IN PARTNERSHIP WITH

For more information visit: www.incisiveworks.com

This digital experience is an Incisive Works product © 2023 Incisive Business Media (IP) Limited

Real assets and the net-zero pathway

xxxxxxx

xxxxxxxxxxx

The sustainable forces driving change in real assets

The real asset green premium explained

hile conditions for fixed income markets were extremely tough in 2022, there were hopes that 2023 would be different. However, bond yields have

trended higher again in recent months and remain volatile, despite optimism that central banks’ hiking cycles are reaching their peaks. There may still be volatility ahead, but at today’s starting yield levels, which are historically strongly correlated with returns, there are promising opportunities for the discerning investor.

W

“Net zero commitments are set to revolutionise the world of long-dated real assets”

scroll

FIXED INCOME

Mark Meiklejon on the Aviva Investors’ Climate Transition Real Assets Fund

How can pension funds use ESG to futureproof portfolios?

Professional Investors Only

Featured in this Spotlight

Click on the plus icons for more information

Ketish Pothalingam Portfolio Manager, EVP

Ketish is a member of PIMCO’s ESG team, focusing on corporate credit and global bond ESG portfolios

Samuel Mary ESG Research Analyst, SVP

Samuel focuses on the integration of ESG factors into PIMCO's portfolio management and credit research

Sectors in focus: real estate, banking and more

Spotlight on: GIS Income Fund

'Bend but don't break': the portfolio view

Big picture outlook with Dan Ivascyn

Indeed, a major risk now is of missing out on the returns that could be on offer, whether by staying too heavily in equities or by being too comfortable in very safe government bonds.

"People are pretty happy right now because they’re getting so much yield on their government bonds. But if they go out just a little bit more in the risk spectrum, they can pick up several hundred basis points in yield"

This digital experience is an Incisive Works product © 2021 Incisive Business Media (IP) Limited

Disclaimer Past performance is not a guarantee or a reliable indicator of future results.The Fund will be actively managed in reference to the Bloomberg Barclays MSCI Global Green Bond Index as further outlined in the Prospectus and Key Investor Information Document. Performance and fees Past performance is not a guarantee or a reliable indicator of future results. Performance figures are presented net of management fees commissions, other expenses, and the deduction of actual investment advisory fees; but do not reflect the deduction of custodial fees. The "net of fees" performance figures above also reflect the reinvestment of earnings. All periods longer than one year are annualized. Separate account clients may elect to include PIMCO sector funds in their portfolio; sector funds may be subject to additional terms and fees. Charts Performance results for certain charts and graphs may be limited by data ranges specified on those charts and graphs; different time periods may produce different results. ESG Socially responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgment exercised, by PIMCO will reflect the beliefs or values of any one particular investor. Information regarding responsible practices is obtained through voluntary or third-party reporting, which may not be accurate or complete, and PIMCO is dependent on such information to evaluate a company’s commitment to, or implementation of, responsible practices. Socially responsible norms differ by region. There is no assurance that the socially responsible investing strategy and techniques employed will be successful. Past performance is not a guarantee or reliable indicator of future results. For professional use only The services and products described in this communication are only available to professional clients as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness.The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E) and PIMCO Europe GmbH Irish Branch (Company No. 909462) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch and Spanish Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; and (3) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication.| PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2) . The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser.

ast year saw record issuances of green, social and sustainability (GSS) bonds. 2021 has been similar, reaching several new records. At the

same time, climate risk has become a key consideration to ensure stability of financial returns going forward as issuers and investors alike grapple with physical and transition risks.

MARKETING COMMUNICATION

There are promising opportunities in fixed income

Time to get on board?

The role of advisers in educating clients about responsible investment

Marketing Communication This is a marketing communication. This is not a contractually binding document and its issuance is not mandated under any law or regulation of the European Union or the United Kingdom. This marketing communication does not include sufficient detail to enable the recipient to make an informed investment decision. Please refer to the Prospectus of the UCITS and to the KIID before making any final investment decisions. For professional use only The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules and as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. The views contained herein represent those of the authors and not necessarily those of PIMCO. Views and opinions may be subject to change without notice Additional Information/Documentation A Prospectus is available for PIMCO Funds and UCITS Key Investor Information Documents (KIIDs) (for UK investors) and Packaged retail and insurance-based investment products (PRIIPS) key information document (KIDs) are available for each share class of each the sub-funds of the Company. The Company’s Prospectus can be obtained from www.fundinfo.com and is available in English, French, German, Italian, Portuguese and Spanish. The KIIDs and KIDs can be obtained from www.fundinfo.com and are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). In addition, a summary of investor rights is available from http://www.pimco.com .The summary is available in English. The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. PIMCO Global Advisors (Ireland) Limited can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.” RISK Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. High yield, lower-rated securities involve greater risk than higher rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Swaps are a type of derivative; swaps are increasingly subject to central clearing and exchange-trading. Swaps that are not centrally cleared and exchange-traded may be less liquid than exchange-traded instruments. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Past performance does not predict future returns This material contains the current opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser.

Resilience: the secular theme shaping the future

Marketing Communication Professional Investors Only

‘Stagnation’ – a mixed outlook for the UK

Two underappreciated sectors offering potential

Aiming high: don’t leave returns on the table

BROWSe OTHER CHAPTERS

READ THE FIRST ARTICLE >

Read on to hear our views on this challenge in the first chapter of this guide. We’ll then analyse two sectors with untapped potential, before assessing the outlook for the UK and outlining PIMCO’s approach to income investing.

Spotlight on: PIMCO’s balanced approach to income investing

Josh Anderson, PIMCO Portfolio Manager

Marketing Communication This is a marketing communication. This is not a contractually binding document and its issuance is not mandated under any law or regulation of the European Union or the United Kingdom. This marketing communication does not include sufficient detail to enable the recipient to make an informed investment decision. Please refer to the Prospectus of the UCITS and to the KIID before making any final investment decisions. For professional use only The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules and as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. The views contained herein represent those of the authors and not necessarily those of PIMCO. Views and opinions may be subject to change without notice Additional Information/Documentation A Prospectus is available for PIMCO Funds and UCITS Key Investor Information Documents (KIIDs) (for UK investors) and Packaged retail and insurance-based investment products (PRIIPS) key information document (KIDs) are available for each share class of each the sub-funds of the Company. The Company’s Prospectus can be obtained from www.fundinfo.com and is available in English, French, German, Italian, Portuguese and Spanish. The KIIDs and KIDs can be obtained from www.fundinfo.com and are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). In addition, a summary of investor rights is available from http://www.pimco.com .The summary is available in English. The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. PIMCO Global Advisors (Ireland) Limited can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.” RISK Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. High yield, lower-rated securities involve greater risk than higher rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Swaps are a type of derivative; swaps are increasingly subject to central clearing and exchange-trading. Swaps that are not centrally cleared and exchange-traded may be less liquid than exchange-traded instruments. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Past performance does not predict future returns This email contains the current opinions of the manager and such opinions are subject to change without notice. This presentation has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this presentation may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser.

Bonds are back, although risks persist

or BROWSe OTHER CHAPTERS

Spotlight on: The GIS Income Fund

Josh Anderson, Portfolio Manager

SPOTLIGHT

MENU

HIDE X

now is of not allocating enough to fixed income.

quity-like returns from high quality bonds? Two years ago, that was a very far-fetched idea. Today, however, things are very different. Indeed, it is a measure of how much circumstances have changed that the greater risk

E

“The fund has consistently outperformed the IA Sterling Strategic Bond sector”

Investors risk missing out if they don’t take advantage of the opportunities on offer in fixed income

“The comparison that investors have to make is between the expected returns in fixed income, which have increased substantially, or those from equity markets, which haven’t to the same extent,” says Alfred Murata, Portfolio Manager of the PIMCO GIS Income Fund.

None of this is to say that the environment for fixed income is risk-free. There are still landmines out there that require a measured approach and a focus on resilience.

Aftershocks

“Putting it simplistically,” he explains, “if bonds are yielding 4% then it might be attractive to invest in equities if you think the expected return is going to be 8%. But if bonds are yielding around 7%, as they are now, then you ought to be looking at, say, 10 or 11% from equities. That sort of return is much harder to find.”

“We see this as totally consistent with the way our credit analysts think”

But like many asset managers, over the last decade, PIMCO has been intensifying its focus on ESG issues. A decade ago, it became a signatory of the UN Principles for Responsible Investment (UN PRI) and established a dedicated ESG team. From 2017, PIMCO began launching dedicated ESG-labelled bond products and now offers a full suite, including the GIS Global Bond ESG Fund, the GIS ESG Income Fund and the GIS Climate Bond Fund.

the world of investing for several years, but the concept is not new for PIMCO. The bond house first offered clients a socially responsible version of one of its key funds as far back as 1991.

he idea of investing with environmental, social and governance (ESG) principles in mind has been gaining traction in

T

“The more generic, plain vanilla assets have seen a lot of support from central banks over the past year, so the valuations of these assets are not as compelling today,” explains Murata. “You have to work harder to generate attractive returns in this environment.”

Fixed income investors also risk missing out if they only stick to the safest bonds, warns Josh Anderson, fellow PIMCO GIS Income Portfolio Manager.

Significant reduction in CO2 emissions

Yields have increased meaningfully across sectors

BACK

NEXT

1 / 2

“We think this is a very exciting time for these markets after the recent sell-off,” he says. “Things can certainly get worse before they get better, but for an intermediate-to-longer-term investor with income needs, we are very excited about the opportunity set.”

< PREVIOUS ARTICLE

NEXT ARTICLE >

“People are pretty happy right now because they’re getting so much yield on their government bonds,” he says, “but if they go out just a little bit more in the risk spectrum, they can pick up several hundred basis points in yield.

“I think there's an under-appreciation of how much potential total return and yield investors are going to give up by being in the safe government securities. Over a three or four-year period, staying very, very safe can add up to a lot of return left on the table.”

“In our minds, the impact of a lot of the rate moves hasn’t fully played out,” says Anderson. “Last year there was a huge shock to the bond market, and those reverberations are still going on. Particularly in commercial real estate, and in the credit markets, where we continue to see defaults.”

Or as Murata puts it: “We have higher yields today but we also have less support from central banks. That can lead to more volatility in the marketplace.”

That said, however, heightened volatility is not necessarily a bad thing. “That volatility could impact some investors negatively, but it could also provide tremendous opportunities,” he says.

In this sort of environment, PIMCO’s approach can come to the fore. The PIMCO GIS Income Fund seeks to find attractive, risk-adjusted opportunities that may potentially do well in a variety of conditions. “We call this philosophy ‘bend but don’t break’,” says Anderson. “This means there’s a dispersion of return outcomes but we’re targeting assets that are well placed to potentially perform in relative terms in different economic circumstances.”

Relative outperformance in a range of conditions

This approach has been vindicated in recent, challenging times. While nine out of the top 10 competitors by AUM in the strategic bond funds space posted negative returns over the past three years, PIMCO’s GIS Income Fund was the only one that managed to earn a positive return, albeit a modest one.

The fund has also consistently outperformed the IA Sterling Strategic Bond sector over a three-year time period.

We’ll take a closer look at the sectors it is targeting in the next chapter.

“Volatility could impact some investors negatively, but it could also provide tremendous opportunities”

Alfred Murata, Portfolio Manager

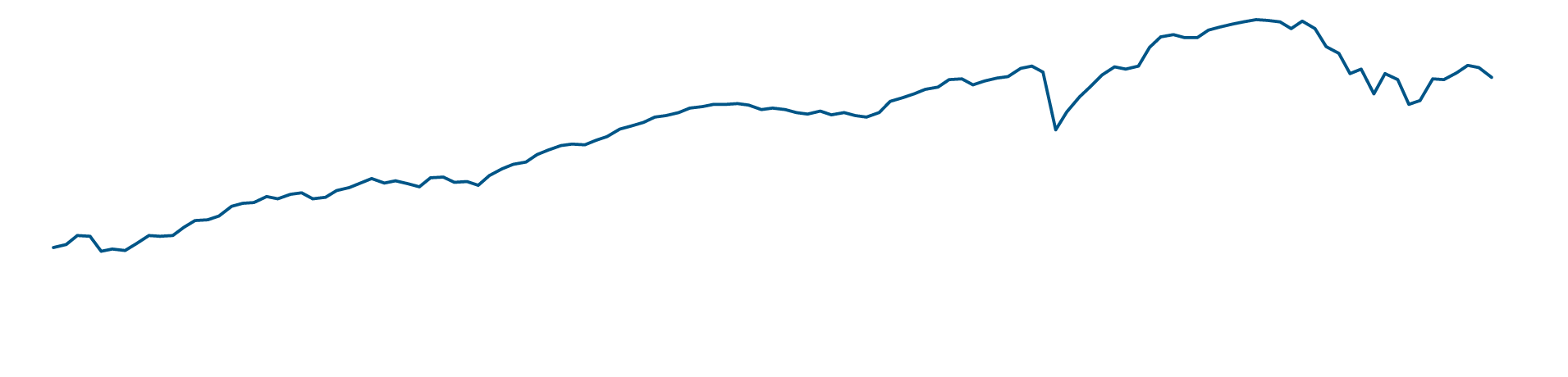

GIS Income fund vs. the top 10 competitors by AUM in the IA Sterling Strategic Bond sector

The PIMCO Income Fund provides superior three-year cumulative returns (%)

Share value can go up as well as down and any capital invested in the Fund may be at risk. The Fund may use derivatives for hedging or as part of its investment strategy which may involve certain costs and risks. For more details on the fund’s potential risks, please read the Key Investor Information Document. As of 30 September 2023. Drawdowns as from July 2018 to September 2023. Performance is shown for the Institutional, Income class, GBP shares, annualized and net of fees. SOURCE: PIMCO For illustrative purposes only. Past performance does not predict future returns. All periods longer than one year are annualised.

1.7%

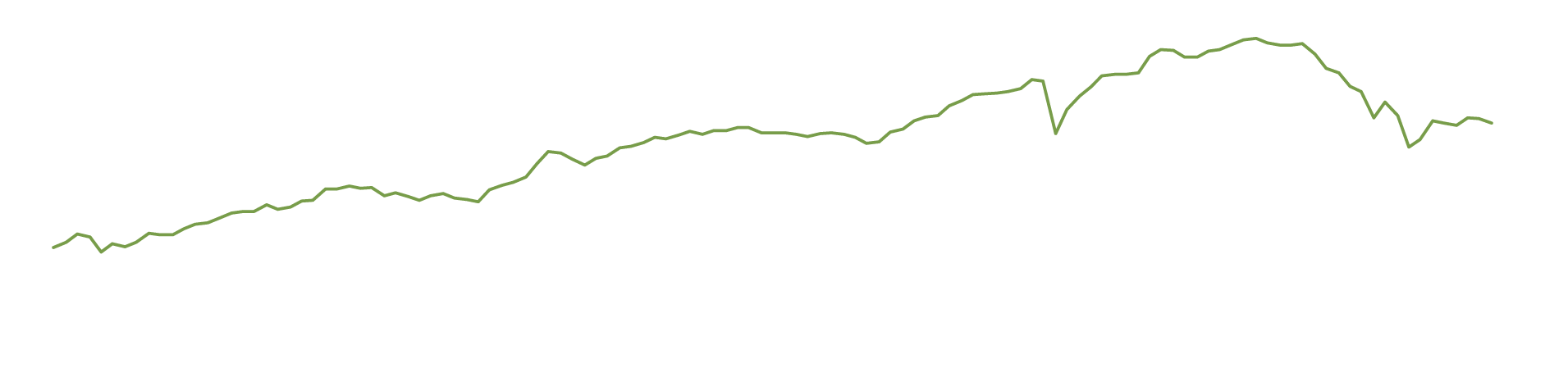

PIMCO’s GIS Income Fund has exhibited higher risk-adjusted returns and better downside protection than the IA Sterling Strategic Bond Sector

Growth of £100

As of 30 September 2023. Source: PIMCO, Morningstar. Performance is shown for the institutional class, GBP shares, annualized and net of fees. Past performance does not predict future returns. All investments involve risk including the possible loss of capital.

GIS Income (GBP-Hedged)

IA Sterling Strategic Bond

Sources.

(1) As of 30 September 2023. (2) There is no guarantee that the fund will achieve any forecasts or objectives as stated herein.

1

2

Opportunity with a lower risk profile

Indeed, it is not just the potential financial returns that make fixed income attractive right now, but the ability to do so with a lower risk profile. This, explains Ivascyn, stems from a substantial rebalancing of public and private market valuations – the former having outstripped the latter significantly in recent times.

Indeed, PIMCO’s recent Secular Forum highlighted the reverberations we are likely to see as economies transition to tighter monetary policy, calling it “the aftershock economy”.

Share value can go up as well as down and any capital invested in the Fund may be at risk. The Fund may use derivatives for hedging or as part of its investment strategy which may involve certain costs and risks. For more details on the fund’s potential risks, please read the Key Investor Information Document. As of 30 September 2023. Drawdowns as from July 2018 to September 2023. Performance is shown for the Institutional, Income class, GBP shares, annualized and net of fees. SOURCE: PIMCO For illustrative purposes only. Past performance does not predict future returns. All periods longer than one year are annualized.

As of 30 Sept 2023. Source: PIMCO, Morningstar. Performance is shown for the institutional class, GBP shares, annualized and net of fees. Past performance does not predict future returns. All investments involve risk including the possible loss of capital.

The fund has also consistently outperformed the IA Sterling Strategic Bond sector over a 5 year time period.

Relocating the fixed income opportunity — the case for going global

Blue bonds: long-awaited innovation or yet to make a splash?

Banking and real estate look appealing as PIMCO’s GIS Income Fund seeks wider spreads with lower credit risk

Sustainable investment examples

PREV

“PIMCO’s scale allows it to drive positive change”

“In theory a bank could be taking these deposits, investing in short-term government bonds at a 5% or even higher yield, and yet be passing on close to zero to depositors.”

“Even with a 20% drop in housing, many of these securities can still be very well-protected”

Company B SECTOR: Packaging MATURITY: September 2028 COUNTRY OF DOMICILE: Ireland Green bond proceeds to be allocated towards expenditures relating to energy efficiency projects and manufacturing of sustainable packaging. PIMCO had a 1x1 call with the company to discuss best practices for ESG bond disclosure and reporting. We recommended that the company consider leveraging additional environmental indicators to quantify the environmental impacts of its sustainable aluminium products. PIMCO also shared guidance on sustainable bond issuance and examples of lifecycle impact assessments.

green bond

Company A SECTOR: Real estate finance MATURITY: 15 April 2031 COUNTRY OF DOMICILE: United States This bond focuses on energy efficiency, green buildings, infrastructure and renewable energy-generation projects. Following the issuance of the bond, PIMCO also engaged with the company to request the creation of a green bond framework to provide a deeper level of assurance to market participants. We suggested they include language regarding exclusionary categories given their investments in the natural gas value chain.

Company C SECTOR: Materials MATURITY: 15 January 2032 COUNTRY OF DOMICILE: United States The company’s second sustainability-linked bond (SLB) includes key performance indicators centred on reducing its industrial water-withdrawal intensity by the end of 2026 and increasing the representation of women in leadership positions to 30% or more by 2025. After passing up the opportunity to invest in the company's initial SLB in 2020, PIMCO met with management to discuss their ESG action plan and provide recommendations for improvement. Following our discussion, the company announced more ambitious ESG targets and issued this second SLB, where PIMCO participated.

sustainability-linked bond

1 / 3

2 / 3

3 / 3

Samuel Mary, ESG research analyst

“Xxxxxxxxxxxx xxxxxx xxxx xx xxx xxx xxxx xxxxx xxxxxxxxxx xxxxxx xxxx xxx xxx xxxxx xxxxxx xxx xxxxxxx xxxx xxxxxxxxx xxxxxxx xxxx xxxxxxx”

Xxxxxx Xxxxxx, Xxxxxx

Sweet spots in real estate

We have specifically been investing in legacy NAMBSs that were issued before the global financial crisis. The underlying borrowers here have benefited from more than a decade of house price appreciation, and the loan to valuation on many of these is now less than 50%. So even if you have a downturn in the housing market, you still expect to get positive yields on a hold-to-maturity basis.

What is your “bend but don’t break” philosophy and where does it take you in practice?

Alfred Murata: “Bend but don’t break” means we’re trying to focus on positions where there may be some price fluctuations in volatile markets but where there is unlikely to be a long-term permanent impairment of capital. One of those sub-sectors has been non-agency mortgage-backed securities (NAMBSs). These are bonds that are backed by residential loans but not guaranteed by the government. As an investor, you’re depending on the cash flow from the underlying loans to pay you back.

“We’re focusing on positions where there may be some price fluctuations but where there is unlikely to be a long-term permanent impairment of capital”

2013: Taper tantrum

Event description

Date

Time period

YTM

Peak yield (%)

Returns following peak yields (%)

2016: Oil crash

2018: Rising rates

2020: Covid-19

9/13/2013

1/20/2016

11/27/2018

3/23/2020

6.27

5.93

6.69

8.16

1-year

10.94

9.67

8.83

23.83

3-year

6.54

5.96

6.03

–

5-year

5.63

6.55

As of 31 October 2022. Source: PIMCO. Performance is shown as an annualized return for the institutional class shares after fees. For illustrative purposes only.

Past performance is not a guarantee or a reliable indicator of future results

PIMCO GIS Income Fund has outperformed higher-risk assets

PIMCO GIS Income Fund – Historic Returns Following Peak Yields

4/ 4

3/ 4

2/ 4

1 / 4

As of 30 September 2022. Top left chart is as of 31 July 2022. Source: PIMCO, S&P Global. For illustrative purposes only. *CLTV: Combined loan-to-value ratio, which is the ratio of all loans secured by a property to the property's value.

Fund is diversified across a variety of income-generating ideas

though interest rates have been increased dramatically, many banks are not passing them along to depositors,” says Alfred Murata.

his year’s bank crises were certainly dramatic. But looking forward, PIMCO is confident that we are through the worst. A major reason for this is that higher interest rates should be supportive for the banks’ profitability. “Even

Putting aside the ethics of this from a depositor perspective, it adds up to a positive outlook for the banking sector. Yet at present, some investors aren’t grasping the opportunity. They’re being put off by the banks’ mark-to-market calculations, which are currently showing a loss due to investments the banks made when rates were low, such as securities or loans.

Murata argues it is a mistake to focus on this calculation and not the banks’ forward profitability. “I think that as time passes, the banks’ profitability could offset these losses, which in any case have not actually been realised,” he says. “And the lending facilities provided by the US Federal Reserve should hopefully tide the US banks over.”

Of course, there is still a need to be vigilant and cautious. As a result, the firm is focusing on senior debt from the larger, systemically important banks, as these are the most likely to potentially benefit from government support if they were to run into trouble.

The other key focus for the PIMCO GIS Income Fund at present is real estate. Indeed, Josh Anderson says the whole AAA and AA structured-product market is very attractive.

“Spreads are historically wide,” he says. “They’re anywhere from 50 to 100, maybe even 150 basis points wider than they were pre-Covid.

“One of the reasons for this is that the banks, particularly regional ones, haven’t been buying the AAA structured products that we buy due to their mark-to-market issues. Neither has the Federal Reserve in the US. That’s driving a portion of the spread widening and is beneficial for us.”

At this lower end of the risk spectrum, PIMCO believes that US agency mortgage-backed securities are particularly attractive given current valuations. The residential loans packaged within these bonds are guaranteed by government-sponsored enterprises such as Fannie Mae, Freddie Mac and Ginnie Mae, offering a great deal of risk protection.

“Real estate is one asset class that we think is particularly compelling today”, says Anderson. “It benefits from the fact that while the market technicals are poor, these securities can provide compelling value for the investor that has a longer-term holding period.”

That’s not to dismiss non-agency mortgage-backed securities, however, which PIMCO also sees as an important opportunity. “As an asset class we think it will be very resilient, even if you have a downturn in housing,” says Anderson.

“In the US,” he continues, “many of these securities have a loan-to-value ratio of less than 50%. So even with a 20% drop in housing, they can still be very well-protected.

“We're seeing similar opportunities in the UK as well. We think the residential space will be very well-protected even during a downturn in housing.”

As for the PIMCO GIS Income Fund’s overall positioning, Murata says it has upgraded to a neutral view on interest rate risk, compared to the cautious view of a couple of years ago.

Duration and credit risk positioning

“We’ve been adding duration to the portfolio,” he says. “With the significant repricing that's taken place, we think that there's a lot more value in US and UK duration.”

However, there are still enough reasons to retain some circumspection. “Although inflation is on a downward trend, there is still substantial risk that the next few inflation prints could be higher than expected,” says Murata. “If that were to occur, it's likely that central banks will end up being more hawkish than anticipated, and we could have a widening in credit spreads.

“Given that our mandate is to generate a consistent level of income while trying to protect against downside risk, we think that it makes sense to just have a neutral view on duration rather than a more elevated one.”

As for credit risk, Murata says the fund is relatively cautious. “So far the economy has still performed very well, despite the rise in rates,” he says. “But we think that as time passes – as interest rates continue to rise and funding costs continue to increase – that is going to put pressure on the economy.”

Nevertheless, there are still areas where the fund is looking to spot opportunities. “We're trying to find positions where spreads are at very wide levels but which we think are not going to have significant credit risk in a downside economic scenario.”

“Spreads are anywhere from 50 to 100, maybe even 150 basis points wider than they were pre-Covid”

quity-like returns from high quality bonds? Two years ago, that was a very far-fetched idea. Today, however, things are very different.

Indeed, it is a measure of how much circumstances have changed that the greater risk now is of not allocating enough to fixed income.

Recessionary conditions would be bad news for many but could potentially mean attractive returns for fixed income markets and the PIMCO Select UK Income Bond Fund

Achieving net zero emissions is a key engagement theme for PIMCO. The firm has engaged with more than 20 global banks on implementing their carbon emissions strategies and aligning with the Paris Agreement.

BACKGROUND Company C is a British mutual financial institution. The bulk of the indirect GHG emissions created across their value chain (known as scope 3 emissions) relates largely to their mortgage portfolio. ENGAGEMENT PIMCO engaged with management to help shape their new sustainability KPIs, specifically on setting targets on net-zero portfolio emissions and improving the Energy Performance Certificates ratings (EPCs) for the assets secured by their mortgage lending. PROGRESS TO DATE In 2021, Company C pledged to go net-zero by 2050, joining the Net-Zero Banking Alliance (NZBA) and the Glasgow Financial Alliance for Net Zero (GFANZ). They also set a target for their mortgage portfolio to reach 50% of C-rated or above by 2030 in line with our recommendations.

BACKGROUND A major US utility holding company with operations in eight Western and Midwestern states, Company B serves 3.7 million electricity customers and 2.1 million natural gas customers. The company has committed to generating 100% carbon-free electricity by 2050 as well as an 80% reduction in GHG emissions by 2030. ENGAGEMENT PIMCO has engaged company management over several years regarding their green bond programme, climate disclosure and climate strategy. PIMCO encouraged alignment with the International Capital Markets Association Green Bond Principles as well as PIMCO’s Best Practice Guidance for Sustainable Bond Issuance. PIMCO emphasised the importance of transparency in green bond eligibility criteria and impact reporting, as well as firm-wide alignment with the Paris Agreement. PROGRESS TO DATE In autumn 2020, Company B published its first green bond impact report largely following suggested best practices. A year later, Company B published its first standalone sustainable financing framework, setting out the full list of eligible categories, criteria and examples, along with a second-party option provided by S&P.

Emerging markets

When we look at emerging markets from a global perspective, valuations look quite attractive. But emerging markets don’t tend to do very well when you have a significant central bank tightening cycle across the globe. There’s also a lot of idiosyncratic uncertainty with emerging markets, tied to US or Western friction with China, Chinese growth questions, uncertainty in Eastern Europe and various elections across Latin America.

The bottom line is that we think emerging markets will be a good diversifier for clients over the course of the next few years, but our exposure remains low. We have reduced our position over the course of the last year and our focus is almost entirely on the higher quality and more liquid segments of the emerging markets.

We have small emerging markets currency exposures and our bond exposures are almost always in sovereigns and quasi-sovereigns. We’re very hesitant to move into emerging market corporates, frontier markets and lower-rated segments in the emerging markets opportunity set.

Seek Yield and diversification via select exposures within emerging markets

Focus on higher quality and more liquid areas of the emerging markets. Mostly sovereign or quasi-sovereign positions, very limited exposure to corporates.

Scale positions small given the potential for volatility from idiosyncratic and geopolitical events.

Country breakdown (PBE)

As of 31 October 2022. Source: PIMCO. EM Index Product is exposure to the ICE CDX EM Index. "PBE" denotes "Percent Bond Exposure".

Developed markets

However, with the types of investments we’re focusing on within this strategy, their performance is not going to be tied in a significant way to house price action because we’re not buying new originations. As mentioned before, we’re focused on legacy non-agency mortgage-backed securities, so our stock of exposures are very, very seasoned investments that have benefited from significant house price appreciation not only since the Covid shock but over the last 15 years or so.

The US dollar looks very, very expensive relative to other global currencies. We may have more of a negative dollar exposure at some point in the future, but given the dollar’s momentum and its flight-to-quality attributes, we’re hesitant to be more aggressive in that space. Right now we have a relatively small position in non-dollar currencies: specifically some high quality emerging markets and a few developed markets.

AMBSs benefit from either a direct government guarantee or via an agency of the US federal government. That makes them very high quality, and they are currently at near record wide spreads versus Treasuries or other high-quality alternatives. AMBSs have widened because they tend to not do so well in periods of heightened interest rate volatility. There are also a lot of AMBSs on the Federal Reserve balance sheet that may need to come back to the marketplace over the course of the next few years.

Historically, we have at times had significant positions in AMBSs. This is fairly atypical for income-oriented strategies because AMBSs’ high quality means they tend to have lower yields than high-yield bonds, for example.

Agency mortgage-backed securities

“Interest rates are expected to stay restrictive in the UK overall, but they may start falling at some point next year, which would raise bond values and allow holders to potentially benefit from capital appreciation. And even if interest rates don’t fall, we’d expect bonds to offer a degree of safety and a predictable income compared to equities.”

“Given how much fixed income has repriced,” he says, “if you have stagnation, a mild recession or modest growth, then you could do very well.

e expect economic stagnation and a mild recession over the coming year in the UK.” That may not be great for the UK as a whole, but as PIMCO’s Josh Anderson explains, it ought to be for fixed income markets.

The rates picture will of course be heavily influenced by the UK’s inflation trajectory. To date the UK has been lagging behind the US in getting inflation under control, but Alfred Murata, lead portfolio manager on the PIMCO Select UK Income Bond Fund, believes there is room for cautious optimism.

“In the US, the Fed raised rates aggressively and now inflation has come down dramatically,” he says. “This dynamic has taken longer to play out in the UK, but I think the Bank of England has now caught up.”

Murata adds that he now sees a steady fall in UK inflation over time. “Nothing dramatic,” he says, “but just a continued weakening over the coming year, given the modest economic environment that we expect.”

For the PIMCO Select UK Income Bond Fund, this represents an opportunity to add duration, says Murata. “As rates have been rising in the UK, and expectations for the Bank of England to continue to raise rates have as well, we've been adding some duration to the portfolio. Today I'd say we're cautiously positioned whereas before we were extremely cautiously positioned.”

The case for duration

Indeed, Murata says that as time passes, the case for adding duration in the UK should become more compelling. He’s also heartened by the fact that the UK has a much faster linkage between the rise in interest rates and the cost of mortgage debt than the US.

“In the US, many people have a 30-year fixed rate mortgage,” he says. “So even if the Federal Reserve raises rates, many people are not going to need to refinance their mortgage. In the UK, there's going to be a faster flow-through into the economy as a whole.”

The Fund is focusing on areas where spreads have widened significantly but the credit risk hasn’t increased substantially. One such area is UK residential mortgage-backed securities that are very seasoned, meaning the homeowners have built up sufficient equity to act as a buffer in the event of a housing dip.

“Over the past decade or so, we've seen continued liquidations from the UK asset resolution that took over the assets of some of the banks during the global financial crisis,” says Murata. For example, the mortgage assets of Northern Rock have been liquidated over time and that's provided a tremendous opportunity for us in the UK income portfolio.”

Central bank policy expected to stay restrictive

As of 30 September 2023. Source: Bloomberg, PIMCO The views and expectations expressed are those of PIMCO. There can be no guarantee that the trends mentioned above will continue. Statements concerning financial market trends are based on current market conditions, which will fluctuate.

Fed Funds Rate

BoE Base Rate

The path to disinflation is likely to remain bumpy

ECB Deposit Rate

Performance: PIMCO Select UK Income Bond Fund

As of 30 September 2023, subject to change. Source: PIMCO. *Benchmark: Bloomberg Sterling Agg 1-10yr Bond Index. The fund is actively managed in reference to the Bloomberg Sterling Agg 1-10yr Bond Index as further outlined in the prospectus and key investor information document. Duration based on PIMCO internal calculations. Past performance is not a guarantee or a reliable indicator of future results. All periods longer than one year are annualised.

Portfolio (before fees)

Benchmark

Institutional Class, Accumulation Shares

“

PIMCO SELECT FUNDS Past performance is not a guarantee or a reliable indicator of future results. PIMCO Select Funds plc is an umbrella type open-ended investment company with variable capital and with segregated liability between Funds incorporated with limited liability under the laws of Ireland with registered number 480045. The information is not for use within any country or with respect to any person(s) where such use could constitute a violation of the applicable law. The information contained in this communication is intended to supplement information contained in the prospectus for this Fund and must be read in conjunction therewith. Investors should consider the investment objectives, risks, charges and expenses of these Funds carefully before investing. This and other information is contained in the Fund's prospectus. Please read the prospectus carefully before you invest or send money. For additional information and/or a copy of the Fund's prospectus, please contact the Administrator: State Street Fund Services (Ireland) Limited, Telephone +353-1-776-0142, Fax +353-1-562-5517 Additional Information/Documentation A Prospectus is available for PIMCO Funds and Key Investor Information Documents (KIIDs) are available for each share class of each the sub-funds of the Company. The Company’s Prospectus can be obtained from www.fundinfo.com and is available in English, French, German, Italian, Portuguese and Spanish. The KIIDs can be obtained from www.fundinfo.com and are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). In addition, a summary of investor rights is available from www.pimco.com .The summary is available in English. The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. PIMCO Global Advisors (Ireland) Limited can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive. RISKS Credit and Default Risk A decline in the financial health of an issuer of a fixed income security can lead to an inability or unwillingness to repay a loan or meet a contractual obligation. This could cause the value of its bonds to fall or become worthless. Funds with high exposures to non-investment grade securities have a higher exposure to this risk. Currency Risk changes in exchange rates may cause the value of the investments to decrease or increase. Derivatives and Counterparty Risk The use of certain derivatives could result in the fund having a greater or more volatile exposure to the underlying assets and an increased exposure to counterparty risk. This may expose the fund to larger gains or losses associated with market movements or in relation to a trade counterparty being unable to meet its obligations. Emerging Markets Risk Emerging markets, and especially frontier markets, generally carry greater political, legal, counterparty and operational risk. Investments in these markets may expose the fund to larger gains or losses. Interest Rate Risk Changes in interest rates will usually result in the values of bond and other debt instruments moving in the opposite direction (e.g. a rise in interest rates likely leads to fall in bond prices). Liquidity Risk Difficult market conditions could result in certain securities becoming hard to sell at a desired time and price. Mortgage Related and Other Asset Backed Securities Risks Mortgage or asset backed securities are subject to similar risks as other fixed income securities, and may also be subject to prepayment risk and higher levels of credit and liquidity risk. BENCHMARK Unless referenced in the prospectus and relevant key investor information document, a benchmark or index in this material is not used in the active management of the Fund, in particular for performance comparison purposes. Where referenced in the prospectus and relevant key investor information document a benchmark may be used as part of the active management of the Fund including, but not limited to, for duration measurement, as a benchmark which the Fund seeks to outperform, performance comparison purposes and/or relative VaR measurement. Any reference to an index or benchmark in this material, and which is not referenced in the prospectus and relevant key investor information document, is purely for illustrative or informational purposes (such as to provide general financial information or market context) and is not for performance comparison purposes. Please contact your PIMCO representative for further details. AAA (highest) to B, C, or D (lowest) for S&P, Moody’s, and Fitch respectively. CORRELATION As outlined under “Benchmark”, where [disclosed herein] and referenced in the prospectus and relevant key investor information document, a benchmark may be used as part of the active management of the Fund. In such instances, certain of the Fund’s securities may be components of and may have similar weightings to the benchmark and the Fund may from time to time show a high degree of correlation with the performance of any such benchmark. However the benchmark is not used to define the portfolio composition of the Fund and the Fund may be wholly invested in securities which are not constituents of the benchmark. Investors should note that a Fund may from time to time show a high degree of correlation with the performance of one or more financial indices not referenced in the prospectus and relevant key investor information document. Such correlation may be coincidental or may arise because any such financial index may be representative of the asset class, market sector or geographic location in which the Fund is invested or uses a similar investment methodology to that used in managing the Fund

his year’s bank crises were certainly dramatic. But looking forward, PIMCO is confident that we are through the worst. A major

reason for this is that higher interest rates should be supportive for the banks’ profitability. “Even though interest rates have been increased dramatically, many banks are not passing them along to depositors,” says Alfred Murata.

As of 31 August 2023. Source: Bloomberg, PIMCO The views and expectations expressed are those of PIMCO. There can be no guarantee that the trends mentioned above will continue. Statements concerning financial market trends are based on current market conditions, which will fluctuate.

This is a marketing communication. This is not a contractually binding document and its issuance is not mandated under any law or regulation of the European Union or the United Kingdom. This marketing communication does not include sufficient detail to enable the recipient to make an informed investment decision. Please refer to the Prospectus of the UCITS and to the KIID before making any final investment decisions. The services & products described in this communication are only available to professional clients as defined in the FCA's Handbook. PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. ESG Category Article 6 Article 6 funds do not have sustainable investment as its objective, nor do they promote environmental and/or social characteristics. While such funds integrate sustainability risks into its investment policy (as further outlined in the Prospectus) and this integration process forms part of the investment level due diligence of the fund, ESG information is not the sole or primary consideration for any investment decision with respect to the fund. The climate statistics provided on the next slide are for informational purposes only. As the Fund is actively managed and does not promote environmental or social characteristics, the climate related holdings are not static and may vary considerably overtime. A Prospectus is available for PIMCO Funds and Key Investor Information Documents (KIIDs) are available for each share class of each the sub-funds of the Company. The Company’s Prospectus can be obtained from www.fundinfo.com and is available in English, French, German, Italian, Portuguese and Spanish.The KIIDs can be obtained from www.fundinfo.com and are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). In addition, a summary of investor rights is available from www.pimco.com .The summary is available in English. The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. PIMCO Global Advisors (Ireland) Limited can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive. Past performance is not a guarantee or a reliable indicator of future results. The “gross of fees” performance figures are presented before management fees and custodial fees, but do reflect commissions, other expenses and reinvestment of earnings. The “net of fees" performance figures reflect the deduction of ongoing charges. All periods longer than one year are annualized. Investments made by a Fund and the results achieved by a Fund are not expected to be the same as those made by any other PIMCO-advised Fund, including those with a similar name, investment objective or policies. A Fund may be forced to sell a comparatively large portion of its portfolio to meet significant shareholder redemptions for cash, or hold a comparatively large portion of its portfolio in cash due to significant share purchases for cash, in each case when the Fund otherwise would not seek to do so, which may adversely affect performance.

PIMCO GIS INCOME FUND

Portfolio management team

Seek consistent income distribution as a driver of total returns over time

Benchmark-agnostic* allowing for a flexible, actively managed approach to invest across the $136 trillion bond market

Led by Group CIO Dan Ivascyn and Portfolio Managers Alfred Murata and Josh Anderson

FOUR DRIVERS OF ENGAGEMENT

>

<

Steer positive impactby improving the ESG performance of the company

As of 31 August 2023. Source: PIMCO. *The fund measures its performance against the Bloomberg US Aggregate Index (the “Index”). However, the fund does not track nor seeks to outperform the Index (or any other index). As a benchmark agnostic strategy, it instead focuses on generating high current income, irrespective of the performance or composition of the Index.

Balanced Approach

Flexibility

Award-winning PM Team

Investment process – Balance yield and capital preservation objectives

Manage portfolio risk and ensure it is truly diversified

Capital preservation

Yield

PIMCO’s macroeconomic views

Seek consistent income

Seek opportunities across entire global bond market and have broad flexibility to express secular thinking and core investment themes

Be global and flexible

PIMCO GIS INCOME FUND philosophy

We have extensive experience in managing income strategies and a successful track record of delivering consistent income and capital appreciation.

Expertise

Our multi-sector income strategy is actively managed in line with our macroeconomic views. The flexibility of our mandates helps us to navigate volatility.

Differentiated approach

The insights of our secular and cyclical investment forum process is informed by deep credit research

Rigorous investment process

Our global investment and risk management teams reach across multiple sectors and geographies. We have more than 200 portfolio managers around the world, all coming up with ideas to include in our portfolios. And our Global Advisory Board includes experts such as Mark Carney and Ben Bernanke.

Extensive resources

Source: PIMCO

Leverages PIMCO’s robust "top down" and "bottom up" analytics across sectors along with our scale and relationships across global fixed income markets

PIMCO’s Fixed Income Expertise

Source: PIMCO For illustrative purposes only.

Allocate to high quality securities that should perform well during an economic slowdown and higher yielding securities that should remain resilient even in negative economic scenarios.

Seek to hedge against heightened volatility

Seek high and consistent level of distribution

income-oriented strategies from PIMCO

GIS Income Fund

Strategy since March 2007 UCITS fund since Nov 2012

SOURCE: PIMCO. * It refers to the Institutional EUR Hedged share class.

February 2011

UK Income Bond

Benefits from the full global opportunity set

Core allocation to Sterling securities with up to one-third globally sourced income

Seek consistent income & potential capital appreciation over time

Share value can go up as well as down and any capital invested in the Fund may be at risk. The Fund may use derivatives for hedging or as part of its investment strategy which may involve certain costs and risks. For more details on the fund’s potential risks, please read the Key Investor Information Document

Reflect PIMCO’s top-down views & include best income generating ideas

Mitigate downside risk by including high quality assets alongside higher income assets

Inception

Regional focus

Key features

Risk

TWO income-oriented strategies

Access multiple sources of return

Click on a fund name to view that fund and hover over boxes for details

As of 31 August 2023. Source: PIMCO Past performance is not a guarantee or a reliable indicator of future results and no guarantee is being made that similar returns will be achieved in the future. Dividend is not guaranteed.

Focus on income as a driver of total return

Seek to reduce downside risk versus other credit-oriented strategies

Strong consistent return since inception

Diversifying allocation within investor portfolios

Risk management

Duration: 0 to + 8 years Corporate high yield: Max 50% Emerging markets: Max 20% Currency: Max 30% gross exposure

Seeks a consistent income distribution + capital appreciation with volatility slightly higher than core bonds A consistent income distribution helps portfolio build up returns over time

Successful track record navigating rising interest rate environments Delivered attractive risk-adjusted returns of 5.4% (after fees) since inception Dan Ivascyn and Alfred Murata were named Morningstar Fixed Income Managers of the Year for 2013

Fixed Income continues to be a source of liquidity, carry and diversification Current macro backdrop and our secular thesis suggest the flexibility of the Income approach may be especially valuable in the environment ahead

Utilise a “bend but don’t break” philosophy where we expect price volatility, but we attempt to avoid permanent losses This has resulted in less volatility historically than other credit-oriented strategies

Income and capital objectives

Strategy: the best ideas and dynamic sector weightings

Key guidelines: duration and credit

Risk management: staying aware of the potential risks

This fund seeks to provide a high and consistent level of current income with a secondary objective of achieving long-term capital appreciation with a focus on UK opportunities

PIMCO's best ideas across multiple fixed income sectors Two-thirds of the portfolio invested in sterling denominated securities Sector weightings dynamically managed, in line with PIMCO’s broader investment outlook

Average duration range: 1-8 years Below investment grade: Max 50% Emerging market bond securities: Max 25%

Spotlight on: PIMCO’s approach to income investing

Hover over boxes for more details

PIMCO GIS Income Fund

Benchmark-agnostic strategy with flexibility to access global opportunity set

PIMCO Select UK Income Bond Fund

Our global investment and risk management teams reaches across multiple sectors and geographies. We have more than 200 portfolio managers around the world, all coming up with ideas to include in our portfolios. And our Global Advisory Board includes experts such as Mark Carney and Ben Bernanke.

Investment philosophy