to achieve the 2050 net zero target.