Alternative sources of income

As prices continue to rise around the world, investors can create more resilient portfolios and manage inflation risks by investing in real assets.

Are real assets the answer to managing inflation?

Real assets

Alternative asset classes are increasingly in the spotlight as investors hunt for returns in a challenging and volatile environment.

10 considerations for building strategic allocations to alternative credit

Alternative credit

Latest articles

Scroll down for latest insights

Investing in sustainably managed timberland and farmland alongside the protection and restoration of natural capital has the potential to offer tremendous returns for society and investors.

A bedrock for the future

Natural Capital

Carbon credit markets allow investors in land-based assets to unlock the value in timberland and farmland to help achieve net zero commitments.

The road to net zero: Carbon markets and land-based investments

natural capital

$44 trn

The amount of global output that is dependent on natural capital

In partnership with

“Land-based assets have either kept pace or outpaced inflation”

Source: The World Economic Forum

Find out more from Nuveen

Nuveen has supported the financial futures of millions of investors for over 120 years. Under the leadership of TIAA and with $1.1 trillion assets under management*, we invest in the growth of businesses, real estate, infrastructure, farmland and forests while building long-term relationships with clients from all over the globe. With expertise across income and alternatives, and as one of the first in the industry to practise responsible investing, we continue to expand our capabilities while maintaining our legacy as a leading investment manager.

Investing to make an enduring impact on our world

About Nuveen

*As of 30 Jun 2022.

ESG’s impact on investor and management behaviour has changed the way we look at the world, but what does it mean for private credit?

What does ESG mean for private credit?

PRIVATE CAPITAL

Real estate themes for 2023 are predominantly driven by the continued fallout of surging inflation and interest rate hikes from central banks.

Real Estate Outlook: five themes for 2023

REAL ESTATE

“Contending with the continued impact of high inflation will be made more challenging by the widely accepted verdict that a recession is imminent”

As real assets become more accessible for investors, the time is ripe to look for yield outside of traditional investments, says Mike Sales, CEO of Nuveen Real Assets.

Generating income in a tough market

REAL ASSETS

Inflation looks set to ease in the coming months, but a looming threat of recession persists. Despite a rocky environment, various asset classes present opportunities.

2023 Outlook: Peaks and valleys

OUTLOOK

Source: The European Leveraged Finance Association

90%

of managers have passed on, reduced or sold out of a credit investment due to ESG reasons at least once

In today’s market, investors are looking for solid, stable and inflation-hedged income. Explore why alternatives are one of the first places investors should be looking at for compelling returns.

Mike Sales, CEO of Nuveen Real Assets

WATCH OUR VIDEO

Real estate plays an important role in portfolio diversification. The asset class has the potential to provide more than financial returns and can have a significant impact in helping the environmental aspect of portfolios.

Tackling environmental change through real estate

Private credit continues to mature and to increasingly find a permanent place in portfolios. Randy Schwimmer explores trends in the asset class.

How is private credit shaping up in a high-rate environment?

PRIVATE CREDIT

The potential of commercial real estate to offer attractive returns with low volatility, steady income flows, and fixed or floating rate structures makes real estate direct lending attractive to a wide range of investors.

Unlocking opportunities in real estate debt

Benefits beyond inflation

Hot inflation is stoking opportunities in real assets as historically, land-based assets have either kept pace, or outpaced inflation compared with traditional asset classes. Land-based assets like farmland and timberland produce goods such as food and housing, which are part of the consumer price index (CPI) basket. “As the prices of these goods rise, so does inflation, and cash yields from farmland and timberland assets rise with them as well,” says Gwen Busby, Head of Research and Strategy, Nuveen Natural Capital. “Eventually these higher prices are baked into valuations, helping to increase the capital appreciation component of return,” she says.

December 2022

As the prices of these goods rise, so does inflation, and cash yields from farmland and timberland assets rise with them as well.

Inflation will affect farmland and timberland differently and where the link between rising prices and the underlying investment is most direct, the inflation hedge is the strongest and felt most immediately. “In farmland, row cropland investments in grains and oil seeds tend to be most responsive to inflationary pressures, especially compared to permanent cropland like almond or citrus investments, for example” says Busby. Indeed, part of that responsiveness is due to the relationship with energy markets, especially for crops like sugar and oil seeds where the correlation with energy markets helps to support that positive feedback. “In timberland, wood supply agreements can have pricing linked to inflation,” Busby says. “In those cases, the positive relationship with performance is explicitly built-in to the investment.” Even so, when investing in real assets, investors face a wide set of risks that are unique compared to purely financial investments. There are risks related to growth in the yield of the crops or the commercial timber species, market risks, liquidity, operational and foreign exchange risks.

Learn about investing in real assets

Discover more

Click to view

There are a number of broader benefits of having real assets in a portfolio that reach beyond inflation and diversification tops the list. Firstly, land-based assets lack of correlation with capital market cycles and show a negative correlation between traditional equity and bond indices. The returns on land-based investments can also be advantageous. “Over time, we see a stable income return from real asset yields, and then a capital appreciation component of return that comes from asset sales,” says Busby. “In general, for farmland and timberland, we see higher returns compared to fixed income and lower volatility compared to public equities,” she says.

The environmental, social, and governance (ESG) benefits that stem from land-based assets include biodiversity, conservation, water quality and carbon sequestration and storage. The inclusion of land-based assets in a portfolio can help reduce the overall carbon intensity of a traditional portfolio, which can result in a hedge against more carbon intensive allocations and reduce potential volatility in the low-carbon transition. “Compared to traditional asset classes, both timberland and farmland have low-carbon intensity. They generate modest or low net negative CO2 emissions per USD invested,” says Busby.

In general, for farmland and timberland, we see higher returns compared to fixed income and lower volatility compared to public equities.

Investments in land-based real assets are long-term and focused on sustainable food, fiber, and timber production. “We view the transition to a low-carbon economy as an opportunity for investors to build climate resilient portfolios positioned to benefit from rising carbon prices,” says Busby. “For example, investing in land-based assets with strong carbon value drivers – achieved through enhancing yields, making operating practices more efficient, and sequestering and storing carbon in soil and trees – will be important for long-term performance and resiliency,” she says.

A focus on the long-term horizon

There are myriad factors that are driving investors to diversify their fixed income portfolios including high inflation, volatility, and low rates in traditional fixed income over the last decade, though rates are now rising. Against this backdrop, investors are increasingly looking across the credit spectrum to broaden their search for yield. According to Nuveen’s 2022 EQuilibrium survey, three-quarters of investors are planning to expand their reach for yield over the next two years and the vast majority are looking to alternative credit.

Alternative asset classes are increasingly in the spotlight as investors hunt for returns in a challenging and volatile environment. Within this broader shift, alternative credit is seeing continued strong interest.

Private credit has seen significant inflows for much of the past decade and the largest year-on-year increase among investor allocations to alternatives, according to the EQuilibrium survey. Recent events such as supply chain disruptions stemming from the COVID-19 pandemic and the war in Ukraine have led to surging inflation and pressured major central banks to raise rates. This has only added to the asset class’s attractiveness because the floating-rate nature of many private credit instruments makes this a key asset in a rising rate environment. Creating multi-asset portfolios that effectively blend private and public credit has become a top priority for investors seeking to enhance their returns. Below, we have identified 10 factors that are important for investors to consider when allocating to alternative credit:

Learn more about Nuveen’s approach to allocating alternative credit into portfolios

Investors reach for yield (%)

Alternative credit (private direct lending, real estate, debt, etc.)

Extend duration

Leverage

Low credit quality

Not planning to expand reach for yield

62

28

23

21

While some asset classes may exhibit similar yields, their underlying risk factors (equity, credit, rates and idiosyncratic risk) can be quite different. To truly diversify, the composition of that risk needs to drive diversified portfolio construction. So, rather than categorising assets as private vs. public or traditional vs. alternative, investors should view each portfolio component through a risk factor lens. This allows investors to avoid introducing unintended overlapping risk exposures.

Public markets can serve as liquid proxies while waiting to deploy

Unlike with publicly traded fixed income, it can sometimes take several quarters to deploy capital effectively in private credit, depending on the type of investment. But this does not mean that investors need to miss out on the desired exposures while they are waiting. Publicly traded assets, such as broadly syndicated loans, can generate directionally similar returns as middle market debt, for example.

New exposures need to be viewed through a risk factor lens

1

2

PREV

2 of 5

NEXT

The private credit market isn’t as crowded as you may think

3

4

As capital has flowed into private credit over the past decade, many investors have expressed concern about entering what some view as an overcrowded asset class. This overlooks the fact that demand for this type of lending is growing at a much faster rate than supply. Much of this demand is being driven by private equity firms seeking financing to support leveraged buyouts.

Selectivity and rigorous underwriting are paramount for middle market loans

Underwriting that minimises the risk of default is central to the success of a private credit strategy. This is especially true at a time when the credit cycle may be in its later stages and as rising interest rates loom as a potential recession trigger. Private credit investors need to be particularly mindful of the following underwriting considerations: sector exposure, exposure to rising interest rates, Covid-related impacts, and covenants.

Private equity sponsorship provides additional protection

5

6

Private equity sponsors provide an additional reservoir of capital that can be injected to help a business survive a downturn. They can also serve as an additional set of eyes and ears on the front lines to identify and address potential issues that could threaten a borrower’s solvency.

Managers have multiple levers for adding value

Private credit provides managers multiple ways to generate alpha for investors beyond simply credit analysis and underwriting skill. Originating a steady flow of deals from high-quality companies not only generates origination fees for the manager, it also empowers them to maintain selectivity and investor-friendly loan structures. Private credit fund management is a highly active, opportunistic approach that results in idiosyncratic risk being a large driver of the asset class’s return.

Risk factor premiums are not static

7

8

One of the primary reasons institutional investors use private credit is to harness the illiquidity premium, which compensates investors for locking up their capital for extended periods. It is important to realise that the premium that private credit offers can vary significantly over time.

Junior capital can be a valuable tool for boosting yield

Junior capital is overlooked by many investors, and this creates opportunities for incremental yield. It can take on multiple variations, such as subordinated notes and second-lien term loans. But, while it has attractive qualities, it also has higher risk than senior middle market direct lending and may be more vulnerable in a late-cycle environment where there can be uncertainty about the growth outlook.

Technique matters when modeling private credit

9

10

When it comes to modeling private credit into a portfolio alongside publicly traded fixed income, it is essential to desmooth the returns of private credit to create a workable like-for-like comparison. There are multiple valid techniques that investors can use to desmooth private credit returns, and it is important to realise that the choice of desmoothing technique can have a significant impact on the degree of the asset’s returns that are attributed to idiosyncratic risk.

Uncorrelated return opportunities with CLO equity

CLOs are securitised portfolios of floating-rate loans to well-established companies. Some key factors to know about them are that they are a long-term investment to help weather market cycles, they may offset other holdings that have more of a J-curve return profile and they can generate uncorrelated returns.

1 of 10

3 of 5

4 of 5

5 of 5

/

Source: Nuveen EQuilibrium Survey, 2023. Q: In the next two years, how does your organization plan to expand its reach for yield/how do you anticipate your clients will be expanding their reach for yield? Multiple answers allowed; includes all 800 respondents.

Nature-based climate solutions

To address the challenge of climate change and to achieve the Paris Climate Agreement’s goal of holding global warming to below 2°C, there is a broad understanding that concentrations of CO2 need to be reduced. Over one-third of the cost-effective, scalable climate mitigation opportunities come from forests, food and land, according to prominent climate scientists and major environmental organisations. Investing in land-based assets can help realise these opportunities and offer investors the potential to generate carbon credits from their investments. Carbon credits can be generated from timberland and farmland management that reduces greenhouse gas emissions (GHG) or sequesters CO2 from the atmosphere. In the short term, credits can be used to offset emissions that are currently difficult to abate. In the long-term and as production systems and supply chains decarbonise, they can be used to balance residual emissions to help achieve net zero targets by 2050.

Carbon credit markets are a way for investors in land-based assets to unlock the value in timberland and farmland to help achieve net zero commitments.

A carbon credit is a certificate representing one metric ton of carbon dioxide equivalent that is either prevented from being emitted into the atmosphere or removed from the atmosphere

Learn more about carbon markets for land-based investments

The dominance of forestry and land use credits in the voluntary markets is largely because these sources of emission reductions and removals are proven technologies and among the lowest cost available.

Demand for carbon credits is expanding rapidly as corporates, financial institutions, and governments commit to net zero climate targets. In 2021, voluntary carbon market purchases and retirements grew by 70% to 161 million tCO2e from 95 million tCO2e in 2020.

Management for carbon has a potentially beneficial diversification role in land-based portfolios

As climate action ramps up across the private and public sectors, we expect timberland and farmland’s capacity to generate carbon credits will be increasingly valued. Investments in timberland and farmland that reduce or remove GHG emissions and generate high-quality carbon credits have the potential to enhance investor returns and contribute to climate change mitigation.

What does this mean for investors?

Putting a price on carbon is one way to tackle climate change and advance the transition to a low-carbon economy. Pricing carbon creates incentives to reduce GHG emissions, increase GHG removal from the atmosphere, and encourage the growth of renewable energy sources. Different types of carbon credits and systems exist. Independent crediting systems form the largest market for carbon credits and have more than a decade of transaction history. Credits trade on a voluntary basis (and are known as “voluntary carbon credits”), and public or private parties can both generate and purchase credits. A “compliance carbon credit” is part of regulatory framework in which the buyer has legal obligations to reduce emissions and typically limited flexibility to purchase offsets as a way to help meet their obligation. The voluntary carbon credit market grew by 190% year-on-year in 2021 to about $1bn and is expected to continue growing, with credits from nature-based climate solutions in high demand as they are lower cost compared to technological interventions and capable of generating additional environmental and social benefits.

Understanding global carbon markets

Source: Nuveen Natural Capital

The process of carbon crediting and sales in the voluntary market

Timberland owners have, to date, been more active than farmland owners in carbon project development because of several factors specific to farmland – the high cost of soil carbon measurement, a larger minimum economic scale, and the prevalence of lease structures. However, as soil carbon metrics advance and the price for carbon credits increases, more agriculture (and forest carbon) projects are expected to come online. Across the major crediting mechanisms in markets, climate benefits carbon projects must be:

Real and measurable

Realised and quantified through a recognised methodology

Permanent

GHG emissions or removals must endure for at least as long as the emitted gas is contributing to climate change, with safeguards to reduce or reverse leaks

Additional

Emissions reductions must be “above business as usual” and would not have happened otherwise

Independently verified

Projects must be verified by an accredited, independent third party

Unique and traceable

Credits are tracked in a public registry to ensure that one carbon certificate is used to offset exactly 1 tCO2e

Returns from investment strategies that manage for carbon appear to be weakly correlated with returns from traditional timberland and farmland management. As a result, management for carbon has a potentially beneficial diversification role in land-based portfolios, which is in addition to the diversification benefits of adding natural capital to a portfolio of equities and bonds.

Natural capital sector

Project type

GHG benefit potential

Reduction

Removal

Forestry

Agriculture

Avoided deforestation (REDD+)

Forest restoration (Afforestation/Reforestation)

Improved forest management

Improved agriculture land management

Landowner provides land base for GHG reduction and/or removal project

Project development

Carbon project independently verified, then registry issues credit certificate and maintains certificate registry for tracking

Credits issued to project

Payment for credits received and certificate transferred to buyer

Credit sales

Credit buyer or polluter retires credit with registry

Credit retirement

Article author

Gwen Busby Ph.D

Head of Research and Strategy, Nuveen Natural Capital

Past economic development has degraded the earth’s air, land, and water, severely impacting nature’s capacity to support society and future prosperity. In just six decades, the global economy has grown from about $11 trillion in 1960 to $82 trillion in 2020, according to World Bank data. This seismic increase in activity has had an enormous impact on natural capital assets – the earth’s air, land, and water, and all their biodiversity – and the benefits, or ecosystem services, that flow from them. The flow of these benefits includes provisioning services, such as food, fiber, and timber, as well as a broad range of regulating, supporting, and cultural ecosystem services that drive the global economy and support livelihoods. The World Economic Forum estimates that $44tn trillion or over half of global output is dependent on natural capital. The global decline in nature puts this economic value and the wellbeing of people all over the world at risk.

Natural capital is the foundation for the livelihoods and wellbeing of people all over the world. Investing in sustainably managed timberland and farmland alongside the protection and restoration of natural capital have the potential to offer tremendous returns for society and investors.

As an asset class, natural capital investments, such as timberland and farmland, have the lowest average carbon intensity — or net CO2 emissions per dollar invested — among both alternative and traditional asset classes

Learn more about Nuveen’s approach to natural capital

Together, these supply constraints elevate the benefits of a globally diversified natural capital portfolio focused on productivity and positioned for climate resiliency. Timberland and farmland’s sustainable, low-carbon production systems and the capacity to generate verified carbon credits are increasingly valued as climate action ramps up. Allocations to timberland and farmland, with a net-negative carbon profile, can balance more emissions intensive sectors within an institutional portfolio, helping to achieve climate targets efficiently and without having to sacrifice returns unnecessarily.

Investing in sustainable farmland and timberland is a way to benefit from growing worldwide demand for resources and for supporting responsible food, fiber, and timber production systems. By 2050, farmland and timberland will have to support 9.7 billion people, according to the World Bank. Over this same period GDP per capita is expected to nearly double. In emerging market countries like India and China, where middle incomes are rising, resource demand is likely to increase significantly. In developed markets, such as the U.S. and E.U., demand for wood is expected to rise as it becomes increasingly recognised as a low-carbon input to building, packaging, and energy production. Just as global demand for food, fiber and timber is increasing, both timberland and farmland face supply constraints in some places. To combat deforestation and unsustainable management, forests and grasslands are increasingly protected for biodiversity conservation and climate mitigation. Meanwhile, farmlands are being lost to degradation, with soil erosion leading to significant losses in crop yields.

Natural capital assets and benefits

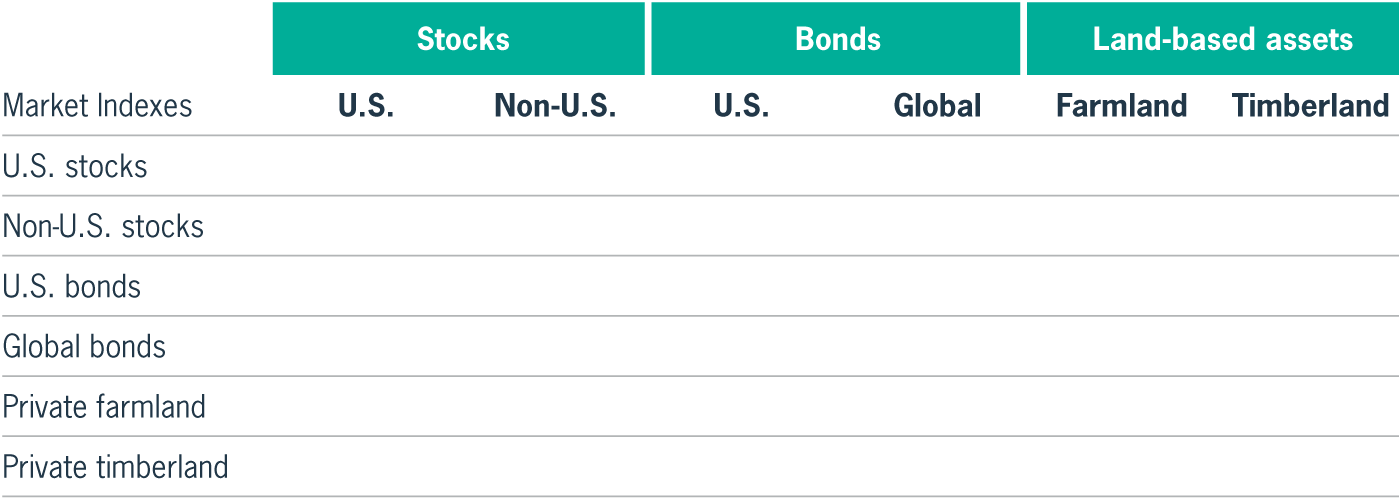

Data are based on total returns, calculated on a rolling four-quarter basis for the periods ended 31 Mar 1992 – 31 Dec 2021. Asset classes reflect the following indexes: U.S. stocks: Russell 3000 Index; U.S. bonds: Barclays U.S. Aggregate Bond Index; Non-U.S. stocks: MSCI ACWI ex-US Index; Global Bonds: Barclays Global Aggregate Bond Index; Farmland: NCREIF Farmland Index Timberland: NCREIF Timberland Index. Sources: NCREIF, FactSet.

The attractive risk-adjusted returns of timberland and farmland are in large part due to the lower volatility compared to U.S. and non-U.S. stocks. This low volatility is underpinned by stable cash yields as demand for timber and agricultural crops is relatively inelastic, remaining consistent through economic cycles. The fundamentals driving returns got natural capital are supported by long-term secular trends, such as population and economic growth.

Tailwinds support the long-term outlook

Investing in natural capital means incorporating nature into investment decisions in a way that achieves financial returns and considers natural capital stocks and ecosystem services. In practice, this means managing timberland and farmland for timber and agricultural crops alongside a broader set of ecosystem services. Like all alternative asset classes, timberland and farmland must earn their position in an institutional portfolio. The portfolio-level benefits include portfolio diversification, a hedge against inflation, and an attractive return profile coupled with a stable cash yield. Over the past several decades, U.S. timberland and farmland returns have exhibited low or negative correlations with traditional asset classes.

The case for investing in natural capital

They have provided a strong hedge against inflation as evidenced by long-term returns that have far outpaced the inflation rate. The positive correlation between inflation and performance is underpinned by the fact that many commodities, such as food and building materials, are components of inflation measures, such as the Consumer Price Index. Rising inflation reflects increasing prices for these goods and an ability to earn more from timber and crops. In the near term, higher prices improve performance by increasing cash yields. Over the long term, higher prices can also increase the capital appreciation component of return as they are incorporated into asset valuations.

Positive correlation with inflation

Correlation coefficient between U.S. inflation and traditional asset classes, timberland and farmland returns (1992 – 2021)

U.S. stocks U.S. bonds Non-U.S. stocks Global bonds U.S. farmland U.S. farmland: row crops U.S. timberland

-0.06

0.34

0.16

0.06

0.17

0.11

Correlation coefficents for U.S. CPI and total returns, calculated on an rolling four-quarter basis for the periods ended 31 Mar 1992 – 31 Dec 2021. Asset classes reflect the following indexes: U.S. stocks: Russell 3000 Index; U.S. bonds: Barclays U.S. Aggregate Bond Index; Non-U.S. stocks: MSCI ACWI ex-US Index; Global bonds: Barclays Global Aggregate Bond Index; Farmland: NCREIF Farmland Index; Timberland: NCREIF Timberland Index. Sources: NCREIF, FactSet.

Real assets are powerful diversifiers

Correlation of land-based assets (Annual Returns, 1992 – 2021)

Investors are still reeling from a difficult year but the contours of the investment landscape have evolved. One primary obstacle — stubbornly elevated inflation — looks a little less imposing, while another — a projected recession affecting countries around the globe — has been brought into sharper relief. In the U.S., we think inflation peaked in October, with both headline and core CPI readings showing significant year-over-year declines. This initial descent from the inflation summit is welcome, but it takes more than one data point to make a trend. And even a downhill climb can have its treacherous moments. Contending with the continued impact of high inflation will be made more challenging by the widely accepted verdict that a recession is imminent. The shift from inflation risk to recession risk reflects the impact of aggressive monetary tightening by the world’s central banks, which have fixated on inflation-fighting at the expense of economic growth. Even with inflation starting to moderate in the U.S., there is no guarantee that central bank policy rates will follow suit. In light on these challenges, we have emphasised these central themes for 2023:

January 2023

Inflation looks set to ease in the coming months, but a looming threat of recession persists. Despite a rocky environment, various asset classes present opportunities going into the new year

In the wake of declining inflation, we’ll find a global economy still nursing a hangover from the post-pandemic reopening binge, hampered further by higher borrowing costs and diminished savings

Signs of inflation easing should be cause to celebrate. But in the wake of declining inflation, we’ll find a global economy still nursing a hangover from the post-pandemic reopening binge, hampered further by higher borrowing costs and diminished savings. This may lead businesses to slow their pace of hiring — or reverse course to reduce headcounts — which will, in turn, weaken consumer spending even if income growth once again starts to outpace inflation. Countries like China and Japan remain sensitive to export demand but have also seen their domestic economies struggle. Meanwhile, Europe’s fate remains closely tied to global commodity prices, energy preparedness and, yes, the weather.

The economy and markets

Varied opportunities should present themselves across geographies: In the U.S., we’re focused on specialized medical offices that benefit from an increasing move toward outpatient procedures; we like European suburban housing (specifically rentals) in areas enjoying growing industrialization; and in Asia we prefer investments such as Tokyo senior living facilities and Australian student housing benefiting from demographic trends.

Real estate

Adopt a less cyclical stance Strengthen core bond holdings Carefully assess public vs. private allocations.

• • •

Perhaps the highest-conviction collective view from Nuveen’s Global Investment Committee is our preference for infrastructure investments, particularly public infrastructure. Regulated utility revenue tends to be relatively decoupled from the economy and can experience growth from rising capital costs and policies related to energy transition and the Inflation Reduction Act in the U.S. Private infrastructure may well benefit from these same trends. Farmland is another promising area within private real assets, as it can do well amid elevated levels of inflation and the geopolitical pressures that are creating supply issues. We expect row crops across geographies to have a better-than-average year, and believe farmland will remain a solid inflation hedge.

We think we are approaching the end of the current rate-hiking cycle in the U.S. and think a terminal rate might kick in sometime in the second quarter of 2023. Other central banks are likely to continue tightening as they are further behind the curve. As such, we’re growing more comfortable taking on some duration risk and think it makes sense to move closer to neutral. At the same time, we’re growing a bit more wary toward credit risk as recession indicators rise, which could cause some spread widening. We think corporate credit fundamentals remain solid and we’re not expecting a significant rise in defaults since most companies have been focusing on improving their balance sheets.

Fixed income

Regulated utility revenue tends to be relatively decoupled from the economy and can experience growth from rising capital costs and policies related to energy transition

We expect the all-too-familiar headwinds of 2022 - persistent inflation, rising yields, hawkish central banks and a rocky geopolitical landscape - to drive volatility and uncertainty through the start of next year. Geographically, we prefer U.S. stocks (especially large caps) relative to other markets, as they offer better opportunities for both defensive positioning and growth. However, healthcare, REITs and the materials sectors may be favourable globally, though we’re avoiding growth sectors such as technology, which could struggle in a longer-than-expected high interest environment.

Equities

Key takeaways

1. Inflation and pressure from interest rate hikes are likely to ease in 2023, but recession risks are growing. Our base case is for a mild recession in the U.S., but a worse environment in Europe. 2. We believe investors should focus on non-cyclical asset classes and investments that are less correlated with economic growth. 3. Additionally, we suggest modestly extending duration and carefully assessing the balance between public and private markets given the sharp public markets selloff.

For a more detailed outlook and the best ideas Nuveen has for each asset class, download our Outlook 2023

GAD-2625559PF-E0123W

As the ability to invest and scale in areas like infrastructure and real estate becomes more available, investors are increasingly adding alternatives to their portfolios. And while investors can be sure to find yield in a tough market, the caveat is what further rate rises have in store. “Investors must take a view on the macroeconomic outlook, especially what rates are likely to do,” says Mike Sales, Chief Executive Officer of Nuveen Real Assets. “After so much rate volatility in 2022, we’re beginning to see a leveling out which is good for the real assets market because you can’t have a 300-basis point rate rise and not see yields across all real assets rise.” “In terms of today’s yield environment, there is going to be sustainable income available from high quality real assets over the coming 12 to 18 months,” he says.

February 2023

As real assets become more accessible for investors, the time is ripe to look for yield outside of traditional investments

“We're seeing more resilience in the infrastructure space given the tailwinds behind the push to Net Zero Carbon” adds Sales.

Commercial real estate has seen headwinds, not just from Covid, and there is no doubt that the real estate valuations will be challenged in 2023. “We've already begun to see it across the globe in valuations coming through at the end of 2022. Real estate private markets tend to follow the public markets but there is always a lag,” says Sales. Rate rises must filter through because the cost of debt has a knock-on effect and takes time to come into the market. “There will be rental growth in those sectors with continued tailwinds and, whilst it may not be enough to compensate you for the outward yield shift that we're going to see, it will help mitigate that valuation impact,” he says. “The focus is really on those sectors that we expect to come through relatively unscathed whatever the market throws at us over the next two years and sectors we want to be in for the long term.” Mike believes that certain real estate sectors driven by long-term sustainable tailwinds, especially those supported by demographics such as the aging population and medical and life sciences facilities, will continue to see demand that will generate rental growth. For example, Nuveen’s Japan alternatives living strategy, seeks to address a structural under-provision of senior homes in Japan, with some estimated 400,000 seniors waiting for accommodation in public nursing homes alone. Japan provides an interesting opportunity as its population is aging faster than the global average. At 29% of the total, the population aged 65 and above increased to 36.2 million (as of 2020), growing by 2.3 million people compared to 2015 and the strategy operated by Nuveen will primarily focus on stabilised senior housing based on this data.

Real estate needs a long-term outlook

The subject of ESG (Environmental Social Governance) and the path to net zero has created challenges, but also huge opportunities across real assets and real estate. Significant amounts of investment capital are needed to reduce the carbon footprint of buildings and some infrastructure assets. An example is the firm's timberland strategy which sees a lot of interest because of its sequestration benefits and the fact that it can be used as a potential offset for some other elements of investor portfolios. Sales says regenerative agriculture, as it becomes more of a thematic investment, will present similar opportunities.

Real assets offer investors the potential for diversification and non-correlated returns compared with their holdings in their equity and, to a certain extent, their fixed income portfolios. They can also offer stable incomes and returns. The infrastructure market, along with renewables, the energy transition, and regulated utilities are seeing real resilience and continuing demand from investors. Sales expects demand to continue in the long term and particularly on the renewables side. He also points to continuing strong demand for timber and farmland because of their diversification and inflation hedge benefits.

Read more insights from Nuveen

GAD-2625520PF-E0223W

Mike Sales

Chief Executive Officer of Nuveen Real Assets

Real estate themes for 2023 are predominantly driven by the continued fallout of surging inflation and interest rate hikes from central banks. The general consensus is that interest rate rises will move at a slower pace in 2023, but the impact it will have on real estate is not yet reflected in the markets.

During October 2022, the euro traded at 20% below its long-run average for the first time since 1989. But deviations were even greater in Japan and the U.K. One-way bets are extremely rare in currency markets, but the scale of these movements makes it extremely likely that these currencies will appreciate against the dollar over the medium term. Europe, Japan and the U.K. could be fertile ground for U.S. dollar-based investors. Dollar returns are likely to be 20%–40% higher than local currency returns for a medium-term hold. An overshoot during the correction phase would take currencies above long-run average exchange rates against the dollar, meaning this sort of correction over a five-year hold could be as high as 4%–10%.

2: Is it a good time to invest in Asia-Pacific and Europe?

GAD-2625568PF-E0123W

Lending has become more focused on higher-quality assets. Lenders are more keen on loans backed by multifamily, industrial and alternative sector properties with strong cash flows, rather than spending more on financing business plans which require greater capital. With limited opportunities to finance light value-add business plans in the traditional multifamily and industrial sectors, financing aggregation strategies, particularly within alternative real estate sectors, may be an attractive opportunity for lenders. These financing arrangements can be particularly beneficial for lenders for several reasons:

3: A bigger role for alternative lenders

After an unprecedented period of ultra-loose monetary policy, higher interest rates are emerging as the key driver of a real estate market reset. More expensive financing could lead to upward pressure on cap rates across the globe, and the value correction in equity and most crucially bond markets may curtail the capital flow into real estate. European markets will likely face a significant property market correction resulting from the energy price shock, labour and supply shortages, interest rate hikes, currency weakness and a looming recession. Meanwhile, the U.S. economy is in the grips of demand-side inflation resulting from an overheated economy fuelled by government stimulus and energy independence. Economies in the Asia-Pacific region are in a better position than the U.S. and Europe, as milder inflation and more robust economic growth supports real estate markets. The cost of capital will be markedly higher in 2023 than the average of recent years for all regions. The extent of change is what will matter most for real estate markets. On that metric the U.K. looks most exposed, followed by the eurozone. The U.S. and Asia-Pacific markets are expected to see a somewhat gentler increase with hardly any change in Japan.

1: Same global problems, different market reactions

The cost of capital will be markedly higher in 2023 than the average of recent years for all regions. The extent of change is what will matter most for real estate markets

These arrangements provide scale, which is difficult to achieve in many alternative real estate sectors, as assets tend to be either small or sparsely traded. Many alternative sectors have secular tailwinds and non-cyclical drivers, which many lenders find attractive during a volatile market. Lenders can frequently get recourse to the sponsor’s platform or fund in case of default, given that there is more risk associated with financing smaller sponsors.

Climate risk is investment risk

Now that the costs of transforming buildings to be net zero carbon have started to be incorporated into underwriting, they cannot be ignored. There is also a greater body of data to show that greener buildings tend to outperform.

1 of 3

5: Sector winners, losers and surprises for 2023

As the market faces a protracted slowdown in 2023, a thoughtful selection of the most resilient sectors is critical. Structural tailwinds are important to picking the long-term winners and losers, but fundamentals are also key to deriving strong risk-adjusted outcomes.

4: ESG is here to stay

There are good reasons why environmental, social and governance (ESG) factors are likely to remain a priority – particularly for real estate investors.

Assets which fall short of ESG standards are likely to be repriced given the level of investment for adequate refurbishment needs. There is likely to be noticeable divergence between sustainable buildings, which will likely hold their value, and buildings which ignore ESG goals.

2 of 3

Repricing is an opportunity to accelerate net zero carbon

A wave of recent and forthcoming regulation makes it difficult for a company to abandon ESG agendas. Europe, the U.S. and Singapore have introduced regulations based on environmental disclosures, which, combined with U.K. regulations on transparency, demonstrate a concerted global effort to ramp up requirements.

3 of 3

Regulation will continue to drive ESG agenda

The industrial sector will face some challenges driven by macroeconomic headwinds and upcoming new supply. However, secular tailwinds from elevated e-commerce penetration and supply chain diversification will sustain demand and provide resilience for the sector. Alternative workspaces look set to offer greater potential as traditional office spaces have been hit from the normalisation of remote working, along with growing recession risks. However, opportunities for office spaces linked to specific industries will provide opportunities in 2023. Despite continued impact from e-commerce retail platforms, we believe there will be numerous surprises from physical retail properties in 2023.

For a more detailed outlook, read our full Real Estate Outlook 2023

Screening out companies for ESG reasons is a powerful tool for lenders. The European Leveraged Finance Association reported 90% of managers surveyed had “passed on, reduced or sold out of a credit investment entirely due to ESG reasons at least once.” It also signals to borrowers the need to up their ESG game to attract capital. As lender checklists become more sophisticated, demands on borrowers will grow. Larger companies, particularly broadly syndicated loan issuers, can be incentivized for meeting certain ESG targets. Spread discounts, for example, can be offered. But middle market businesses, often the most attractive area for private credit opportunities, do not always have the capability, for example, to track their carbon footprints or other ESG factors. Yet doing so will carry cost benefits the same way that better credit ratings do. Credit managers can use ESG criteria at the beginning of borrower due diligence. This is critical to establishing baselines to measure future performance against. These classifications generally fall into three categories: macro, micro and values-based. Direct lenders tend to focus on the latter two, with specific frameworks established to find red flags, and monitor them closely after the deal closes. Key to successful ESG integration in private debt is the close relationship lenders have with both the private equity owner and the borrower. The tighter the circle of credit providers, the more likely that key issues will be communicated.

Screening, due diligence and communication

GAD-2625573PF-E1222W

A consistent concern of private credit investors is the availability of ESG data. Over three quarters of participants in a recent ESG private debt survey, conducted by the European Leveraged Finance Association, cited a lack of ESG information would constitute a deal breaker and lead managers to turn down opportunities. To better bridge the ESG data gap between private equity and private credit firms and to standardize market information, the UN PRI has worked with managers including Churchill and other signatories to help develop the Private Credit-Private Equity ESG Factor Map. The tool’s goal is to promote collaboration between sponsors and lending partners, building off a standard set of ESG factors shared during the investment process. This tool aligns to industry reporting frameworks, including the Sustainability Accounting Standards Board framework, the Loan Syndications and Trading Association ESG questionnaire, Task Force on Climate-related Financial Disclosures and the Sustainable Finance Disclosure Regulation’s principal adverse impact indicators. The tool can also be adapted to an investor’s proprietary ESG framework. It increases in access to ESG data across stakeholders, reducing the many and varied data requests across private markets. As data availability becomes more prevalent, so too can the way ESG criteria is directly tied to lending practices and pricing schedules. These efforts, which will continue to evolve and improve over time, can reassure investors who seek to align their investment portfolios with their values and standards.

Overcoming ESG data challenges

Environmental, social and governance (ESG) assets will exceed $53 trillion globally by 2025, according to Bloomberg. At almost 40% of the projected $140.5 trillion global assets under management, investor demand for capital to be managed responsibly across all asset classes is evident. While private credit managers are not typically involved in the direct management of the companies they finance, they can integrate ESG practices into their investment portfolios.

Key to successful ESG integration in private debt is the close relationship lenders have with both the private equity owner and the borrower

Find out more about private credit and ESG practices

Building on TIAA’s history of five decades of responsible investing, Churchill began partnering with Nuveen, the investment manager of TIAA, in 2017 to integrate ESG factors into our investment process. As the focus on ESG integration in private markets has increased over the years, we have continued to expand our efforts and refine the methods we use to identify ESG risks and opportunities.

ESG evaluation for private credit

Identify if a company exhibits best practices, average practices or lack of management in ESG criteria.

Interpret ESG score

Companies are scored on E, S and G aspects of their business. Scores are weighted based on risks exposures identified in the underwriting and management assessment. Identify alignment with PRI and other global standards.

Calculate ESG score

Starts with underwriting team’s materiality assessment of the business, which helps define climate and headline risk screening, and the sector-specific management team’s assessment. Use proprietary ESG rating tool to understand the deal’s key ESG risks and opportunities.

Gather ESG data

Identifies investments in companies that work against our values (e.g. companies with a history of corruption, fraud, misconduct, etc) or sell core products or services that we do not want to be associated with (e.g. weapons, tobacco, coal, etc).

Broad negative screening against the firm’s exclusions

Co-Head of Senior Lending, Churchill Asset Management

Randy Schwimmer

Private credit continues to mature and to increasingly find a permanent place in portfolios. Randy Schwimmer, Co-Head of Senior Lending at Churchill Asset Management, an investment specialist of Nuveen, explores the trends in the asset class.

Until March of 2022, markets were operating in a zero-rate environment. After years in a zero-gravity world, you believe weightlessness is the natural state. You think ultra-high leverage for borrowers and no-covenant structures won’t hurt you. You don't care about interest coverage because for so long it was not an issue. But gravity has returned with U.S. Federal Reserve rate hikes. Interest coverage ratios now matter. Leverage has shrunk from six or seven times EBITDA to four or five. With the all-in cost of senior debt around 11% to 12% – twice what it was a year ago – borrowers’ capacity to service debt has greatly diminished. While private equity sponsors are forced to be more conservative about the amount of debt they're putting on their portfolio companies, private credit investors are benefiting from the diminished risk elements and greatly improved yields.

What do the twin threats of high inflation and recession pose for private credit?

GAD-2743457PF-Y0223W

Leverage is coming down because interest expense is going up. The all-in cost of capital for senior debt right now is in the double digits with the loan benchmark SOFR (Secured Overnight Financing Rate) up to almost 5%. We expect borrowing costs to remain at these levels through most of the year, and perhaps into 2024. This suggests market conditions will remain very favourable for private credit investors. Financial covenants in our deals have tightened thanks to the relative risk-off environment – also not expected to change any time soon. For example, the cushions between the leverage tests and borrower performance had widened to 40%, and is now back to around a 30% level. In contrast to the broadly syndicated loan market, direct lenders generally require quarterly maintenance financial tests. Before the Fed’s higher rate regime kicked in last year, some larger middle market borrowers could obtain incurrence-only tests, i.e. covenant-lite. Those are more scarce today.

What trends are you observing in private credit?

Defensive sectors such as healthcare, technology, software, logistics, and distribution have performed well and, in some cases, even better over the last three years than they did pre-Covid

Private credit as an asset class is about $1.3 trillion today, with estimates it will grow to about $3 trillion over the next five years. Compare that to the high yield bond and broadly syndicated loan markets which are each about $1.2 trillion. That growth is powered both by the amount of dry powder in the hands of private equity sponsors, and private credit fundraising. Direct lenders are leading new buyout financings by a ratio of eight-to-one over banks as of 4Q 2022. The asset class will continue to mature, and we think private credit lenders are going to be the dominant source of capital for private equity financings in the US.

Why do you think private credit market will continue to grow?

April 2023

Recession resistant companies have historically demonstrated resilient operating performances and steady enterprise values based on purchase price multiples. Our seventeen-year track record is composed largely from financing middle market companies that are more business-to-business and less consumer-facing. Industries we lean into include healthcare, technology, software, logistics, and distribution. These borrowers have done well through several business cycles and, in some cases, even better over the last three years than they did pre-Covid.

Financial covenants in our deals have tightened thanks to the relative risk-off environment and we don't expect that will change any time soon

One trend that has accelerated despite Covid and higher rates is the ability of private credit managers to build balance sheets to hold leveraged loans in ways that the banks never could. Discouraged for decades by the regulatory agencies from holding higher risk assets, banks mostly underwrote to distribute the loans to buyers such as retail and collateralised loan obligations (CLOs) funds. Post the global financial crisis, tighter regulation as well as increased bank consolidation put direct lenders in a position to increasingly disintermediate leveraged loans away from banks. Their ability to hold loans on balance sheet grew commensurate with the size of the firms. As an example, Churchill has a wide variety of funds under our control – separate managed accounts, CLOs, commingled funds, and BDCs – among which we can allocate commitments so that no one fund has any significant concentration.

How have private capital lenders stepped in to replace bank lending?

The practice of direct lenders using multiple pockets to hold loans – what I call “the cargo shorts strategy” – is a trend that will endure. If you have thirty different funds, you can commit to a $300 million loan and no one fund will hold more than $10 million of any one financing

Floating rate asset class

Fully secured by assets and cash flow

As private credit grows, we believe the potential benefits to investors will persist:

Hedge against recession and higher rates

Hedge against headline risk and volatility

2 of 2

Top managers with strong relationships supplying top tier quality asset

Protection in downturn with defensive industries

1 of 2

Those benefits have been available to sophisticated institutional investors, but increasingly also to high net worth individuals, family offices and retail investors. Interest in private credit is keen and growing given its proven track record of generating steady income at premium yields to public credit.

Over the next five years we expect to see more 'retailisation' of private credit, making it affordable and manageable for smaller investors. Public asset prices remain extremely volatile, so in our view, portfolios with private credit allocations may benefit from their valuations’ steadying effect.

What changes do you expect to see in the private credit market over the next five years?

Over the next five years we expect to see more 'retailisation' of private credit, making it more affordable and manageable for smaller investors

The need for less correlated assets in a very correlated world where other assets and prices tend to trade down in unison, is going to be essential going forward, especially as headline risk is not going away.

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR PUBLIC DISTRIBUTION AND NOT FOR USE BY RETAIL INVESTORS This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals. The views and opinions expressed are for informational and educational purposes only, as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; loss of principle is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Economic and market forecasts are subject to uncertainty and may change based on varying market conditions, political and economic developments. Risks and other important considerations Private equity and private debt investments, like alternative investments are not suitable for all investors given they are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, concentrated investments and may involve complex tax structures and investment strategies. Nuveen, LLC provides investment advisory services through its investment specialists. This information does not constitute investment research, as defined under MiFID.

Learn more about us

Source: Nuveen as of 16 Feb 2023.

Real estate has historically played an important role in portfolio diversification, offering investors alternative income streams. The asset class has the potential to provide more than financial returns, and can have a significant impact in helping the environmental aspect of portfolios.

Considering how the asset class can help portfolios, the benefits regarding returns fall into two main categories: Steady income Due to the essential nature of real estate, it has generally benefitted from inelastic demand regardless of where we are in the economic cycle. As a result, real estate assets have historically been linked to steady income cashflow. This characteristic means that the asset class can offer investors a low volatility alternative to traditional asset classes. Portfolio diversification The risk/return profile of real estate has shown that the asset class has the potential to produce a low and even negative correlation to equities and bonds. This low correlation can provide valuable diversification to balanced portfolios, possibly being able to offer a softer landing when traditional assets suffer amid market volatility or other macroeconomic factors.

What can real estate offer?

GAD-2788361CF-E0323W

Following a difficult year for public equities and bonds, the role that alternative assets such as real estate can play in portfolios is becoming increasingly valuable to understand. Alongside the need for asset diversification in portfolios, increasing attention is being placed on environmental change via investments. Real estate investors are increasingly aligned with the view that sound environmental credentials could have a positive influence on investment performance

As lawmakers seek to address climate change and regulators increase scrutiny on related activities, real estate is an asset class which could be a focal point for change

Environmental challenges do not mean sacrificing returns

Previously addressing environmental challenges through investments was perceived to be an exercise which comes at the cost of financial returns. However, the rise of impact investing into the mainstream investment world means there are far more options to tackle environmental challenges alongside financial returns. Impact strategies can vary greatly across asset classes, including real estate, and the goals they seek to reach. Nuveen Real Estate offers a variety of impact strategies, all of which are underpinned by a rigorous investment process, which aligns impact goals to specific Sustainable Development Goals alongside the financial potential of an investment. The need for positive environmental change is becoming increasingly clear for investors. Understanding how assets like real estate can help produce those positive changes alongside the wider investment benefits the asset class can offer demonstrates the need for well-diversified portfolio. Working alongside an experienced asset manager like Nuveen Real Estate offers investors the opportunity to benefit from a diverse global team with regional expertise across real estate markets. With more than 85 years of real estate experience, and a history of responsible and impact investing, we provide a platform with which to tackle environmental challenges, while seeking to capitalise on the growing trends that sustainability and climate change are starting to offer in real estate.

Regulation is inevitable

Regulators in Europe are pushing for a greater emphasis on reducing carbon emissions, with the need to be net zero by 2050. Implementing initiatives, like energy efficiency and sustainable materials, is a substantive start for reaching net zero. At Nuveen Real Estate, for example, we have brought our net-zero target forward to 2040, with these types of activities including water management, waste and recycling. Not only can these efforts have a positive impact on the environment through building efficiencies, they also have the potential to save costs further down the line. There are signs that environmentally friendly real estate could improve investment returns as well. Data from real estate analysts JLL and Knight Frank shows that greener buildings approved by the universally recognised Leadership in Energy and Environmental Design (LEED) certificate have seen outperformed returns over one, three, five and 10 years periods, while greener office buildings in London have demonstrated a rental premium of around 10% to 12%.

Read more real estate insights from Nuveen

While the wider benefits of real estate can provide attractive alternate income streams for portfolios, the asset also has the potential to deal with a growing need for investors – to account for environmental impact in portfolios. As lawmakers around the world seek to address climate change and regulators increase scrutiny on related activities, real estate is an asset class which could be a focal point for change, having accounted for 40% of CO2 emissions globally in 2021, according to the International Energy Agency. Understanding how investors can begin to overcome environmental challenges through real estate investments is of growing importance, and here is why.

Real estate’s environmental role

NCREIF office returns (%) by LEED certification

1.2%

2.2%

2.8%

1.7%

2.5%

2.3%

3.4%

5.2%

6.1%

5.9%

5.8%

7.3%

-0.6%

-0.1%

1 year

3 year

5 year

10 year

Certified

Silver

Gold

Platinum

Sources: NCREIF, Q3 2022, Knight Frank, 2022

Correaltions of real assets, commodities and REITs (1991-2021)

Real assets had low correlations to other asset classes - and to each other

Sources: NCREIF, FactSet, Nuveen, LLC.

Commercial real estate debt (CRE) continues to see strong interest from investors globally, especially in today’s rising interest rate environment. The potential to offer attractive returns with low volatility, steady income flows, and fixed or floating rate structures makes real estate direct lending attractive to a wide range of institutional and professional investors.

Rising interest rates and inflation in 2022 affected economic activity, leading to growing concerns of a recession or at least an economic slowdown in 2023. Historically, real estate debt often provided higher risk-adjusted returns than real estate equity across economic cycles, and better nominal returns at points such as this in the cycle. Declining equity and bond markets were an outcome of challenging economic environment, and resulted in many portfolios overallocated to real estate. In our opinion, these conditions in the current economic cycle could be an opportune time to invest in CRE debt. Given the abundance of lending opportunities offering strong relative value and attractive risk-adjusted returns, CRE debt has the potential to offer investors opportunity amid uncertain markets

Why now for CRE debt?

GAD-2799496PF-O1222W

Like many investment markets, real estate markets are currently experiencing heightened uncertainty due to inflation and political-related risks. Investors are now exploring alternative solutions to produce strong but predictable income returns. CRE debt investments are becoming increasingly sought after as they can provide relatively high and stable income streams, downside risk mitigation, diversification benefits, and competitive returns relative to other fixed income and direct real estate investments. These benefits are now open to lenders beyond the traditional banking sector as a result of the significant regulatory and market changes that have occurred since the global financial crisis.

Historically, real estate debt often provided higher risk-adjusted returns than real estate equity across economic cycles, and better nominal returns at points

Partnering with experience

Having invested in debt since 1934, and holding $45 billion in assets under management that are focused on debt globally as of December 2022, Nuveen Real Estate’s experience in CRE debt of identifying risk and navigating the intricacies of the market. Nuveen Real Estate’s CRE debt platform invests across the capital structure, seeking income-focused, stable and attractive, risk-adjusted as well as absolute total returns for investors through a diversified portfolio of investments. We have an extensive origination network, in-house debt structuring, syndication, risk, portfolio management and asset management capabilities that enable Nuveen to originate attractive credit investment opportunities on behalf of our clients. Nuveen finances core loans and transitional bridge loans, and can structure loans as senior notes, whole loans, and subordinate notes, with long and short durations across a wide array of risk/return.

CRE debt challenges: understanding risk and reward

Identifying how CRE debt differs geographically and identifying high-risk sectors and whether the rewards on offer are sufficient in current market conditions are just two of the challenges investors face when entering the debt market. Understanding how the CRE debt environment changes from one country to another is essential. Capital volatility differs between CRE sectors over the course of the real estate cycle and between countries, which creates differences in lending risk. Lenders need to identify where loans are at greater risk and ensure margins are high enough to compensate for that risk. Lenders should also manage risk through sponsor selection, asset analysis, loan structure and leverage, and they can target their desired risk by adjusting leverage and capital structure. Investors who intend to invest in CRE debt should partner with experienced and expert CRE lenders. These partners will have developed the sponsor relationships and have the expertise to structure transactions with features that can reduce risk.

The opportunities within CRE debt are not limited to the current market conditions. There are wider benefits that CRE debt can offer as part of a balanced portfolio.

What can CRE debt offer?

Capital protection Debt occupies a more secure part of the capital stack than equity, offering a measure of downside risk mitigation.

Capital volatility differs between CRE sectors over the course of the real estate cycle and between countries, which creates differences in lending risk

Diversification CRE debt can provide diversification benefits and a stabilising effect in a multi-asset portfolio.

Stable income Real estate debt has the potential to deliver stable, income-focused returns with low correlation to wider property and investment markets.

Relative value Attractive risk-adjusted returns relative to fixed income investments and direct real estate on a current income and total return basis.

Market opportunity Structural and regulatory changes in global CRE lending markets have created a long-term opportunity for alternative lenders.

Global CRE debt

CLICK ON SEGMENTS FOR DETAILS