Multi-asset in motion

From changing currency dynamics to shifting market leadership, global forces are reshaping how multi-asset portfolios deliver returns

present

Latest insights

Previous insights

READ THE ARTICLE

Dimitris Korovilas, Senior Investment Strategist at Vanguard, Europe explains why the merits of portfolio diversification, at the asset class and sub-asset class levels, are worth investigating for diligent investors.

Is portfolio diversification worth it?

READ THE ARTICLE

Vanguard’s Madison McCall and Claire Hsu explore why a weakening US dollar does not necessarily equal a weak US dollar.

What does the US dollar’s recent weakness mean for multi-asset investors?

READ THE ARTICLE

Dimitris Korovilas, Senior Investment Strategist at Vanguard, Europe explains why the merits of portfolio diversification, at the asset class and sub-asset class levels, are worth investigating for diligent investors.

Is portfolio diversification worth it?

READ THE ARTICLE

Vanguard’s Madison McCall and Claire Hsu explore why a weakening US dollar does not necessarily equal a weak US dollar.

What does the US dollar’s recent weakness mean for multi-asset investors?

In partnership with

RETURN TO HOMEPAGE

Multi-asset in motion

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time. The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the US Treasury and corporate fixed income markets, international fixed income markets, US money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

The primary value of the VCMM is in its application to analysing potential client portfolios. VCMM asset-class forecasts—comprising distributions of expected returns, volatilities, and correlations—are key to the evaluation of potential downside risks, various risk–return trade-offs, and the diversification benefits of various asset classes. Although central tendencies are generated in any return distribution, Vanguard stresses that focusing on the full range of potential outcomes for the assets considered, such as the data presented in this paper, is the most effective way to use VCMM output.

The VCMM seeks to represent the uncertainty in the forecast by generating a wide range of potential outcomes. It is important to recognise that the VCMM does not impose “normality” on the return distributions, but rather is influenced by the so-called fat tails and skewness in the empirical distribution of modelled asset-class returns. Within the range of outcomes, individual experiences can be quite different, underscoring the varied nature of potential future paths. Indeed, this is a key reason why we approach asset-return outlooks in a distributional framework.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results. The performance data does not take account of the commissions and costs incurred in the issue and redemption of shares.

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Important information

This is directed at professional investors and should not be distributed to, or relied upon by retail investors.

This is designed for use by, and is directed only at persons resident in the UK.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on it when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued by Vanguard Asset Management Limited, which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2025 Vanguard Asset Management Limited. All rights reserved.

Find out more about our multi-asset solutions

“Beyond the shock-absorbing benefits of global bonds, the higher interest rate environment has significantly improved the return outlook for bond markets”

“Taking the past-performance argument as an investment guide to its logical conclusion reveals the argument’s fallacy - you end up with a one-stock portfolio”

Past performance is not a reliable indicator of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Vanguard calculations, based on MSCI indices and historical equity data from Bloomberg, as at 31 December 2024. Performance calculated in GBP with gross income reinvested.

Notes: Charts show the final balance of a hypothetical £100 investment in the relevant MSCI indices and individual equities denominated in GBP for the 10 years ended 31 December 2024.

You can always find an asset that will outperform your portfolio

Dimitris Korovilas, Senior Investment Strategist at Vanguard, Europe explains why the merits of portfolio diversification, at the asset class and sub-asset class levels, are worth investigating for diligent investors.

Dimitris Korovilas,

Senior Investment Strategist, Vanguard

CONTRIBUTOR

As investors constantly seek new and improved sources of returns, global stock/bond portfolios can attract criticism from proponents of alternative investment strategies.

Some commentators question the diversification benefits of global bonds relative to global equities; and the merits of a global equity market exposure versus a more concentrated position, say, in US stocks.

It’s an age-old debate and one that merits a diligent investigation.

We’ll start by looking at the merits of maintaining an exposure to global bond markets before analysing the equity diversification point.

Managing risk

A core tenet of the 60/40 model is the risk-reducing benefits of broad market diversification and the negative return correlation between global equity and bond markets, with bonds historically rising when stock markets fall by more than 10% . Critics of the 60/40 model might be quick to highlight the negative returns posted by global equity and bond markets in 2022.

The scenario that came to pass in 2022 represented the first time that both equities and bonds had experienced negative returns in the same year since 1977 . This unwelcome positive correlation was driven largely by a sharp, unexpected increase in interest rates — but the negative relationship then resumed in 2023 .

While the case of 2022 was rare, when we look at the stock/bond return correlation over shorter time frames, we can see that the correlation can enter positive territory periodically , typically in response to economic shocks or surprises.

The spike in volatility in stock markets during April 2025, fuelled by the US administration’s international trade tariffs, offered a real-time example of the role of global bonds in a diversified portfolio. At the end of April, global equities were down 7% since the turn of the year, while global bonds were up 2% .

Beyond this episode demonstrating the shock-absorbing benefits of global bonds, it highlighted the higher interest rate environment has significantly improved the return outlook for bond markets. Long-term multi-asset investors can now expect higher returns from bond market exposures relative to the past 15 years .

Do you need global diversification?

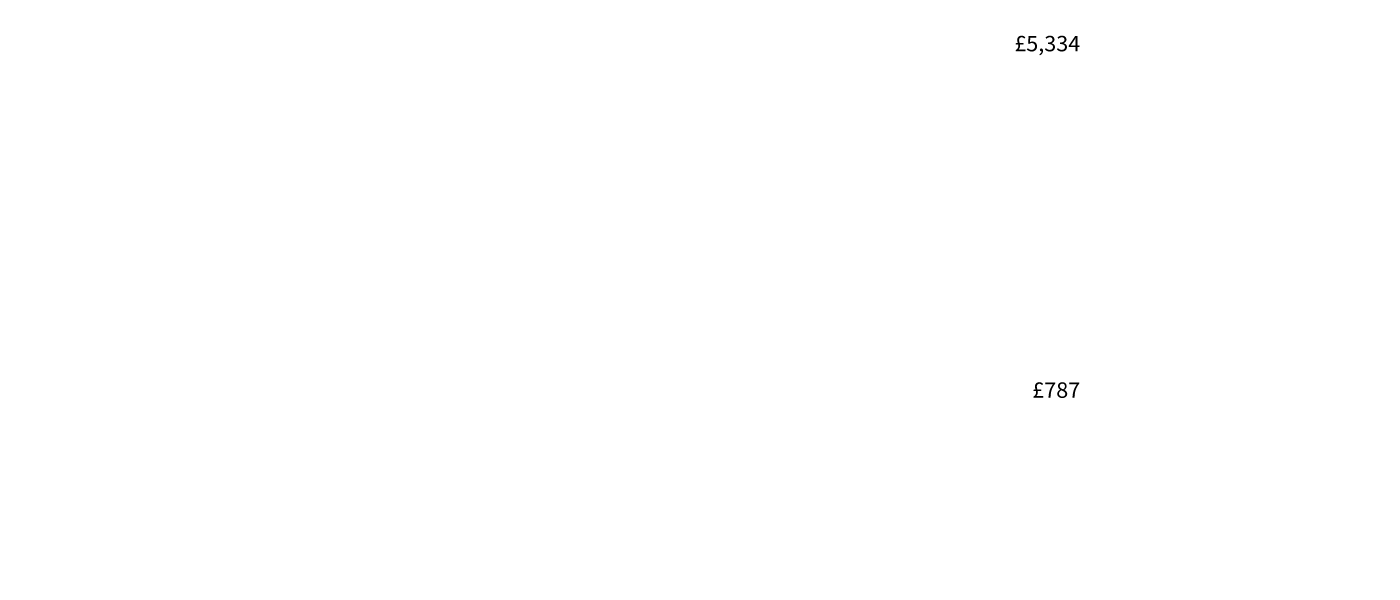

The outperformance of US equities in recent years might lead some investors to question the case for a globally diversified portfolio. After all, a £100 investment in US equities 10 years ago would have grown to £402 by the end of 2024 (an annualised 15% return) - more than twice the final balance of £193 (an annualised 7% return) for an equivalent investment in global ex-US equities .

But with that logic in mind, why stop with global diversification? The same argument could apply to all levels of portfolio diversification. Looking at market results over the 10 years ended 31 December 2024, why bother with broadly diversified US equity exposure when US growth stocks outperformed the broad US market by 1.4 times (£566 versus £402)? Why invest in value stocks at all?

Or given that the information technology sector, in turn, outperformed growth stocks by 1.4 times, why not just concentrate the entire equity portfolio in that sector? And why not further weed out the underperforming parts of the sector? The Magnificent Seven outperformed the IT sector by 6.8 times . And one stock, Nvidia, outperformed the collective return of the Magnificent Seven by 6.3 times.

Hedging the unknowable

Although diversification makes sense in any environment or time period, it may be particularly important now. Heightened geopolitical uncertainty is feeding into markets and volatility is likely to persist for some time.

Portfolio diversification with a strategic allocation to fixed income is one of the most potent strategies investors have to smooth portfolio returns over the long term. While market downturns are inevitable, patience and a steadfast commitment to a long-term investment strategy are crucial.

Sometimes, the most effective solutions are the simplest. A strategic allocation to global equities and global bonds has been found to give long-term investors a good chance of success .

Taking the past-performance argument as an investment guide to its logical conclusion reveals the argument’s fallacy - you end up with a one-stock portfolio.

1

2

3

4

5

6

7

8

9

Sources

1. Source: Bloomberg. Data are monthly total returns in USD from 01 January 1990 to 30 April 2023. Global equities are represented by the MSCI ACWI Index. Global bonds are represented by the Bloomberg Global Aggregate Index Value (USD Hedged). An equity market downturn is defined as a decrease of more than 10% from the previous maximum.

2. Source: Bloomberg. Note: Annual total returns calculated in USD from 1977 to 2022. For equities, we use US equities represented by the MSCI USA Index from 1977 to 1987 and global equities afterwards, represented by the MSCI ACWI Index. For bonds, we use US bonds represented by the Bloomberg U.S. Aggregate Index from 1977 to 1990 and global bonds afterwards, represented by the Bloomberg Global Aggregate Index Value (USD Hedged).

3. Source: Vanguard calculations in GBP, based on data from Refinitiv. Data between 1 January 2022 and 5 April 2023. Stocks are represented by the FTSE All-Share Total Return Index and bonds are represented by the Bloomberg Sterling Aggregate Bond Index.

4. Source: Vanguard calculations in GBP, based on data from Refinitiv, as at 17 January 2025. correlation of daily stock and bond returns over 60 business days and over 504 business days since 1 January 2002. Stocks are represented by the FTSE All-Share Total Return Index and bonds are represented by the Bloomberg Sterling Aggregate Bond Index. Data for the Bloomberg Sterling Aggregate Bond Index starts on 30 March 2000. It is not uncommon for the correlation between stocks and bonds to turn positive over the shorter term, but this has not altered the longer-term negative relationship.

5. Vanguard calculations based on Bloomberg data. Global equities represented by the FTSE All-World Index GBP. Global bonds represented by the Bloomberg Global Aggregate Float-Adjusted Index GBP Hedged. Data between 1 January 2025 and 29 April 2025.

6. Source: Vanguard calculations based on the Vanguard Capital Markets Model (VCMM). Global bonds based on the Bloomberg Global Aggregate Index (GBP Hedged). Distribution of 10-year annualised return outcomes in GBP from the VCMM are derived from 10,000 simulations for each modelled asset class.

7. Returns in all the scenarios are based on our calculations using the relevant MSCI indices denominated in GBP over 10 years ended 31 December 2024.

8. The Magnificent Seven are the seven stocks that have driven much of the market’s returns over the past few years: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla.

9. For example, see Gary P. Brinson, L. Randolph Hood, and Gilbert L. Beebower, 1995. ‘Determinants of portfolio performance.’ Financial Analysts Journal 51(1):133–8. (Feature Articles, 1985–1994).

Is portfolio diversification worth it?

RETURN TO HOMEPAGE

Multi-asset in motion

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Important information

This is directed at professional investors and should not be distributed to, or relied upon by retail investors.

This is designed for use by, and is directed only at persons resident in the UK.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offe\r or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on it when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued by Vanguard Asset Management Limited, which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2025 Vanguard Asset Management Limited. All rights reserved.

Find out more about our multi-asset solutions

“We encourage investors with a long-term horizon and wealth accumulation or preservation goals to hold global equities unhedged and global bonds hedged”

“With the dollar now fairly valued and US equity valuations looking stretched, future US equity returns may be more muted for sterling-based investors”

Vanguard’s Madison McCall and Claire Hsu explore why a weakening US dollar does not necessarily equal a weak US dollar.

Past performance is not a reliable indicator of future returns.

Source: Chart based on data from Refinitiv and the International Monetary Fund, as at 9 July 2025.

Notes: The chart shows our fair-value estimate for the US dollar against an equity market capitalisation-weighted basket of the euro, the Japanese yen, the British pound, the Canadian dollar and the Australian dollar. The fair-value estimate is based on the part of exchange-rate movements that can be explained through differentials in relative economic strength, measured by productivity (GDP per capita at purchasing power parity) and long-term real rates.

The dollar returns to fair value for the first time since 2021

Past performance is not a reliable indicator of future returns.

Source: Bloomberg and Vanguard calculations, chart data as at 17 June 2025.

The US dollar has weakened against major currencies in 2025

A weakening US dollar does not equal a weak US dollar

In 2025, headlines have been dominated by the weakening of the US dollar. Yet, beneath the surface of short-term fluctuations lies a more enduring truth: the US dollar remains the most-used currency in the global financial system . While recent depreciation has implications for investors, that does not necessarily imply that the US dollar is weak.

Sources

1. Source: Vanguard and Bank of England.

2. What the decline of the US dollar means for investors - Lukas Brandl-Cheng, Investment Strategist Analyst, Vanguard Europe and Ian Kresnak, Investment Strategist Analyst, Vanguard US.

3. Note: FX reserves refer to foreign currency assets held by central banks to support monetary policy and currency stability. International debt includes bonds issued by a country’s residents in foreign markets or currencies. International loans are cross-border lending arrangements between institutions or governments. SWIFT (Society for Worldwide Interbank Financial Telecommunication) tracks global financial messaging flows, often used as a proxy for currency usage in international payments. Source: Bloomberg Intelligence, ECB, IMF COFER, SWIFT, BIS. Data as at April 2025 (SWIFT), Q4 2024 (Reserves), Q4 2023 (Debt & Loan) as at June 2025.

The slide in the US dollar’s value has been driven by a mix of economic cooling, geopolitical uncertainty and the April 2025 announcement of new US trade tariffs (see the first chart below). Historically, such uncertainty has typically led to a strengthening of the US dollar as investors sought safe-haven assets. But this time, the US dollar has experienced a pronounced decline, reflecting a shift in investor sentiment and its valuation.

However, a weakening US dollar doesn’t equate to a weak US dollar. In fact, the US dollar has returned to its fair value range for the first time since 2021, according to Vanguard’s valuation models (as the second chart below shows). This suggests that the currency is no longer overvalued relative to its economic fundamentals, such as productivity and real interest-rate differentials, and against a basket of other major currencies.

Implications for investors

For investors, especially those based in the UK, the US dollar’s depreciation has real consequences. Over the past decade, a strong US dollar and booming US equity market have boosted returns for unhedged UK investors. But with the dollar now fairly valued and US equity valuations looking stretched, future US equity returns may be more muted for sterling-based investors.

This has reignited interest in currency hedging. Yet, as Vanguard’s research cautions , hedging is not a panacea. While hedging may reduce short-term volatility, it can be costly over time and often fails to deliver consistent benefits. With the US dollar now within its fair value range, the cost of hedging has come more into focus. As such, we encourage investors with a long-term horizon and wealth accumulation or preservation goals to hold global equities unhedged and global bonds hedged. This is to capture as much of the diversification benefit as possible of both the underlying assets and currency fluctuations, while ensuring that volatility is consistent with the comparable local asset. Overall portfolio volatility can be reduced by maintaining a balanced and diversified portfolio across and within asset classes.

The US dollar’s unrivalled share of global markets

Despite recent depreciation, the US dollar remains the most-used currency in global markets. For instance, the US dollar represents 58% of global foreign exchange reserves, 64% of international debt, 51% of international loans and 50% of global payments . These figures dwarf those of other major currencies as a portion of the global finance and investing landscape.

Fundamentals over headlines

While the US dollar’s recent decline has sparked debate, the fundamentals remain clear. The US dollar is undergoing a cyclical adjustment. Investors should look beyond short-term movements and focus on long-term positioning. A diversified global portfolio, with unhedged global equities and hedged global bonds, remains one of the best ways to navigate an evolving world in which the US dollar still plays a major role.

The benefits of global diversification – staying the course with a multi-asset solution

Considering the recent US dollar weakness, it’s crucial for investors to maintain a balanced and diversified portfolio. Naturally, when the US dollar depreciates, other currencies appreciate. Diversifying across asset classes (equities and bonds) and within asset classes (styles, sectors and countries) can help reduce overall portfolio volatility.

While currency fluctuations are a natural part of the global economic cycle, a broadly diversified investment strategy can help mitigate these risks and still capitalise on the opportunity for long-term growth.

1

1

2

3

What does the US dollar’s recent weakness mean for multi-asset investors?

Claire Hsu

Multi-Asset Product Management, Specialist, Vanguard Europe

Madison McCall

Multi-Asset Product Management, Specialist, Vanguard Europe

CONTRIBUTORS