IN PARTNERSHIP WITH

For more information visit: www.incisiveworks.com

This digital experience is an Incisive Works product © 2022 Incisive Business Media (IP) Limited

China: The new player in Biotech

xxxxxxx

xxxxxxxxxxx

The sky is the limit in emerging Biotech

Biotech – Invest in the science, not the macro-outlook

n recent years the biotech industry has grown significantly and despite the current challenges in the macroeconomic environment, the sector is well-positioned with new

technologies and performance that are less dependent on economic cycles.

I

“Net zero commitments are set to revolutionise the world of long-dated real assets”

scroll

BIOTECH INVESTING

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly. This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. Before making an investment, investors should read the relevant Prospectus and the Key Investor Information Document / scheme documents, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those documents or for professional external advice. The products or strategies discussed in this document may not be registered nor available in your jurisdiction. Please check the countries of registration with the asset manager, or on the web site https://www.axa-im.com/en/registration-map, where a fund registration map is available. In particular units of the funds may not be offered, sold or delivered to U.S. Persons within the meaning of Regulation S of the U.S. Securities Act of 1933. The tax treatment relating to the holding, acquisition or disposal of shares or units in the fund depends on each investor’s tax status or treatment and may be subject to change. Any potential investor is strongly encouraged to seek advice from its own tax advisors. For more information on sustainability-related aspects please visit https://www.axa-im.com/what-is-sfdr. AXA Framlington Biotech Fund is a part of AXA Framlington Range of Authorised Unit Trust Schemes and is managed by AXA Investment Managers UK Limited, part of the AXA IM Group. The capital of the Fund is not guaranteed. The Fund is invested in financial markets and uses techniques and instruments which may be subject to sudden and significant variation, which may result in substantial gains or losses. Single Sector Risk: as this Fund is invested in a single sector, the Fund's value will be more closely aligned with the performance of that sector and it may be subject to greater fluctuations in value than more diversified funds. Currency Risk: the Fund holds investments denominated in currencies other than the base currency of the Fund. As a result, exchange rate movements may cause the value of investments (and any income received from them) to fall or rise affecting the Fund's value. Further explanation of the risks associated with an investment in this Fund can be found in the prospectus. Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ.

In this Spotlight guide, we hear why the biotech sector presents investors with an opportunity not immediately influenced by the macroeconomic environment and why the best judge of performance is the quality of the science. We also explore the changing landscape as China becomes a new player in biotech.

The future looks bright

The outlook for the biotech industry looks positive as innovative technologies continue to drive performance

Additionally, we lift the curtain on exciting new opportunities in the sector that have the potential to reshape treatments across some of the most pressing healthcare challenges we face. We hear how AXA IM fund managers approach picking biotech disruptors while seeking to provide long term capital growth.

In depth Q&A: How AXA IM picks Biotech disrupters

BY THE NUMBERS: THE INVESTMENT CASE FOR BIOTECH

For Professional investor use only, not suitable for a retail audience.

Finally, we look deeper into the investment case for biotech, including the top-selling drugs, compelling names at the forefront of the sector, and where valuation stands.

SPOTLIGHT

MENU

HIDE X

Managers, argues that the outlook for the biotech sector remains positive and should be viewed separately from the macro environment; in biotech, the best judge of performance is the quality of the science.

he macroeconomic outlook for investing is going through a period of uncertainty. Share prices across many sectors have fallen amid rising inflation and interest rates. However, Peter Hughes, Fund Manager at AXA Investment

T

“These drugs tested in clinical trials, they don't care what the price of oil is, they don't care how much it costs to fill up at a gas station”

Biotech – invest in the science, not the macro-outlook

In a struggling macroeconomic environment the biotech sector presents investors with an opportunity to invest in businesses resilient to market forces

He says: “Over the last 5 years, we had more drugs approved than in any other 5-year period in the US. I think there's been an acceleration of innovation and drug approvals.”

He explains that from an investment perspective at AXA they don’t change their cost of capital assumptions through an economic cycle. They feel the same level of comfort with the stocks they bought a year ago as they do today.

Hughes says: “These drugs tested in clinical trials, they don't care what the price of oil is, they don't care how much it costs to fill up at a gas station. The trials will either work or they won’t, and they won't necessarily be influenced by the macro environment.”

Hughes also argues that the exciting outlook for the biotech industry is fuelled by hundreds of innovative projects that could see a strong performance. He explains that new technologies like mRNA that underpin the first Covid vaccines are ready to disrupt and accelerate product development in many other areas of biotech.

Beyond Covid

In recent years, the biotech industry has grown significantly in its profile. Before the Covid-19 pandemic, the average investor would likely be unable to name a biotech company. Today Moderna is a household name and organisations such as BioNTech have grown in public awareness. During the pandemic, this growth in familiarity contributed to spikes in performance for biotech indices.

Growing Awareness

Hughes says: “To save 20 million lives within a year is an unprecedented achievement. Covid highlighted the groundwork put in place over the last couple of decades within biotech to build an industry that can respond very quickly and with the right attitude.”

However, despite biotech's achievements during the pandemic, as society has reopened, investor interest has shifted to industries offering more immediate returns. Hughes sees this fall in interest as a significant long-term investment opportunity for a sector whose underlying performance is less dependent on the macroeconomic outlook.

Crucially, the most important variables to consider when investing in biotech companies include management quality and the science adopted. Hughes highlights that drug development spans several stages and years, requiring the company to transition into a commercial operation. Ensuring there is a strong management team in place to help make the appropriate decisions is more important to the success of a company than the macro-economic outlook.

“There's been an acceleration of innovation and drug approvals”

He also emphasises that when new technologies such as the enhanced use of antibodies in the brain, cell therapy and gene editing are approved, the number of profitable biotech companies will likely grow. In fact, with ageing populations and rising global obesity levels, the necessity for more sustainable healthcare spending will only drive further investment into the sector.

The emergence of China as the second largest market in the world for pharma and biotech also presents further room for growth in the sector. While geopolitics might present some hurdles to overcome, there is great potential for organisations to partner in delivering innovative products to Asian markets.

Despite the challenging macro-economic climate, the biotech sector is well-positioned with exciting new technologies and performance that is less dependent on economic cycles.

Hughes concludes: “We are buying what we think is the best science and the best management teams to drive that science forward. We think that is the best approach to investing”.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly. This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

The sky is the limit in emerging biotech

Emerging technologies and advancements in existing cancer and neurodegeneration treatments are bringing new opportunities to the biotech sector

Linden Thomson, Lead Fund Manager at AXA Investment Managers, explores several exciting emerging technologies that can reshape treatments across the healthcare sector.

“We have come a long way in cancer treatment and are still only halfway there”

Capital at risk. For professional investors only. Not suitable for retail audience.

barrier to investors understanding the opportunities in the sector.

nnovation is the lifeblood of the biotech sector. Without innovation, the sector cannot develop new treatments to address the long list of diseases impacting society. But with innovation comes complexity, and its lack of familiarity can act as a

One area that is unsurprisingly seeing a lot of research and development is cancer. Genome sequencing has historically been costly but is becoming cheaper and more accessible, opening the door to the development of treatment that focuses on the specific genetics of the cancer rather than relying on chemotherapy. With these advances, the next natural step for cancer treatment is to detect potential cancer in patients in remission and eventually detecting early stage cancer in otherwise healthy people through a simple blood test, vastly expanding the use of genomics in oncology.

Next step in cancer treatment

Thomson says: “We have come a long way in cancer treatment and are still only halfway there. It remains a hugely important part of biotherapeutics in terms of innovation that looks at immunotherapies, targeted therapies, and beyond.”

Another area of treatment primed for growth is neurodegeneration. Ageing populations will increase the number of expected neurological diseases – such as Alzheimer’s and other forms of dementia – over the next 50 years. Yet, while the need for treatment in these areas will increase, developments in neurodegeneration still lag considerably behind other diseases such as cancer, which puts it in a position ripe for investment.

When compared to oncology our understanding of the genetic basis or underlying biology for some of the most common neurological conditions is nascent which has hampered development of targeted therapy. Further, traditionally neurology clinical trials have been higher risk than for other therapeutic categories.

Neurodegeneration

Thomson explains that multiple US firms are due to report phase-three data for amyloid beta targeting agents used to combat Alzheimers disease, which could act as a catalyst for the sector. She emphasises how the perceived willingness of the regulator to approve drugs addressing neurodegeneration will encourage more firms to develop treatments.

From a neurology perspective, greater attention is also being paid to diseases such as schizophrenia, psychosis and epilepsy with drugs in development offering the potential for new ways to treat these conditions. Very recently we have seen some compelling late stage clinical data in schizophrenia and we’re expecting more clinical data over the next couple of years.

The other side of innovation in the biotech sector is in the technology underpinning drug development. The mRNA technology that was used to develop the Covid-19 vaccine in record time has scope to be used in the development of other vaccines as well as other areas. This includes potentially combatting the flu and even treating cancer.

Thomson highlights that cell and gene therapy is also becoming more prominent in treatment and enables the direct insertion of a healthy gene to replace a mutated gene causing a specific disease. She says: “Gene therapy so far has focused on rarer diseases, and I think the next step forward is probably in the larger diseases like haemophilia. That's where the next catalyst will come from.”

Emphasising the pace of the innovation, Thomson highlights how biotech industries operated at a speed during the pandemic, surpassing established pharmaceutical companies. This showed that biotech innovations aren’t decades into the future; they are very much a reality.

Future drug development

When asked about the potential of the sector, she says: “The sky is the limit.”

“Gene therapy so far has focused on rarer diseases, and the next step forward is probably in the larger diseases like haemophilia”

China: The new player in biotech

As global trends of ageing populations and lifestyle changes begin to become a reality, China has developed its biotech sector and become a new player in the world of innovative healthcare

4

From a private funding perspective, there has also been a significant increase in investment. The number of financing deals and total capital raised reached a record high in 2020.

In recent years the Chinese government have also implemented a series of reforms that have placed greater emphasis on biotech research and development capabilities, encouraging innovative therapy development and shortening the approval timelines for important treatments.

“It's still early days, but over the next 10 years, Chinese biotech is positioned for its next big step”

as the rest of the world. Cinney Zhang, Fund Manager at AXA Investment Managers, explores the emergence of China in the biotech industry and the opportunities and challenges facing the region.

he US has and continues to dominate the biotech sector, but the landscape is evolving. Ageing populations and health concerns related to lifestyle changes such as growing obesity prevalence are global issues, impacting Asia as much

China, as with the rest of the world, is experiencing significant demographic shifts. Its population of senior citizens is to nearly double over the next three decades to around 366 million in 2050. Zhang explains that healthcare expenditure will rise rapidly over that period, and the need for drugs for neurodegenerative disorders will be particularly high. Moreover, the increasing incidence of cancer in the region, the emergence of obesity, and the rising demand for fertility clinics and the treatment of genetic diseases has reinforced the need for innovation and increased options in the biotech sector.

Global Trends

Accordingly, there has been a huge rise in investment allocated to Chinese biotech funds. In 2018, the Hong Kong stock exchange implemented new listing rules that allowed pre-profit revenue companies to list, greatly expanding the sector in Asia.

Zhang says: “From then, more than four dozen biotech/medical device companies achieved initial public offerings on the Hong Kong stock exchange, raising billions of dollars to support the development of novel therapies.”

She says: “It's still early days, but over the next 10 years, Chinese biotech is positioned for its next big step and that presents exciting investment opportunities.”

Investment opportunities in the Chinese biotech sector are already becoming apparent. Zhang highlights several high-profile partnership deals where multi-national companies have licensed drugs from Chinese biotech firms – a reversal of trends where Chinese firms typically license drugs from western firms.

The next step

She says: “We have seen well-established multi-national companies signing deals and licensing drugs from Chinese biotech firms: I-Mab and AbbVie, Novartis and BeiGene, Lilly and Innovent, to name a few. Many of the drugs being developed by Chinese biotech companies are truly innovative which means they now stand as peers with the R&D pipelines of many of the Western biotechnology companies when large cap are considering deals.”

However, one factor that could impede growth opportunities will be the impact of US/China tensions. With the US requiring the auditing oversight of companies listed in the US, there is a risk that Chinese biotech companies could be delisted if they are found to have inappropriate levels of auditing transparency.

Zhang notes positive developments in this regard. She says:

“Recently, two countries have preliminarily reached an agreement, providing a framework to allow inspection of China-based accounting firms by the US regulator. This is a significant step forward to alleviate the delisting risk. As an investor, we monitor the progress on this front very closely.”

Challenges for Chinese biotech firms also exist from a research perspective. For treatments to be approved in the US, trials need to span multiple regions, focusing on various ethnicities, not just Chinese. Zhang emphasised that in the long-term this could help improve the strategy of Chinese firms, as global business opportunities require globalised research practices.

Domestically, the Chinese biotech sector also needs to develop a reimbursement model that can support new therapies. In China, public insurance programmes are still the main channel for patient access. If the country is to bridge the gap with the US biotech sector, it needs to develop its private insurance market to help accommodate the high cost of transformative therapies for patients.

Despite the challenges, the Chinese biotech industry has still progressed at an unprecedented speed. In the long-term, the region could pose healthy competition to the US market, with more opportunities and choices for patients and investors.

Zhang says: “Companies that adopt sustainable research and possess a responsible management team will prevail in financial markets. It doesn't matter in which region, whether it's in the US or China.”

“Companies that adopt sustainable research and possess a responsible management team will prevail in financial markets”

In depth Q&A: How AXA IM picks biotech disrupters

Linden Thomson and Peter Hughes explain their funds’ investment approach and how they gain exposure to innovative companies while seeking to provide an attractive level of long-term capital growth

From a fund perspective, ensuring that you've got a balanced portfolio across the large caps that are lower growth but defensive, cash flow generative and profitable companies, as well as having the mid and small caps is important.

Thomson: AXA Investment Managers has a long history of running sector funds and the healthcare franchise is one of those. We've successfully run both biotech and a healthcare franchise for over 20 years and we're one of the most established long-only investors in healthcare in Europe.

The Biotech Fund specifically invests in biotechnology companies, and we try and keep it pure to that investment thesis so that investors know what they're getting when they buy the fund. The fund invests in biotech companies ranging from small caps to large caps, but all the focus is on innovation in drugs and bringing new medicines to patients.

Hughes: The long-term thinking feeds into the focus on management quality. You want people who are going to be at these companies for a long time and they need to develop drugs through a number of different challenging stages and then transition the company into a commercial operation.

What differentiates the fund from other products in the marketplace?

Thomson: I think the key for investing in the sector is having a scientific background and rigour to hold companies to account on what they're doing. This includes how their drug works, how competitive it is versus others and how management are executing research and development, commercialisation and communicating to investors. Every company believes they have a solution to the next medical emergency or unmet medical need, yet statistics suggest that most drugs in development will fail. Understanding the science and likelihood of success is key to what we do.

I've been looking at biotech from both the buy and sell side since soon after the sector emerged. I've seen markets get too excited and equally, too pessimistic. Being a long-term investor in a market means you can take advantage of those highs and lows relative to what the fundamentals should be.

What is your process for evaluating biotech firms?

Hughes: Argenx is a premier example of a company that we've been invested in for a long time. Management have been very pragmatic and purposeful in the way they go about their development. They realised they had a great asset on their hands and really moved that forward at pace to develop it. They're reaping the rewards of that now.

Thomson: We first invested in the company when it was a European small cap with no approved drugs on the market. However, it had a good technology base, great management quality and an intriguing mechanism of action for the lead drug, which has the opportunity to treat numerous diseases. They then launched into the US market and they have not looked back.

Do you have an example?

Hughes: There are absolutely diversification benefits. If you look at the NASDAQ Biotech index and do a daily correlation over the last 3 years to MSCI World Health, it is more aligned than Pharma. The NASDAQ Biotech index does not move in parallel with pharma.

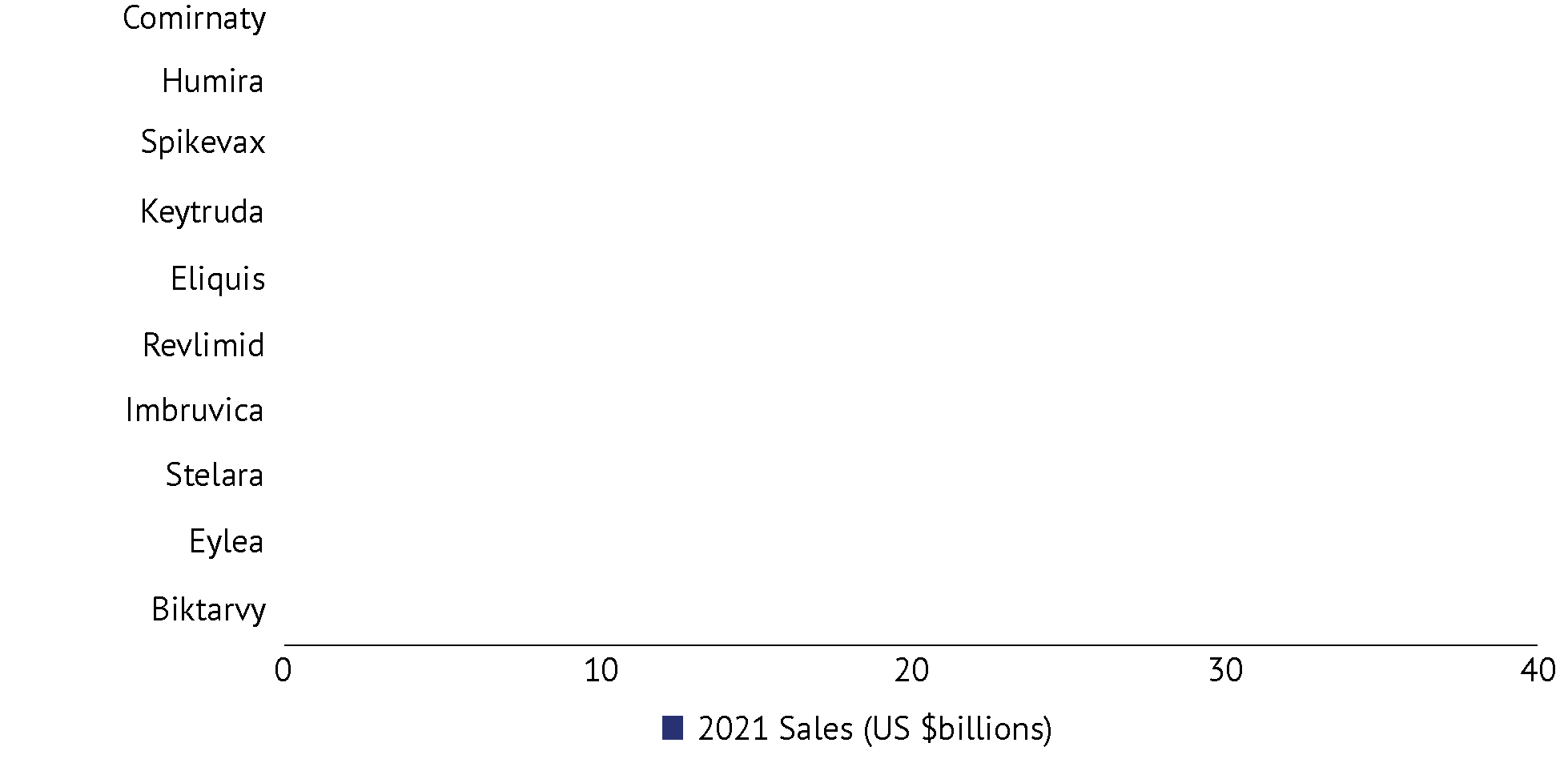

When you look at the top 10 best-selling drugs of 2021, they were all biotech drugs. if you're looking for innovation in drug development, why look at pharma when you can just skip straight ahead to biotech? I think it's fair to correlate high sales with best innovation and I think that's proof that the best innovation is coming out of biotech.

Are there diversification benefits to the fund?

Thomson: If you assume that passive performance is equivalent to an index, then you look at the performance of the fund versus the index to know why active is better. The fund has outperformed the index across all time periods through 10 years and that speaks for itself.

Hughes: A passive index is going to weigh you more towards the large caps, which have slower growth potential than the mid-caps. It's also a fallacy to believe that these passive indexes are built upon pure biotech exposure. Many of the companies are actually pharma companies or specialty pharma companies and don’t showcase the same innovation.

Hughes: It's for people who are looking for disrupters rather than to be disrupted. And you've got a situation where if you try and get exposure to biotech through a generalist fund, it's unlikely that they're going to be able to diversify the risks sufficiently. For our fund, we've got most of the risk coming from stock-specific risk, which is exactly where you want the risk to be.

Thomson: I also think biotech right now is interesting on a macro point. You've got 5%, 6% top-line growth; people's bullish view made them think they could find better returns elsewhere over the last two years. However, now people are looking at reliable 5% and 6% growth and saying “brilliant”.

Who is the fund for?

“The key for investing in the sector is having a scientific background and rigour to hold companies to account on what they're doing”

“The fund is for people who are looking for disrupters rather than to be disrupted”

What is the active management benefit?

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly. This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision. AXA Framlington Biotech Fund is a part of AXA Framlington Range of Authorised Unit Trust Schemes and is managed by AXA Investment Managers UK Limited, part of the AXA IM Group. The capital of the Fund is not guaranteed. The Fund is invested in financial markets and uses techniques and instruments which may be subject to sudden and significant variation, which may result in substantial gains or losses. Single Sector Risk: as this Fund is invested in a single sector, the Fund's value will be more closely aligned with the performance of that sector and it may be subject to greater fluctuations in value than more diversified funds. Currency Risk: the Fund holds investments denominated in currencies other than the base currency of the Fund. As a result, exchange rate movements may cause the value of investments (and any income received from them) to fall or rise affecting the Fund's value. Further explanation of the risks associated with an investment in this Fund can be found in the prospectus. Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.

Making the investment case for biotech with a look at top-selling drugs, companies at the forefront of innovation, and valuation

Innovation led - high growth, defensive business – supported by structural shifts in demographics and lifestyles

Top 10 selling drugs globally are all biotech derived

Fundamentals supported by structural shifts in demographics and lifestyles

Meaningful geographic expansion opportunities

Share prices correlate to sales growth long-term

High numbers of companies are trading under their cash balance

Valuation – sector the cheapest it has been in two decades

Number of companies trading below cash

Portfolio revenue growth CAGR forecast at 18%*

Biotechnology fund offers diversification and exposure to innovative, high growth sector

Nasdaq Biotech Index (NBI) Market Cap

Returns Correlations (36m)

Portfolio average market cap breakdown versus benchmark

Pioneering innovations

Next wave commercial

Mature large caps

AXA Framlington Biotech

Nasdaq Biotechnology Index

Source: AXA IM. Note: market cap – market capitalisation. (1) Update annually. Portfolio positioning is as at 31/05/2022. *probability adjusted.March 2022.

0.85

0.63

Source: FiercePharma.

Source: Cowen as at 25/02/2022.

Source: US population estimates, Catapult Health Oct 2019

Source: Jefferies.

Source: Jefferies as at 08/05/2022.

$80bn China Market 2030E, +10% CAGR

The investment case for biotechnology

BACK

1 / 4

NEXT

2 / 4

3 / 4

4 / 4

1 / 2

2 / 2

A deeper look at the numbers

Source: AXA IM, CRISPR, Intellia, Ultragenyx, Moderna, Sarepta Therapeutics, Denali, Biogen, Xenon, Karuna Therapeutics, iTeos Therapeutics, Ideaya Biosciences, Arcus Biosciences, Zentalis. Companies shown are for illustrative purposes only as of 31/03/2022 and may no longer be in the portfolio later. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. CR09911/07-19

Innovation in Research & Development pipelines looks good

Investment themes

More Oncology

Targeted Neuroscience

Gene Medicine & Gene Editing

Linden leads investment in the AXA IM Framlington Biotech Fund and co-manages the AXA IM Healthcare Fund. She has nearly two decades of buy-side and sell-side experience as one of the early specialists in the biotechnology sector. Her formative career was spent with Goldman Sachs in the Global Investment Research team covering healthcare/biotechnology. She has been at AXA IM since 2011. She holds a BSc in Biology (Medical Microbiology Hons) from the University of Edinburgh and is a CFA Charterholder.

CLOSE X

Linden Thomson

Cinney has over a decade of experience in the financial industry. Prior to joining AXA IM in 2021, she was an equity research analyst focusing on the biopharma sector. Cinney holds a MPhil in Statistics from University of Cambridge and is a CFA Charterholder. She also has a MBA degree from Cambridge, completing her thesis on “The Rise of China’s Biotech Sector: What the Future Holds”.

Cinney Zhang

Peter has been a Fund Manager at AXA IM Equities since 2015, specialising in healthcare. Head of AXA IM Equities healthcare impact research, Peter holds a PhD in Biochemistry from UCL and is a CFA Charterholder. He is also an Ambassador for the Royal Marsden Cancer Charity.

Peter Hughes

Meet the team

Select a for details

This marketing communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision. AXA Framlington Biotech Fund is a part of AXA Framlington Range of Authorised Unit Trust Schemes and is managed by AXA Investment Managers UK Limited, part of the AXA IM Group. The capital of the Fund is not guaranteed. The Fund is invested in financial markets and uses techniques and instruments which may be subject to sudden and significant variation, which may result in substantial gains or losses. Single Sector Risk: as this Fund is invested in a single sector, the Fund's value will be more closely aligned with the performance of that sector and it may be subject to greater fluctuations in value than more diversified funds. Currency Risk: the Fund holds investments denominated in currencies other than the base currency of the Fund. As a result, exchange rate movements may cause the value of investments (and any income received from them) to fall or rise affecting the Fund's value. Further explanation of the risks associated with an investment in this Fund can be found in the prospectus. Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an investment is not usually suitable as a short term holding.