OCTOBER 2025

The changing dynamics of MPS

In this Watchlist...

With assets under management rising and new models emerging, firms are reassessing how MPS fits within their propositions. This edition of the MPS Watchlist explores the innovations, challenges and strategies shaping the market today.

he MPS market is undergoing a period of strong growth and adjustment, driven by regulation, cost pressures and evolving client expectations. Innovation in portfolio design and delivery is moving quickly, while issues such as scale, sustainability and value remain central to the market’s direction.

T

This edition of the MPS Watchlist includes expert insights from L&G, Quilter, Rathbones, Schroders and Vanguard, covering some of the key topics in the MPS space, including:

• Active vs passive – is it as binary as the term suggests? • How to build successful partnerships • Assessing the role of fixed income in MPS • Considerations for the great wealth transfer

The state of the current MPS market and where to be cautious

Q&A WITH...

INSIGHT

Francis Chua, Fund Manager

The dollar dilemma: combatting hidden risks

Not all passives are created equal

Unlocking diversification in model portfolios: The Schroder Alternative Portfolio

The benefits of using liquid alternatives in portfolio construction

Managing Capital Gains Tax more effectively with Rathbones Model Portfolio Service

Invest well, live well: Insights on Rathbones’ investment philosophy

MPS WATCHLIST

Navigating the great wealth transfer

The value of personalised advice

The business of investment management is increasingly complicated because Consumer Duty means advisers who continue to manage client portfolios themselves face rules akin to asset managers. As a result, a growing number of advisors prefer to rely on MPS to manage assets and focus their efforts on financial planning and maintaining client relationships.

• Investors may not need to choose between active and passive strategies • Home bias should be a thing of the past • Advisers should be rethinking how to manage investments for clients • That there has never been a better time than now to be an adviser • Read the latest on issues in the sector

odel portfolio services are projected to grow to £154bn by 2028 and their increasing popularity reflects their importance for financial advisors and their practices.

< Return to homepage

Read our Q&A >

Key risk The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Past performance is not a guide to future performance. At times, especially over shorter timescales, lower risk-profiled model portfolios, and investments included in them, may fall in value by more than higher risk-profiled model portfolios, and investments included in them. Details of the specific and general risks associated with the model portfolios mentioned in this document are contained in the applicable fact sheet for each model portfolio. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. It should be noted that diversification is no guarantee against a loss in a declining market. Important information The information in this document is for professional investors and their advisers only. This document is for information purposes only and we are not soliciting any action based on it. The information in this document is not an offer or recommendation to buy or sell securities or pursue a particular investment strategy and it does not constitute investment, legal or tax advice. Any investment decisions taken by you should be based on your own analysis and judgment (and/or that of your professional advisers) and not in reliance on us or the Information. This document does not explain all of the risks involved in investing. No decision to invest should be made without first reviewing the Target Market Assessment, which can be obtained from the Client Relationship Manager. This document has been prepared by Legal & General Investment Management Limited and/or its affiliates ('L&G', ‘we’ or ‘us’). The information in this document is the property and/or confidential information of L&G and may not be reproduced in whole or in part or distributed or disclosed by you to any other person without the prior written consent of L&G. Not for distribution to any person resident in any jurisdiction where such distribution would be contrary to local law or regulation. No party shall have any right of action against L&G in relation to the accuracy or completeness of the information in this document. The information and views expressed in this document are believed to be accurate and complete as at the date of publication, but they should not be relied upon and may be subject to change without notice. We are under no obligation to update or amend the information in this document. Where this document contains third party data, we cannot guarantee the accuracy, completeness or reliability of such data and we accept no responsibility or liability whatsoever in respect of such data. This financial promotion is issued by Legal & General Investment Management Limited.© 2025 Legal & General Investment Management Limited, authorised and regulated by the Financial Conduct Authority, No. 119272. Registered in England and Wales No. 02091894 with registered office at One Coleman Street, London, EC2R 5AA.

Click here to find out more about L&G’s Model Portfolio Service (MPS).

Find out more

James Giblin, Fund Manager

“Consolidation can often lead to changes and updates in investment panels, sometimes creating uncertainty for end clients”

“Investment partners will face higher client expectations, which may drive innovation and transformation among MPS service providers”

he MPS market continues to evolve, with new participants entering each year, reflecting its ongoing growth and maturation. Segmentation has increased, both in terms of service offerings and the diversity of providers, including traditional wealth managers, ratings agencies, asset managers like ourselves, and, more recently, institutional investment consultants. This expansion raises important questions about how best to serve this market and what its stakeholders truly require.

Before addressing these supply considerations, it is important to recognise recent changes within the advisor market, which may influence demand for MPS-related solutions. A significant trend is consolidation, which is reshaping the industry and affecting all aspects of service delivery.

Consolidation can often lead to changes and updates in investment panels, sometimes creating uncertainty for end clients.

At L&G, we view these ongoing changes as analogous to managing multi-asset portfolios: by diversifying, we aim to build resilient and balanced portfolios capable of withstanding future challenges.

For advisors selecting an investment partner, this means prioritising those who demonstrate long-term reliability and consistent service quality, ensuring that their proposition remains relevant over the coming decades.

The important part here is that we’re continually developing these tools and services over time as client needs change. For example, we’re currently developing a tech solution for clients to sit alongside our existing microsites.

Finally, the growing variety of providers in the market offers advisors an expanded selection pool, in our view further enhancing their ability to help meet client needs effectively.

The initial step is to inquire about the adviser's expectations from a partnership. Typically, these discussions focus on four key areas:

What do firms ask for in a partnership and how are L&G set up to deliver this?

1. Ongoing resources and reporting

Trust – transparent and honest communication from an investment partner Strong performance track record The experience, size, and legacy of the investment team Business stability

• • • •

Co-branding various types of literature based on advisers’ identified needs, such as detailed articles or structured joint video content for client use. Self-service microsites developed for partner firms to act as a central hub for adviser requirements.

• •

2. Investment support

Weekly emails, monthly videos, and quarterly rebalancing documents to provide information about current market conditions and portfolio activities.

•

3. Enhancing governance and efficiency

Assistance with meeting regulatory reporting requirements and ensuring appropriate documentation is available.

What services can you provide?

With ongoing consolidation in the industry, it is anticipated that larger advisory firms and networks will continue to expand. This increased scale enables them to negotiate more favourable terms with suppliers, aiming to benefit end clients. Moreover, such growth offers the potential for enhanced personalisation, both in service delivery and investment portfolio management.

As a result, investment partners will face higher client expectations, which may drive innovation and transformation among MPS service providers. Those capable of adapting to these evolving needs are likely to thrive, increase their market share, and achieve further growth. In this environment, L&G is particularly well positioned. Having established our presence in the MPS market, we have leveraged the support of our wider organisation to continually strengthen our capabilities.

Our position as a large organisation allows us to provide comprehensive support at every stage of a client's journey. The ability to address client needs during periods of significant change cannot be overstated.

What does the future of the MPS market look like?

Consolidation is reshaping the MPS market, creating both uncertainty and opportunity for advisers. As client expectations rise and new entrants intensify competition, the focus shifts to resilience, innovation, and long-term partnership says L&G Fund Manager James Giblin.

he MPS market continues to evolve, with new participants entering each year, reflecting its ongoing growth and maturation. Segmentation has increased,

both in terms of service offerings and the diversity of providers, including traditional wealth managers, ratings agencies, asset managers like ourselves, and, more recently, institutional investment consultants. This expansion raises important questions about how best to serve this market and what its stakeholders truly require.

2

2. humancapital.aon.com.

Tap here to find out more about L&G’s Model Portfolio Service (MPS).

Read our Insight >

“A high-quality service is defined by its ability to address bottlenecks or challenges faced”

“To determine whether MPS functions more as a service or a product, it is useful to apply the consumer duty perspective”

The rise of MPS began with the RDR (Retail Distribution Review) back in 2012, which changed how advisers operate and led to a boom in outsourcing investment products through both multi-asset funds and models. Following last year’s introduction of Consumer Duty, advisers have faced greater scrutiny over their investment processes, prompting many to seek partnerships to improve their solutions and fulfil compliance obligations.

We believe the flexibility of MPS from an investment and service perspective is what advisers find so attractive, allowing firms to address operational challenges without sacrificing their unique investment philosophy. As adviser needs shift and consolidation increases, the MPS landscape will continue to evolve in the coming years in our view.

This topic has generated considerable discussion within our team, as the appropriate approach often depends on the specific requirements of each firm. We believe the flexibility of MPS is a significant factor in its growing popularity among advisers, offering potential opportunities for customisation and utilisation either as a collaborative partnership or in a transactional manner similar to a traditional fund.

To determine whether MPS functions more as a service or a product, it is useful to apply the consumer duty perspective. If the adviser is acting as a distributor, with no influence over the management or structure of the solution, then MPS is primarily treated as a product. Conversely, if the adviser is considered a co-manufacturer, the relationship becomes more consultative and closely resembles a service offering.

Ultimately, the nature of MPS varies depending on the preferred relationship model of the adviser. We believe that leveraging the resources and expertise of an established asset manager—while providing advisers access in a manner tailored to their business needs—can be an effective means to support clients. This approach can help alleviate regulatory and reporting burdens, helping improve marketing materials, and streamline access to technology within adviser firms, ultimately supporting clients to meet their goals.

Q

Why has MPS been such an incredibly popular choice for advisers over the last few years?

Is MPS a product? A service? Or somewhere in between?

These are generally the same questions we receive regarding our fund range, as well as those we direct towards the external fund managers with whom we collaborate. Typically, these questions can be classified into four categories:

A high-quality service is defined by its ability to address bottlenecks or challenges faced by a firm. Achieving this requires gaining in-depth understanding of the business and identifying specific areas requiring improvement. We believe that clear and honest communication is essential for effective collaboration and underpins all successful partnerships.

While each adviser firm we partner with has unique requirements and expectations, there are several recurring themes across our engagements. Enhancing governance and efficiency remains a primary benefit, most notably through the transition from advisory to discretionary rebalancing, which can alleviate significant cost and risk pressures. Additionally, advisers increasingly seek assistance with meeting regulatory reporting obligations and substantiating compliance where necessary.

Client engagement and reporting represent another area of continual development. We actively solicit client feedback to refine our approach, including the co-branding of a diverse range of literature informed by adviser needs. Ranging from basic investment queries to comprehensive thought leadership pieces or collaborative video content for clients. Moreover, we are leveraging technology to better support advisers, offering tools such as illustration software for client switches and self-service microsites tailored for our partner firms.

Ongoing investment support remains a critical component. Our objective is to guide advisers through market volatility by providing timely insights into portfolio management and market developments, ensuring they are equipped to communicate effectively with their clients. Proactive engagement during challenging periods is especially vital, as these moments underscore the value of strong relationships.

Our client base is diverse, encompassing those who seek close, ongoing partnership and others who prefer a more transactional relationship focused primarily on performance outcomes. The flexibility inherent in MPS enables us to accommodate the varied needs and preferences of our advisers to become a trusted long-term partner.

While these represent only the fundamental inquiries we encounter, in summary, most questions tend to fall within the areas of parent, people, philosophy, and product.

Parent: Does the business demonstrate stability and a track record of managing similar mandates? People: Is the investment team appropriately resourced in both size and experience to effectively manage the fund? This aspect is especially critical when overseeing broadly diversified or multi-asset portfolios, where the investment universe is extensive by nature. Philosophy: What is the overarching investment style of the fund, and does it align with our own philosophy and beliefs? Product: This serves as a comprehensive category. Is the investment process robust and thoughtfully designed? Are the risk management practices appropriate?

For those advisers who approach the relationship as more of a product, what are the types of questions they’re asking as part of the selection process?

What are advisers looking for in a partnership and what makes those types of relationships successful?

Why model portfolios keep winning advisers

L&G Fund Manager Francis Chua discusses the rise of model portfolio services, their dual identity as product and service, and what advisers are really looking for in long-term partnerships.

Q&A

with...

Francis Chua

If you would like to know more about our multi-asset passive solutions, click here.

Quilter is a trading name of Quilter Investment Platform Limited and Quilter Life & Pensions Limited, who provide the WealthSelect Managed Portfolio Service. Quilter Investment Platform Limited and Quilter Life & Pensions Limited are registered in England and Wales under numbers 1680071 and 4163431, respectively. Registered office at Senator House, 85 Queen Victoria Street, London, EC4V 4AB. Quilter Investment Platform Limited is authorised and regulated by the Financial Conduct Authority. Quilter Life & Pensions Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Quilter uses all reasonable skill and care in compiling the information in this communication and in ensuring its accuracy, but no assurances or warranties are given. Investors should not rely on the information in this communication when making investment decisions. Nothing in this communication constitutes advice or a personal recommendation. This communication is for information purposes only and is not an offer or solicitation to buy or sell any Quilter product. Data from third parties is included in this communication and those third parties do not accept any liability for errors and omissions. Investors should read the important information provided by the third parties, which can be found at quilter.com/third-party-data. Published: September 2025 QIP 23860/31/12777

Andrew Miller, Lead Investment Director

“Whilst the first tracker funds simply tracked US stock market performance, the market has evolved to offer multi-asset passive investments offering exposure to a wide variety of asset classes”

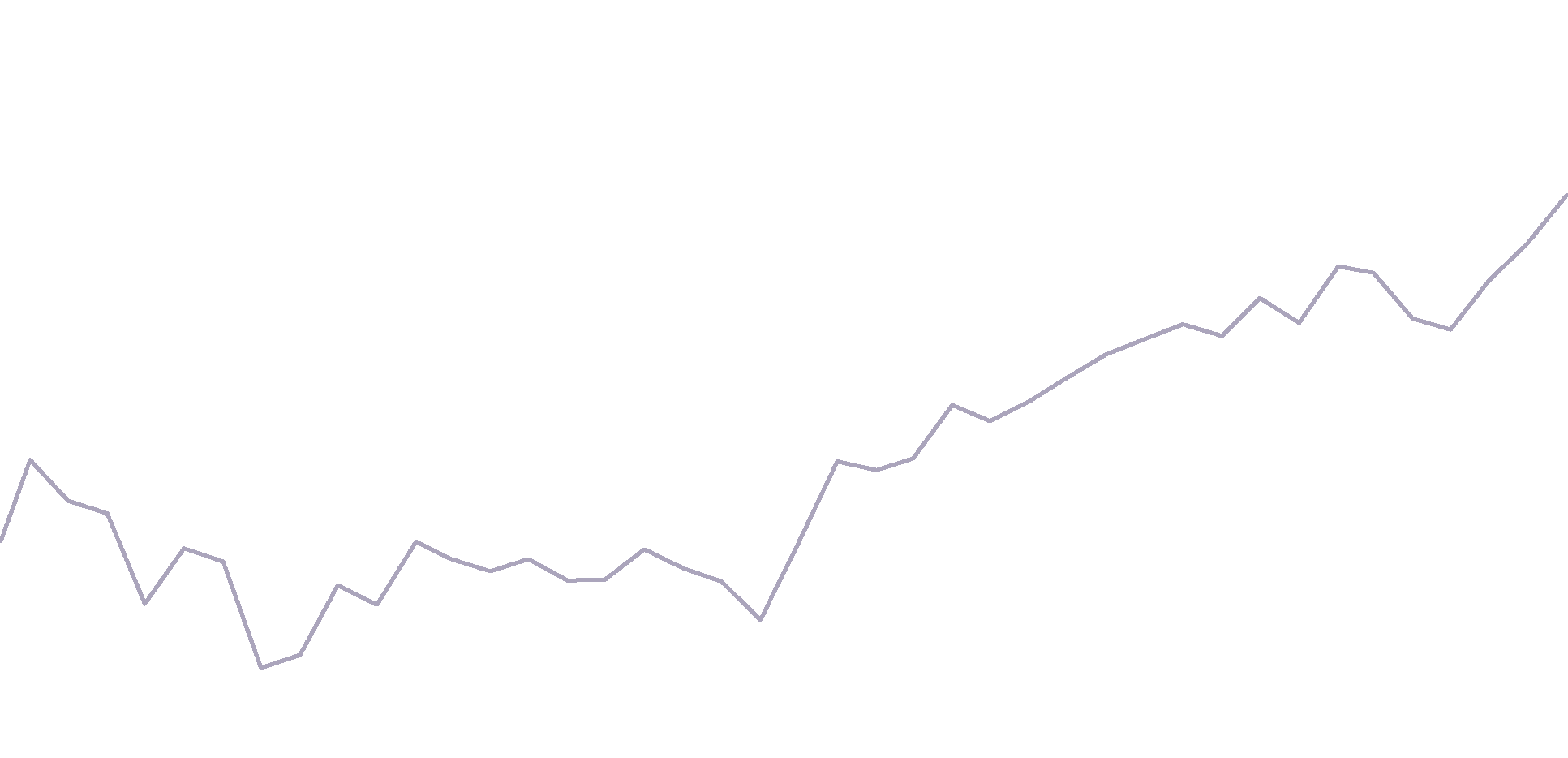

Return since launch of WealthSelect Managed Passive 5 vs peers

Past performance is not a guide to future performance and may not be repeated. Source: Quilter and Morningstar as at 31 August 2025. Total return, percentage growth over period 8 March 2022 to 31 August 2025. All performance figures are net of underlying fund charges, but gross of the Managed Portfolio Service charge. Deduction of this charge will impact on the performance shown. The WealthSelect Managed Passive 5 Portfolio launched on 8 March 2022.

Return (%)

“A multi-asset passive fund may passively follow a defined set of rules, but the decisions taken to create the rules are active”

e created a firm called Vanguard to build and market these tracker funds directly to the public. Dubbed ′The Vanguard Experiment′, the concept initially flopped. Promising only to match what the broader market index achieved was not thought to be very enticing and was denigrated by critics as ‘a sure path to mediocrity’ and, even, ‘un-American’.

Today, the story is somewhat different. In the US, assets in passive mutual funds and ETFs have surpassed those in active funds and Vanguard is the second largest asset manager in the world.

H

The first decision is what assets to include. Equities perform very differently in different regions – take developed and emerging markets as an example. And, unless an investor has a high-risk appetite, a pure equity approach is unlikely to be suitable. So, other areas are normally considered, such as fixed income. This can be government debt, corporate debt, or both, and can then be divided into different regions, maturities, credit ratings, etc. Another area to consider is alternatives like commodities or property. These can provide valuable diversification but can be hard to access via passive instruments.

The next decision is how to track the chosen assets. Passive investing is not as simple as it was in Jack’s day, as there are now over 100,000 funds to choose from. These include market-cap weighted, equally weighted, sector specific, and even so called ′smart beta′ investments. Each of these has their merits. For example, say you wish to invest in the US stock market, but you are concerned about the high exposure of the index to the AI-themed ′Magnificent Seven′. An equal-weighted tracker, where every stock has an exposure of 0.2%, could be an answer. The outcome of investing in this way will be vastly different – even though you are investing in the same underlying companies. So, the decision as to ‘how’ to track an asset class can be as important as ‘what’ to track.

While the first tracker funds simply tracked US stock market performance, the market has evolved to offer multi-asset passive investments offering exposure to a wide variety of asset classes. However, multi-asset passive investing is a lot more complex than tracking a single index.

The construction of a multi-asset passive investment involves a series of decisions, and because there are a variety of ways to approach each area, these are active decisions. As an asset manager, and as a financial adviser, it is important to understand what each of these are, and their potential implications.

Being actively passive

Once the ‘what’ and the ‘how’ are answered, the next question is how different asset classes are combined i.e. what is the asset allocation? Again, there are a variety of approaches. Some multi-asset passives follow a fixed allocation – for example 40% equity and 60% bond. This is simple and easy to explain. However, in years like 2022, holding a high proportion of fixed income was damaging to cautious investors, and this fixed approach slavishly follows its asset allocation regardless of whether it is appropriate or not. Other processes consider current market values and economic indicators and aim to create a forward-looking asset allocation. This is not without complexity, but it can manage the pitfalls of overpriced assets better than a fixed asset allocation.

The last area to consider is whether there should be a rebalancing process, and if so, how often. Answers to this vary from ‘never’ to ‘daily’. The more infrequently portfolios are rebalanced, the greater the chances of drift in terms of risk – which may be inappropriate for your advice process. Conversely, a higher frequency can lead to increased trading costs. However, even then, the word ‘rebalance’ can mean different things. In some cases, it will mean resetting back to the last rebalance. In others, it will mean considering new inputs from time to time and updating to follow these. Again, this discipline will have a significant effect on investment returns over time, so it is worth fully exploring.

The chart below shows three different investments. Fund A is a multi-asset passive fund that sits in the IA Mixed 20-60% Shares sector. It has a fixed asset allocation of 40% in equities and 60% in fixed income and rebalances to this every day. Portfolio B is a discretionary portfolio that adopts the same asset allocation. However, it only rebalances if the portfolio drifts beyond a specific tolerance. In reality, this timeline can be more than three years. Finally, the chart shows the WealthSelect Managed Passive 5 Portfolio, which uses a forward-looking asset allocation process that combines the potential returns of asset classes with their volatility and correlation to create an appropriate asset allocation. As you can see the outcomes of the different approaches can be quite different.

Understanding the differences

So, a multi-asset passive fund may passively follow a defined set of rules, but the decisions taken to create the rules are active – as is the decision of advisers as to which multi-asset passive investment to use. If you are considering using a multi-asset fund it is worth understanding exactly how it operates in each of these areas, as it will have a highly significant effect on the investment outcomes for your clients. Not all passives are created equal.

Making the right choice

Around 50 years ago, a man called John 'Jack' Bogle came up with a new investment concept. He introduced the idea of the tracker fund – a cheap investment fund that replicated a broad index of shares. His argument was that markets are efficient, and investment managers were trying to outperform a market over which they had no information advantage.

If you would like to know more about our multi-asset passive solutions, tap here.

e created a firm called Vanguard to build and market these tracker funds directly to the public. Dubbed ′The Vanguard Experiment′, the concept initially

flopped. Promising only to match what the broader market index achieved was not thought to be very enticing and was denigrated by critics as ‘a sure path to mediocrity’ and, even, ‘un-American’. Today, the story is somewhat different. In the US, assets in passive mutual funds and ETFs have surpassed those in active funds and Vanguard is the second largest asset manager in the world.

If you would like to find out more about Quilter WealthSelect, click here.

Source: Quilter and FactSet as at 31 August 2025. Top 10 stocks of the MSCI USA Index as at 31 August 2015, 31 August 2020, and 31 August 2025.

Top 10 stocks of the MSCI USA Index

Stock

Weight

3.56

1.84

1.71

1.57

1.41

1.35

1.29

1.10

1.07

2015

16.00%

7.73

5.23

4.70

2.27

1.61

1.30

1.18

1.17

2020

2025

27.86%

7.54

6.41

6.35

3.89

2.85

2.36

2.20

1.86

1.72

1.49

36.66%

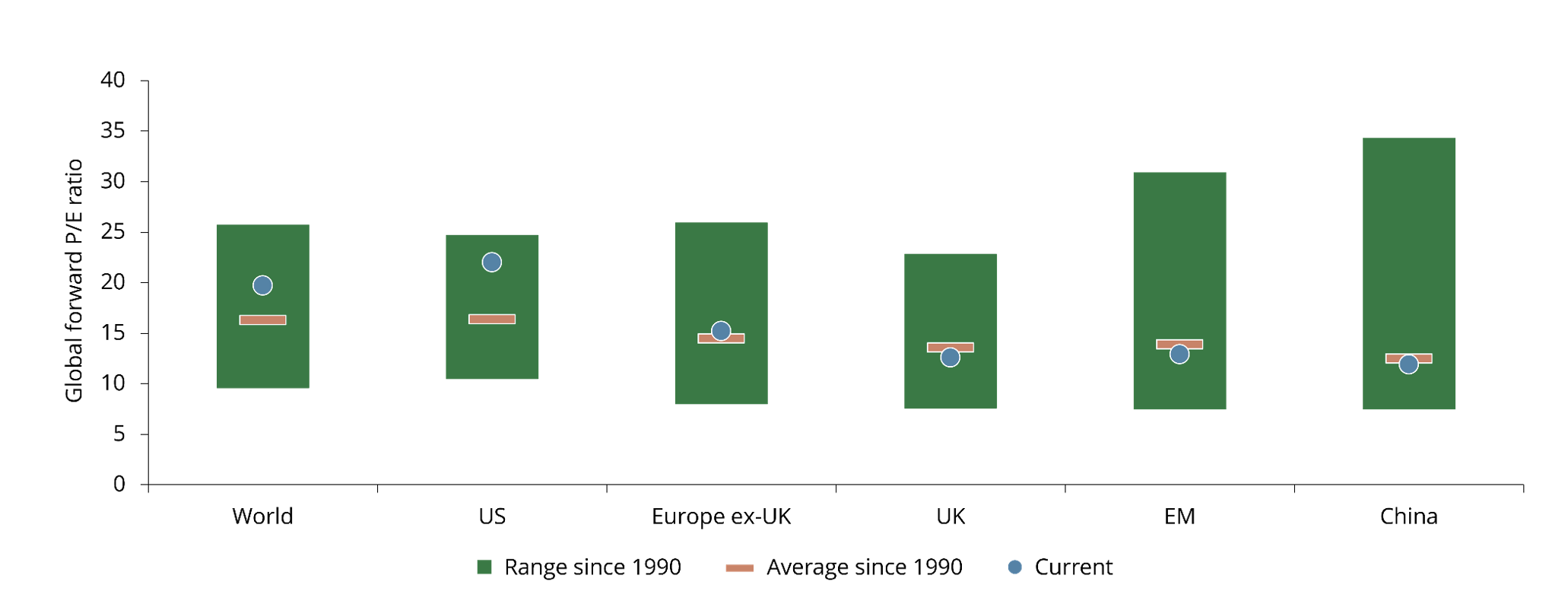

Global forward P/E ratio

Source: Guide to the Markets UK (Monthly), JPMorgan, 31 August 2025. Earnings data is based on 12-month forward estimates.

Regional equity valuations compared to long-term average

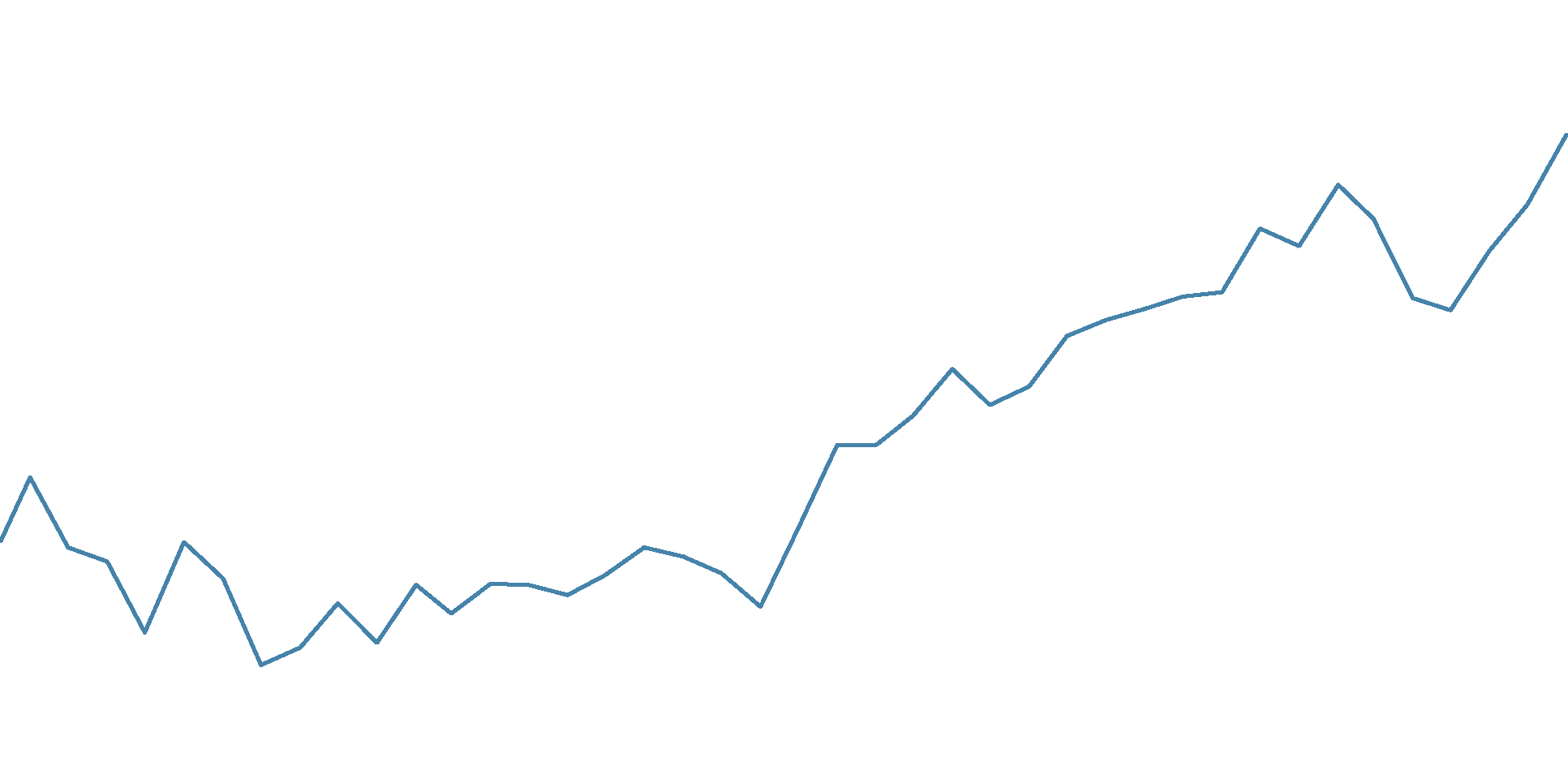

Source: Quilter as at 4 September 2025. Ten-year forward-looking volatility of the portfolio at time of each rebalance over period 24 February 2014 to 4 September 2025. The WealthSelect Managed Active 5 Portfolio launched on 24 February 2014.

Upper

Mid

Lower

Target volatility range

WealthSelect risk positioning

WealthSelect Managed Active 5

Quilter is a trading name of Quilter Investment Platform Limited and Quilter Life & Pensions Limited, who provide the WealthSelect Managed Portfolio Service. Quilter Investment Platform Limited and Quilter Life & Pensions Limited are registered in England and Wales under numbers 1680071 and 4163431, respectively. Registered office at Senator House, 85 Queen Victoria Street, London, EC4V 4AB. Quilter Investment Platform Limited is authorised and regulated by the Financial Conduct Authority. Quilter Life & Pensions Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Quilter uses all reasonable skill and care in compiling the information in this communication and in ensuring its accuracy, but no assurances or warranties are given. Investors should not rely on the information in this communication when making investment decisions. Nothing in this communication constitutes advice or a personal recommendation. This communication is for information purposes only and is not an offer or solicitation to buy or sell any Quilter product. Data from third parties is included in this communication and those third parties do not accept any liability for errors and omissions. Investors should read the important information provided by the third parties, which can be found at quilter.com/third-party-data. Published: September 2025 QIP 23859/31/12775

Ryan Medlock, Investment Director

“While elevated valuations among the ‘Magnificent Seven’ are well documented, the continued stream of strong returns has reinforced the belief that their growth story will simply run on and on”

“Investment decisions should be guided by a more forward-looking and rational assessment of future market dynamics”

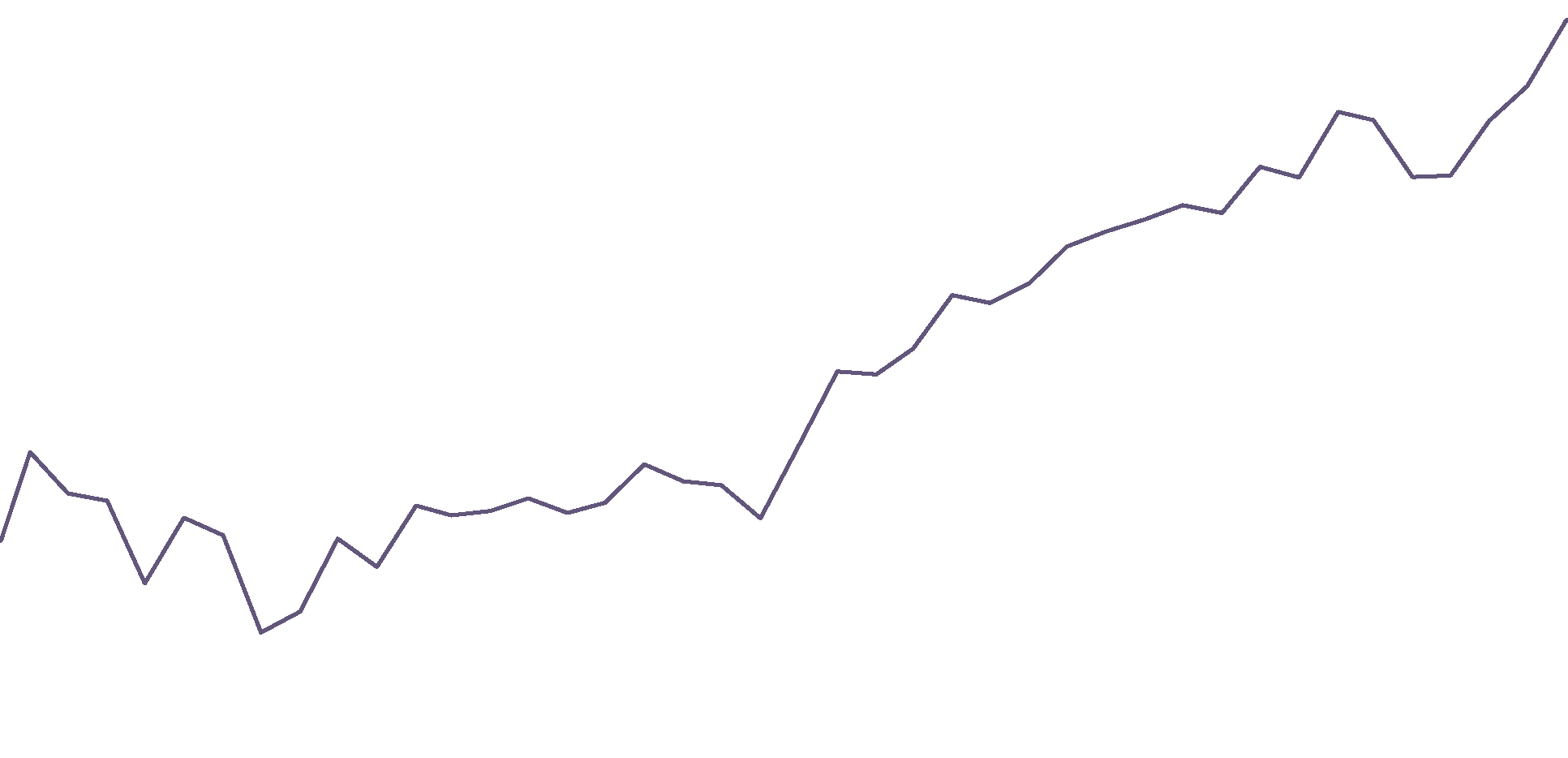

extraordinary growth. It is also interesting to observe that in 2015, the top ten holdings in the index were diversified across various sectors whereas it is now much more concentrated on tech stocks riding the artificial intelligence wave. This surge has been nothing short of remarkable, reshaping the global equity landscape and significantly amplifying returns for investors following a market-cap weighted investment approach.

he strong performance of US equities in recent years has been a major driver of global equity returns. On a market-cap weighted basis, US equities now represent 68% of the MSCI ACWI (as at 31 August 2025) and within the MSCI USA Index, the 'Magnificent Seven' tech giants account for more than one-third of the index – a testament to their

However, while elevated valuations among the ‘Magnificent Seven’ are well documented, the continued stream of strong returns has reinforced the belief that their growth story will simply run on and on. Yet, this narrative risks overlooking valuation concerns that could challenge future performance.

Let’s think about this for a moment. We know US equities now account for a staggering 66% of the global equity index – that is up from 58% five years ago and 52% a decade ago. So, what will that figure be in ten years? They are highly unlikely to experience the same growth as over the last decade and climb to 78%.

Even if there is no further growth – that 66% figure represents significant concentration risk being absorbed into portfolios that follow a market-cap weighted approach and a high allocation to one single currency diluting the typical benefits of broad diversification. Surely, investment decisions should be guided by a more forward-looking and rational assessment of future market dynamics, with greater attention paid to other regions and sources of diversified growth?

Elevated valuations

As noted above, the MSCI USA Index has just reached another all-time high and has delivered a total return of 10.9% in US dollars so far this year (as at 31 August 2025). However, for sterling-based investors, the return over the same period has been only 2.8%, reflecting the impact of the weaker dollar. This divergence underscores how currency fluctuations can materially affect investment outcomes – even when the underlying asset performs strongly.

When the dollar depreciates, the value of US equity gains diminishes when converted back into a stronger sterling, meaning investors can actually see losses in sterling terms despite positive performance in local currency. While the reverse can also be true during periods of dollar strength, this dynamic highlights the hidden risks that can arise from concentrated exposure to a single region and currency, and further underscores the importance of diversification on different levels.

The unintended consequence of currency moves

A forward-looking investment approach would naturally result in a lower allocation to US equities compared to solutions adopting a market-cap weighted approach. However, it is not just about geographic and currency exposure – it is about ensuring the portfolio remains aligned with the risk appetite of the investor. By continuously adapting to evolving market conditions and future expectations, risk-targeted strategies offer a more robust framework for managing uncertainty and delivering consistent outcomes. So, the theory is sound, but let’s consider a real-life example by looking at the Quilter WealthSelect Managed Active 5 Portfolio and considering its risk-targeted objective.

The asset allocation approach taken by the portfolio managers is intentionally dynamic. They rebalance the portfolio quarterly but have the flexibility to undertake ad hoc tactical rebalances at their discretion to take advantage of market opportunities or manage risk. The rebalances also involve reviewing forward-looking capital market assumptions to ensure an optimal strategic asset allocation remains in place over the long term. This forward-looking approach allows the portfolio management team to implement their investment conviction, whilst also keeping a sharp focus on the risk profile over both the short and long term.

The importance of risk targeting

At each rebalance, the portfolio managers focus on ensuring the portfolio stays within its defined range of volatility on a forward-looking basis. The chart below illustrates how this discipline has been maintained since the launch of the WealthSelect Managed Active 5 Portfolio in 2014.

By consistently aligning the portfolio with the risk appetite of the investor and maintaining the flexibility to evolve asset and regional equity market allocation as market conditions shift, risk-targeted solutions can provide a resilient framework for navigating future uncertainty. This dynamic approach helps ensure portfolios remain appropriately positioned, even as markets become more volatile or unpredictable.

Staying inside the lines

Strategies that rely on a market-cap weighted approach to regional equity allocation have undoubtedly benefitted from elevated exposure to US equities in recent years. However, with markets encountering increased uncertainty, the need to prepare for what lies ahead has never been greater. In this context, risk-targeted solutions – with their ability to adapt asset allocation in a controlled and forward-looking manner – may be best positioned to deliver resilient outcomes in an evolving investment landscape.

Meeting future challenges

Despite ongoing political uncertainty and a sharp decline in the value of the dollar, US equities have continued their upward trajectory. However, with stock valuations hovering near historic highs, some multi-asset investment strategies that adopt a market-cap approach to regional equity markets may be exposed to elevated risks.

represent 68% of the MSCI ACWI (as at 31 August 2025) and within the MSCI USA Index, the 'Magnificent Seven' tech giants account for more than one-third of the index – a testament to their extraordinary growth. It is also interesting to observe that in 2015, the top ten holdings in the index were diversified across various sectors whereas it is now much more concentrated on tech stocks riding the artificial intelligence wave. This surge has been nothing short of remarkable, reshaping the global equity landscape and significantly amplifying returns for investors following a market-cap weighted investment approach.

If you would like to find out more about Quilter WealthSelect, tap here.

he strong performance of US equities in recent years has been a major driver of global equity returns. On a market-cap weighted basis, US equities now

Information valid at the date of campaign. Tax regimes, bases and reliefs may change in the future. Rathbones Group Plc is independently owned, is the sole shareholder in each of its subsidiary businesses and is listed on the London Stock Exchange. Issued and approved by Rathbones Investment Management Limited, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered office: Port of Liverpool Building, Pier Head, Liverpool L3 1NW, Registered in England No. 01448919. Rathbones is the trading name of Rathbones Investment Management Limited. Rathbones Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Registered office: 30 Gresham Street, London EC2V 7QN, Registered in England No. 02376568. The Rathbones Model Portfolio Service is managed by Rathbones Investment Management Limited, while Rathbones Asset Management is responsible for managing the underlying building block funds. Both companies are part of Rathbones Group plc. This information has been prepared by Rathbones Group Plc. The information contained within this information is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. Any opinions expressed are not necessarily the views held throughout Rathbones Group Plc. Rathbones Group Plc is under no obligation to update the information contained in this material. No part of this video may be reproduced in any manner without prior permission. © 2025 Rathbones Group Plc. All rights reserved.

In this video, the team at Rathbones shares how its MPS service is structured to deliver clarity and consistency for advisers and their clients.

Gerry Lawlor, Business Development Director, David Coombs, Head of Multi-Asset Investments, Andrea Yung, Investment Director, and Will McIntosh-Whyte, Fund Manager, discuss Rathbones’ approach to MPS, outlining the four pillars that underpin their strategy:

Watch the video below to view the discussion in full.

Investment philosophy A unique investment solution Efficiency Value and service

Click here to explore how the new Rathbones MPS can support your advice process.

What next?

Rathbones’ senior team discusses the four pillars that underpin their MPS service and how the proposition aims to help clients invest well – and live well.

Tap here to explore how the new Rathbones MPS can support your advice process.

Andrea Yung, Investment Director

“Because the majority of rebalancing and repositioning takes place inside the underlying funds, the risk of CGT crystallisation at client level is dramatically reduced”

“Quarterly rebalancing or tactical fund changes can all inadvertently crystallise gains”

he sharp reduction in the annual exempt amount for capital gains tax (CGT) has prompted fresh scrutiny of how portfolio changes affect clients, especially those with general investment accounts. The structure of the re-launched Rathbones MPS helps mitigate many of the issues advisers face when it comes to CGT, offering a cleaner, more controllable way to manage risk and return.

In most traditional MPS portfolios, changes to asset allocation or fund selection are implemented by switching between third-party funds. That might mean:

Why traditional MPS models can trigger unnecessary gains

At Rathbones, we’ve taken a different approach. Rather than blending multiple third-party funds, we construct each MPS portfolio using three purpose-built in-house funds aligned to our Liquidity, Equity-type risk and Diversifiers (LED) framework.

Because each of these funds is a portfolio in itself, many of the active decisions – such as switching holdings, adjusting sector exposure or responding to market shifts – take place within the funds. These internal trades do not crystallise CGT for the end investor.

The only time a CGT event might be triggered is if the weightings between the Liquid, Equity-type risk and Diversifier funds change – and this happens much less frequently than the typical rebalancing or fund switching seen in conventional MPS solutions.

The result can offer a cleaner, more tax efficient experience for clients and may reduce admin for you.

A structure designed to reduce CGT crystallisation events

From £12,300 in 2022/23 to just £3,000 today, the cut in the CGT annual exemption has been swift and steep. While the majority of portfolios may sit within tax wrappers, clients with general investment accounts (GIAs) are now more exposed to the tax implications of everyday investment decisions.

While many investors are keenly aware of positioning when they first invest, less are interested in how this positioning develops over time.

Quarterly rebalancing or tactical fund changes can all inadvertently crystallise gains. As many advisers have seen first-hand, this can result in:

With the Financial Conduct Authority (FCA) placing increased emphasis on outcomes and value for money, CGT events caused by inefficient portfolio structures are fast becoming a compliance concern as well as a client service issue.

These changes, however routine, can trigger a CGT liability if they’re made within a GIA and the client has already used their allowance. Because those changes happen at model level, there’s often little opportunity to tailor or delay them to suit the individual client’s tax position.

Unexpected tax bills for clients Difficult conversations at review time Time-consuming reporting and suitability documentation

• • •

Selling one fund and buying another to reflect a new market view Rebalancing between asset classes by adjusting external fund weights Switching between similar funds that have different sector tilts or regional exposures

Because the majority of rebalancing and repositioning takes place inside the underlying funds, the risk of CGT crystallisation at client level is dramatically reduced. That means:

Easier for clients, easier for compliance

It also makes it easier to demonstrate ongoing value – a growing expectation in light of FCA guidance.

Fewer tax calculations and CGT reporting requirements Less client confusion at review time Greater consistency across your GIA book A clearer audit trail that supports Consumer Duty and suitability

Of course, no MPS structure can eliminate CGT entirely. But the Rathbones approach is designed to reduce unnecessary crystallisation and give advisers greater confidence in the underlying mechanics.

It’s a structural advantage that’s especially helpful for clients who:

As tax allowances become tighter, structures that help minimise friction and reduce CGT crystallisation events are likely to become more attractive – and more defensible.

Andrea is responsible for the portfolio management of Rathbones' MPS on Platforms service. Using a structured and disciplined investment framework, her primary focus is delivering outcomes that align with the objectives and risks associated with each MPS strategy.

Not CGT-free, but CGT-aware

Are near or over the CGT threshold Have legacy investments in GIAs

CGT is now harder to avoid and harder to manage

Rathbones is a trading name of Rathbones Investment Management Limited, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Registered office: Port of Liverpool Building, Pier Head, Liverpool L3 1NW. Registered in England no. 01448919.

Watch our Insight >

Rathbones’ Andrea Yung, Investment Director, discusses a smarter structure to reduce unnecessary crystallisation and simplify planning.

he sharp reduction in the annual exempt amount for capital gains tax (CGT) has prompted fresh scrutiny of how portfolio changes affect clients,

especially those with general investment accounts. The structure of the re-launched Rathbones MPS helps mitigate many of the issues advisers face when it comes to CGT, offering a cleaner, more controllable way to manage risk and return.

Ryan Paterson, Portfolio Manager

“With the increasing sophistication of investment strategies and the ability to adapt to market changes, many liquid alternatives have outperformed traditional assets over different time horizons”

“The ability to quickly enter and exit positions enhances agility in portfolio management, allowing portfolio managers to respond quickly to changing market conditions”

raditional investment strategies can fall short in navigating the complexities and volatility of today’s financial markets. Consequently, portfolio managers are increasingly turning to liquid alternative assets as a compelling solution for enhancing performance and diversification.

While the benefits of liquid alternatives are clear, there are significant access and ownership challenges that must be addressed to fully realise their potential:

We believe that integrating liquid alternatives into portfolios delivers compelling benefits: enhanced diversification, access to innovative strategies, and more robust risk management - ultimately strengthening long-term performance potential.

As markets continue to evolve in complexity, it is increasingly important that investors have both access to, and a clear understanding of, the benefits liquid alternatives can offer. To support this need, we launched the Schroder Alternative Portfolio in September 2023, designed to help investors unlock the full potential of these assets. Read the next article for a closer look at how this fund can strengthen the resilience of your clients’ model portfolios.

The challenges facing alternatives

Liquid alternatives encompass a wide array of investment strategies that are not confined to the traditional categories of stocks and bonds. This includes hedge funds, managed futures, commodities, real estate investment trusts (REITs), and other instruments that offer daily liquidity.

There are five key benefits of using liquid alternatives:

1. Enhanced diversification: a smarter way to manage risk Liquid alternatives are not directly correlated with equities and bonds and can help mitigate risk during fluctuating economic conditions and improve risk-adjusted returns. For instance, while equities may decline during market downturns, liquid alternatives such as commodities or hedge funds, may perform differently, thereby smoothing out overall portfolio performance.

2. Access to non-traditional strategies: broadening the investment horizon Including liquid alternatives offers exposure to a diverse range of investment strategies that are typically inaccessible through traditional asset classes. This includes alternative risk premium, long/short equity, and global macro strategies. This enables portfolio managers to take advantage of niche opportunities and trends that traditional investments may overlook, potentially boosting returns.

3. Flexibility and liquidity: agility without the compromise Liquid alternatives provide investors with flexibility and immediate access to their capital, in contrast to many traditional hedge funds with lengthy lock-up periods. The ability to quickly enter and exit positions enhances agility in portfolio management, allowing portfolio managers to respond quickly to changing market conditions. This liquidity is particularly beneficial during periods of heightened uncertainty, when swift action can help to capitalise on emerging opportunities or to safeguard against losses.

4. Risk management: strengthening portfolio resilience Liquid alternatives can strengthen a portfolio by improving risk management. They use tools like options, swaps, and futures to protect against market downturns. They also utilise advanced models to assess exposure to various risk factors, such as market risk, credit risk, liquidity risk, and others, enabling managers to identify and mitigate potential vulnerabilities in their portfolios.

5. Competitive performance: delivering results in diverse market conditions Historically, liquid alternative assets have demonstrated a capacity for competitive performance in various market environments. With the increasing sophistication of investment strategies and the ability to adapt to market changes, many liquid alternatives have outperformed traditional assets over different time horizons. This potential for alpha generation makes them an attractive addition to portfolios, particularly in a low-return environment.

1. Access challenges

High minimum investments: this is one of the most common barriers to accessing liquid alternatives which can exclude individual investors and smaller institutions. Limited availability on platforms: hedge funds often do not appear on UK investment platforms due to regulation, targeting, complex strategies, liquidity preferences, cost structure, and capacity. Regulatory barriers: some funds may only be available to accredited investors and face strict compliance rules.

2. Ownership challenges

Lack of transparency: information about strategies, performance, and fees is often limited and this lack of transparency can deter potential investors. Complex strategies: hedge funds often use complex investment strategies that include leverage, derivatives, and short selling. These strategies may be difficult for retail investors to understand. As a result, hedge funds may prefer direct relationships with their investors, ensuring that those involved fully understand the risks and complexities associated with their investments. Due diligence requirements: by thoroughly researching managers, understanding strategies, evaluating risk management frameworks, and maintaining continuous oversight, investors can make informed decisions that align with their investment objectives.

Liquid alternatives: expanding the investment toolkit

Important Information Marketing material for professional clients only. The views and opinions contained herein are those of the author and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. This information is not an offer, solicitation or recommendation to buy or sell any financial instrument or to adopt any investment strategy. Nothing in this material should be construed as advice or a recommendation to buy or sell. Information herein is believed to be reliable but we do not warrant its completeness or accuracy. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. No responsibility can be accepted for error of fact or opinion. Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy. Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at www.schroders.com/en/privacy-policy or on request should you not have access to this webpage. For your security, communications may be recorded or monitored. Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority. 07751.

Click here to read our latest insights or to find out more about Schroder Investment Solutions. Alternatively, contact your usual Schroders’ representative or call our Business Development Desk on 0207 658 3894.

Ryan Paterson, Portfolio Manager at Schroder Investment Solutions, explores how liquid alternatives can enhance diversification, improve resilience, and open up opportunities beyond traditional markets.

Tap here to read our latest insights or to find out more about Schroder Investment Solutions. Alternatively, contact your usual Schroders’ representative or call our Business Development Desk on 0207 658 3894.

raditional investment strategies can fall short in navigating the complexities and volatility of today’s financial markets. Consequently, portfolio managers are

increasingly turning to liquid alternative assets as a compelling solution for enhancing performance and diversification.

Risk considerations ABS and MBS risk: The fund may invest in mortgage or asset-backed securities. The underlying borrowers of these securities may not be able to pay back the full amount that they owe, which may result in losses to the fund. Contingent convertible bonds: The fund may invest in contingent convertible bonds which are bonds that convert to shares if the bond issuer's financial health deteriorates. A reduction in the financial strength of the issuer may result in losses to the fund. Currency risk: The fund may lose value as a result of movements in foreign exchange rates, otherwise known as currency rates. Derivatives risk: Derivatives, which are financial instruments deriving their value from an underlying asset, may be used to manage the fund efficiently. The fund may also materially invest in derivatives including using short selling and leverage techniques with the aim of making a return. A derivative may not perform as expected, may create losses greater than the cost of the derivative and may result in losses to the fund. High yield bond risk: High yield bonds (normally lower rated or unrated) generally carry greater market, credit and liquidity risk meaning greater uncertainty of returns. Interest rate risk: The fund may lose value as a direct result of interest rate changes. Liquidity risk: In difficult market conditions, the fund may not be able to sell a security for full value or at all. This could affect performance and could cause the fund to defer or suspend redemptions of its shares, meaning investors may not be able to have immediate access to their holdings. Market risk: The value of investments can go up and down and an investor may not get back the amount initially invested. Multi-Manager risk: The fund allocates capital to multiple strategies managed by separate portfolio managers who will not coordinate investment decisions, which may result in either concentrated or offsetting risk exposures. Operational risk: Operational processes, including those related to the safekeeping of assets, may fail. This may result in losses to the fund. Performance risk: Investment objectives express an intended result but there is no guarantee that such a result will be achieved. Depending on market conditions and the macro economic environment, investment objectives may become more difficult to achieve. Private Assets risk: Investments in private assets carry greater counterparty and liquidity risk. As there is no active market for private assets, it could prove difficult to sell and objectively value the fund’s assets. The fund may have to lower the selling price, sell other investments or forego more appealing investment opportunities. The actual value may not be recognised until the assets are sold. Real estate and property risk: Real estate investments are subject to a variety of risk conditions such as economic conditions, changes in laws (e.g. environmental and zoning) and other influences on the market. Important Information Marketing material for professional clients only. The views and opinions contained herein are those of the author and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. This information is not an offer, solicitation or recommendation to buy or sell any financial instrument or to adopt any investment strategy. Nothing in this material should be construed as advice or a recommendation to buy or sell. Information herein is believed to be reliable but we do not warrant its completeness or accuracy. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. No responsibility can be accepted for error of fact or opinion. Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy. Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at www.schroders.com/en/privacy-policy or on request should you not have access to this webpage. For your security, communications may be recorded or monitored. Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority. 12496.

Click here to read our latest insights or to find out more about the Schroder Alternative Portfolio and Schroder Investment Solutions. Alternatively, contact your usual Schroders’ representative or call our Business Development Desk on 0207 658 3894.

“At the heart of our investment approach is a simple belief: markets are not perfectly efficient”

“Alpha is only valuable if it can be sustained. Repeatability comes from discipline and process”

1.95

-0.81

0.13

0.02

1.39

2.39

Return

Schroder Alternative portfolio

Std Dev

Worst month

Correlation

Sharpe ratio

Sortino ratio

Beta

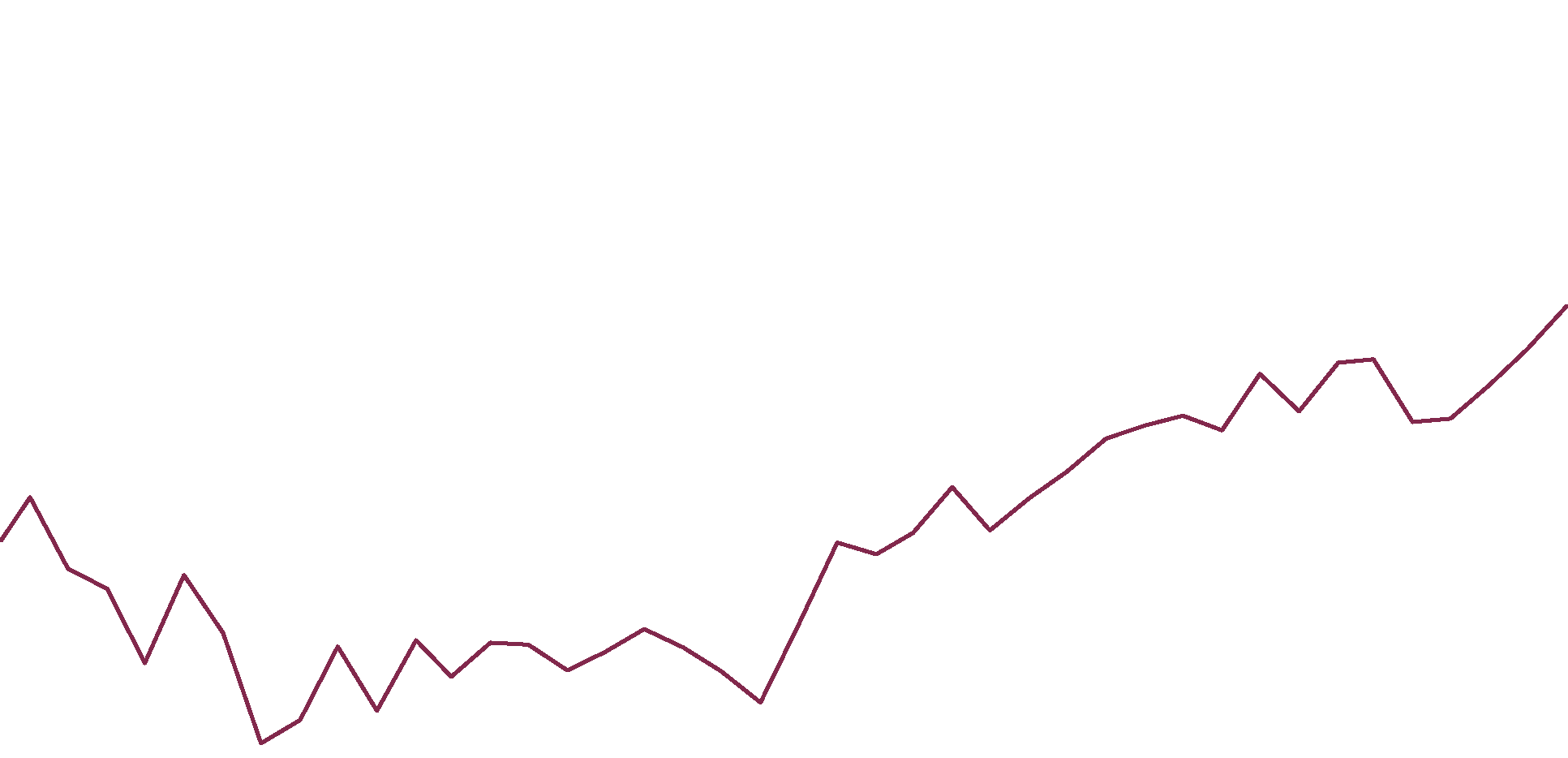

Past performance is not a guide to future performance and may not be repeated. Source: Morningstar Direct, as at 31.08.2025. All returns in GBP net of fees using monthly return series. Inception date 01.09.2023. Return is annualised. Risk metrics measured relative to MSCI ACWI.

Risk and return characteristics

-

5.7

8.3

6.8

CE BofA Sterling 3-Month Government Bill Index plus 2%

Aug 20 - Aug 21

Discrete performance

Aug 21 - Aug 22

Aug 22 - Aug 23

Aug 23 - Aug 24

Aug 24 - Aug 25

Past performance is not a guide to future performance and may not be repeated. Source: Morningstar as at 31.08.25. Calculated based on model portfolio returns net of costs. Cumulative returns apply to all periods. Since Inception 01.09.23.

fund, offering professional management and diversified exposure across a range of liquid alternative strategies. Moreover, the fund’s multi-manager structure of varied liquid alternative strategies can deliver enhanced diversification benefits that surpass those of any individual strategy.

At the heart of our investment approach is a simple belief: markets are not perfectly efficient. Across asset classes and strategies, there are pockets of opportunity where skilful investors can generate excess returns. We believe this alpha is best captured by combining specialist expertise with diversification. Each of our alternative managers focuses on a specific strategy where they have proven insight and edge—whether in trend following, macro, event-driven, or equity long/short. By bringing these managers together in one structure, we diversify the sources of return while reducing reliance on any single theme or style.

Harnessing specialist expertise for Alpha

Alpha is only valuable if it can be sustained. Repeatability comes from discipline and process. We select managers with clear, well-defined strategies, supported by strong research and infrastructure. Our oversight ensures they remain true to their approach, while our risk management and liquidity controls provide stability across market environments. This institutional framework means we are not dependent on short-term calls or luck, but on a consistent, research-driven process that can adapt and endure.

A robust investment process

The fund is designed to be highly liquid, with daily dealing, and aims to maintain a low correlation to traditional asset classes such as equities and bonds. Each holding is classified as either a diversifier, return enhancer or risk mitigator, allowing dynamic allocation based on market conditions. This flexible and diversified approach enables the portfolio to adapt to changing market environments while maintaining a focus on delivering stable, risk-adjusted returns.

Flexibility and adaptability at the core

By leveraging our expertise and commitment to innovation, we aim to meet the complex needs of our clients, providing an investment solution that addresses both current market challenges and future opportunities. As at the end of August 2025, the fund has delivered an annualised return since inception of 7.73% with low levels of volatility and correlation to traditional asset classes.

Consistent performance through innovation

As a core holding within our model portfolios, the Schroder Alternative Portfolio provides true diversification through a multi-manager structure and dynamic allocation across complementary strategies. This forward-thinking approach helps clients navigate complex markets and effectively manage risk, ensuring our model portfolios are built to address evolving investor needs with greater flexibility and resilience.

Final thoughts

he Schroder Alternative Portfolio was launched on 1 September 2023 to make liquid alternative investing more accessible and transparent for clients. This fund serves as a core component within our Schroder Investment Solutions model portfolio range. It addresses common access and ownership challenges through a multi-manager

Portfolio manager Ryan Paterson explores how the Schroder Alternative Portfolio is helping investors achieve greater resilience and diversification through a disciplined, multi-manager approach.

Tap here to read our latest insights or to find out more about the Schroder Alternative Portfolio and Schroder Investment Solutions. Alternatively, contact your usual Schroders’ representative or call our Business Development Desk on 0207 658 3894.

Xxxxxxxxx Xxxxxxxx xxxxxxx xxxxxx xxxxxx xxxxx

he Schroder Alternative Portfolio was launched on 1 September 2023 to make liquid alternative investing more accessible and transparent for clients.

This fund serves as a core component within our Schroder Investment Solutions model portfolio range. It addresses common access and ownership challenges through a multi-manager fund, offering professional management and diversified exposure across a range of liquid alternative strategies. Moreover, the fund’s multi-manager structure of varied liquid alternative strategies can deliver enhanced diversification benefits that surpass those of any individual strategy.

Investment risk information The value of investments, and the income from them, may fall or rise and investors may get back less than they invested. Important information This article is designed for use by, and is directed only at persons resident in the UK. The information contained in this article is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this article when making any investment decisions. The information contained in this article is for educational purposes only and is not a recommendation or solicitation to buy or sell investments. © 2025 Vanguard Asset Management, Limited. All rights reserved. Vanguard Asset Management, Limited is authorised and regulated in the UK by the Financial Conduct Authority.

Click here to view more on The value of personalised advice in the UK

Cash flow simulation

Highly personalised, tax-aware foundation

VCMM return simulations

10,000 market return and inflation scenarios

Life expectancy variability

"True success rates" including survivor scenarios

Utility-based scoring

Focus on the entire range of outcomes, with emphasis on mitigating tail risks

The sources of advice value

Source: Vanguard.

Figure 2. To measure value, compare the advised alternative to a baseline

Establish a baseline model: What will an investor do absent the advice interventions that we want to measure?

Model the interventions: Once a baseline is established, we can change the modelled outcomes by adding the advice interventions we want to value. How does the range of potential outcomes improve when we undertake the suggested interventions?

Add to the baseline model to match value: Return to the original baseline model and determine how much additional wealth or extra annual return the investor would need to achieve across a distribution of outcomes, using their current approach, that is equivalent to the advised alternative.

Figure 1 provides examples of the four different sources of advice value within the framework.

Goal planning • Saving and spending • Income planning • Planning for bad outcomes • Multigenerational planning

Encouraging to stay on track Adjusting for changing goals Avoiding performance chasing and panic selling Getting family members on the same page

Emotional support • Instilling confidence • Understanding life aspirations • Being responsive

Administrative support • Data gathering • Summarising/reporting • Researching potential opportunities

INTERVENTION - ORIENTED

PROCESS - ORIENTED

Portfolio management • Risk assessment • Asset allocation • Investment selection • Controlling costs

Using tax-advantaged accounts Asset location Making efficient use of lower income tax bands Harvesting capital gains/ using tax allowances

Tax planning

Behavioural coaching

“Identifying the right set of advice interventions for your client and their situation is critical to maximising your value”

Warwick Bloore, Senior Specialist, Advisory Research Centre, Vanguard, Europe

“Through regular engagement, you will earn the trust of your clients, which is one of the primary drivers of successful long-term advisory relationships”

n this article, we consider the key findings from the Vanguard paper, The value of personalised advice , which offers a methodology for measuring the value of advice for an individual client. By quantifying the value of your advice you can, more easily, convey the benefits to new and existing clients, ensuring they understand how you offer value over and above your fees.

I

Vanguard has expanded its original three-pillar value of advice framework to include a fourth dimension – time savings:

Financial value: advisers help investors to meet their financial goals and overcome obstacles and challenges along the way. Portfolio value: building a well-diversified portfolio matched to the client’s risk tolerance. Emotional value: helping investors achieve financial wellbeing or peace of mind and instilling confidence in them. Time savings value: performing tasks for your clients that they may not have the capacity or knowledge to undertake themselves.

You can maximise your value with individual clients by matching the advice interventions in each of the four pillars that are likely to provide them with the most value in the most efficient manner. In many ways, your most valuable task is choosing which advice opportunities you should implement with each client.

A new framework for valuing advice

Whilst financial value and portfolio value are most often delivered through the specific interventions that you recommend to your clients, emotional value and time value are most often delivered through the ongoing process of regularly engaging with your clients and monitoring their portfolios. Through this regular engagement, you will earn the trust of your clients, which is one of the primary drivers of successful long-term advisory relationships.

Examples of ongoing emotional and time-value activities that you may undertake for your clients could include:

Following up with clients to ensure they are saving as much as they need to. Showing clients how their investment plans will give them the flexibility to spend and enjoy life. Educating clients through times of economic euphoria and turmoil.

Personalisation: The VFAM assesses value at the individual level and accounts for differences in client tax brackets and other attributes. This means that the value of advice interventions can be calculated on an individual basis. Additionally, it can help advisers discover and prioritise higher-value interventions for individual clients and assist in decision-making conversations. Multi-strategy effects: Whilst each potential advice intervention can add value in isolation, measuring a set of interventions together won’t necessarily equate to a total value which is the sum of its parts. Sometimes multiple interventions can overlap, whilst others can work together to create superior outcomes. Distributional outcomes: The VFAM method explicitly values each possible outcome and weighs them appropriately. It also explicitly accounts for the variability of life-expectancy outcomes whereas most advice conventions project to a given age. Utility-based scoring: At Vanguard we believe that utility-based scoring provides a better measurement of value for individual clients.

Advice as an ongoing process

For your clients to engage with you, they are undertaking an emotional, as well as a financial, commitment. Understanding your clients' needs, goals, values, objectives and lifestyle will enable you to craft a tailored and personalized investment plan that aligns with their views. By engaging with your clients in this way, you are reassuring them that your advice and offering is designed and personalized for them. If your clients does not feel that you understand their needs, it is unlikely that they will be confident in your ability to deliver results.

At Vanguard, our research shows that the more personal an advice plan is, the more value it can deliver.

Why is personalisation important?

To assist you in using our new framework, Vanguard has developed a three-step process for measuring the value of a set of advice interventions for individual clients relative to their existing ‘baseline’ investment strategy. The process can also be used to discover higher-value advice opportunities that can assist clients in their decision-making .

How to measure the value of your advice

The Vanguard Financial Advice Model (VFAM) was developed in conjunction with our new framework to enable calculations of value provided by advice for individual clients relative to their current investment and financial planning strategies.

To calculate the value of a specific set of advice interventions, VFAM draws on the unique needs and goals of the individual client, taking into account the tax and regulatory landscapes of the client’s home market. The model’s results are primarily expressed in terms of the annualised return value provided to the individual investor, in basis points (a basis point is a hundredth of a percentage point), as well as in 'windfall equivalent dollars' — the amount that would need to be added to a taxable account held by the individual today — as an alternative measure.

Currently, the VFAM is configured to calculate the value of advice for US-based investors only. UK and European versions of the VFAM are under development. In the interim, there is more information about the model in the diagram below:

The Vanguard Financial Advice Model

The VFAM approach improves on traditional metrics in the following ways:

The benefits of the VFAM measurement approach

Traditional financial planning often uses a “portfolio success rate” to measure results and score a portfolio’s preparedness, as well as the quality of the financial planning strategy or decision. While a portfolio success rate is useful for conveying the longevity of a portfolio at a specific age, it has clear shortcomings. With the VFAM, we use a utility framework to score the lifetime spending and bequest distributions of a client’s baseline and advised scenarios.

In essence, utility scoring is not strictly a measure of wealth, but rather of the life satisfaction or usefulness that wealth can provide. When considering utility scoring, greater wealth does not necessarily lead to greater outcomes for your client.

Utility scoring does not simply recommend the best average outcome; it also penalises strategies that risk extremely negative outcomes. The VFAM model considers these downside risks and chooses options that result in utility maximisation across a wide range of potential outcomes.

Utility-based scoring: a more meaningful measure of success

Financial advisers provide value in many ways, but by making the value measurable, you can improve client outcomes, attract new clients and retain your existing clients in the long-term. To provide the most valuable advice, however, the key is to understand and know your client so that your advice can be tailored to their goals and aspirations along with being structured to manage their behaviours and keep them on track.

Identifying the right set of advice interventions for your client and their situation is critical to maximising your value. Measuring this is a key way to help you discover the most valuable advice recommendations and also to communicate to your clients the value of following through.

Conclusion

1. The value of personalised advice, Vanguard, 2022.

1

2. The value of personalised advice, Vanguard, 2022.

The question ‘what is the true value of financial advice?’ is of huge importance to financial advisers. According to Vanguard, the answer must consider several key points.

client. By quantifying the value of your advice you can, more easily, convey the benefits to new and existing clients, ensuring they understand how you offer value over and above your fees.

n this article, we consider the key findings from the Vanguard paper, The value of personalised advice , which offers a methodology for measuring the value of advice for an individual

Tap here to view more on The value of personalised advice in the UK

Click here to explore more articles in Vanguard 365

“While advisers may enjoy a solid relationship with a client, they might not have the same bond with the client’s partner or children”

By 2030, a projected $18.3trn in wealth will be transferred globally and by 2050 we expect £7 trillion to pass between generations in the UK alone . Several factors are driving this transfer, including an ageing population, increased wealth concentration and longer life expectancies.

The great wealth transfer presents an opportunity and a challenge for both inheritors and advisers. Previous research in the US has indicated that up to 70% of wealthy families lose their wealth by the next generation and as many as 90% lose their wealth by the third generation.

Good financial advice and planning services can help preserve wealth across generations, but further research suggests that inheritors—usually a female spouse and/or children—tend not to use the same financial adviser as their partner or parents, and in some cases do not use an adviser at all.

The research indicates that advisers often neglect to sufficiently engage with both partners in a relationship and often do not engage at all with the next generation, giving inheritors little incentive to retain their partner or parents’ advice provider after they receive an inheritance.

1. Wealth-X, “Preservation and Succession: Family Wealth Transfer 2021”.

2. Nasdaq, “Generational Wealth: Why do 70% of Families Lose Their Wealth in the 2nd Generation?”, 2018.

3. McKinsey, “Women as the next wave of growth in US wealth management”, 2020. 4. Cerulli, “The Cerulli Edge—U.S. Retail Investor Edition, 4Q 2023 Issue”, 2023.

3

4

To successfully navigate the great wealth transfer and help inheritors preserve wealth, not only must financial advisers be prepared to address a wide range of issues, including estate planning, retirement planning and investment management, but also develop an understanding of inheritor goals and preferences.

n the next few decades, the largest intergenerational transfer of wealth in history is expected to occur. The “great wealth transfer”, as it has been dubbed, will see a significant movement of assets to younger generations and is anticipated to have a profound impact on the financial sector, particularly within financial advice.

“Understanding generational and gender differences could be the key to retaining client trust”

In any scenario, wealth transfer is a complex process that requires advisers to deal with a number of challenges. For the client, planning may feel morbid and uncomfortable. They may struggle to decide how their assets should be disbursed or may disregard sound advice. Additional problems can arise in cases where a subject is elderly or otherwise vulnerable - and specialist legal support should be sought in such cases.

While advisers may enjoy a solid relationship with a client, they might not have the same bond with the client’s partner or children. Partners could have differing objectives – they may disagree with proposed inheritance, trust or succession structures, or have descendants they feel require additional support. Then there is the possibility of conflict among inheritors, with advisers required to play the role of mediator to facilitate open dialogue.

At the heart of wealth transfer is the emotional side of estate planning, particularly when family dynamics are complex. A significant challenge is harmonising the needs, values and aspirations of multiple inheritors while protecting the client’s interest at the same time. Advisers may need to play the role of financial educators, helping clients understand financial concepts such as asset allocation, risk management and tax planning.

The great wealth transfer challenge

As clients take steps to dispense their wealth to descendants, advisers should keep in mind the differing priorities of parents and children. For example, millennial and younger inheritors may prioritise accessible, digital advisory services; and have a contrasting set of tastes in investable assets; or may have a different degree of cost sensitivity and perception of where they see value compared with their parents.